In our current environment, stocks aren’t cheap. Aside from growth and some tech options which have taken a hit, many former value stocks are value stocks no more.

The rotation out of growth into value is in full swing and today, finding good stocks at decent value is a difficult proposition.

Given this, we are looking at companies that are poised to do well in a market where interest rates are on the rise and inflation is looming. In one of our last Premium pieces, we talked about some of the industries that may struggle in such an environment. On the flip side, one that stands to benefit is Real Estate Investment Trusts (REITs) – residential REITs in particular.

It is why this week, when Killam Apartment REIT (TSX:KMP.UN) jumped into our Top 20 – we decided to take a deeper look into the Residential REIT industry and see if a company like KMP.UN would be a good addition to our Dividend Bull List.

Another factor that played into our decision to look at Residential REITs – many have yet to recover and are still trading below pre-pandemic levels. This is despite strong performance by many of the industry leaders.

That means there is likely value to be found here

In total, there are 13 Residential REITs listed on Canadian exchanges. To narrow the list, we first looked at companies which had a market cap of at least $100M. That brought the list down to following nine:

| Symbol | Name | Market Cap (in Millions) |

| CAR-UN.TO | Canadian Apartment Properties Real Estate Investment Trust | $9,678 |

| IIP-UN.TO | InterRent Real Estate Investment Trust | $2,173 |

| KMP-UN.TO | Killam Apartment Real Estate Investment Trust | $2,131 |

| BEI-UN.TO | Boardwalk Real Estate Investment Trust | $2,011 |

| MI-UN.TO | Minto Apartment REIT | $788 |

| MRG-UN.TO | Morguard North American Residential Real Estate Investment Trust | $651 |

| HOM.UN.TO | BSR Real Estate Investment Trust | $379 |

| ERE.UN | European Residential REIT | $378 |

| MHC.UN.TO | Flagship Communities REIT | $143 |

From here, we’ve removed current Dividend Bull List selection Minto Apartment REIT (TSX:MI.UN) and Flagship Communities (TSX:MHC.UN). Flagship is a recent IPO and doesn’t have the operating history required to be added to one of our Bull Lists – it also lacks many data points which hinders our analysis.

Given that we are interested in adding a company to our Dividend Bull list, we like to look for companies that have at least some sort of history of dividend growth. They do not have to be All-Stars or Aristocrats, but we like to see some sort of commitment to dividend growth.

This narrows our list further as Boardwalk REIT (BEI.UN.TO) and BSR REIT (HOM.UN.TO) have no dividend growth history to speak of. In fact, Boardwalk REIT cut the distribution in a material way a few years ago and as such, is one we will want to avoid.

That leaves 5 legitimate contenders

Let’s start with the dividend.

| Symbol | FFO Payout Ratio |

Yield | Dividend Growth |

| CAR-UN.TO | 46.18% | 2.42% | 9 |

| IIP-UN.TO | 66.71% | 2.06% | 9 |

| KMP-UN.TO | 78.97% | 3.47% | 4 |

| MRG-UN.TO | 46.91% | 4.22% | 5 |

| ERE.UN | 45.34% | 3.78% | 2 |

As you can see, there are some notable differences here. First, there are those with attractive yields above 3% (KMP, MRG and ERE), and a subset with lower yields (CAR and IIP). Worth noting, current Dividend Bull list stock MI.UN would fall in the latter category with a yield of only 2.08%.

CAR and IIP have established themselves as the most reliable dividend growth REITs, both with nine-year streaks. MRG just achieved Aristocrat status this year, and KMP is on pace to achieve five consecutive years of dividend growth this year.

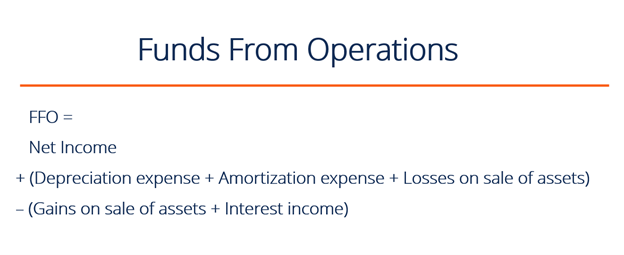

When it comes to the safety of the dividend, there are no concerns with any of these companies. The dividend is well covered by FFO which by our definition is as follows:

FFO = Net Income – Gains on Assets + Losses on assets + Amortization & Depreciation + Other non-cash Items

It is important to note that FFO is a non-GAAP item, which means there is no “standard” calculation, and it can vary differently from company to company. This makes comparing publicly posted numbers against each other very difficult. Same goes for analysts – they will each have their own way of calculating the numbers.

From our perspective, we chose the above formula given the data available to us in Ycharts

It is also consistent with the broad strokes of the commonly accepted definition which is simply described as follows from the Corporate Finance Institute:

Anything below 80% here is generally accepted as being a sustainable distribution. As we can see, the distributions appear to be well covered.

Looking at the debt load of a REIT

Debt load and interest coverage ratios are other important factors to consider is determining the strength of the company’s financial position. A company in strong financial position is more likely to result in a sustainable dividend.

| FFO/Interest | D/E | D/EBITDA | D/Assets | |

| CAR-UN.TO | 3.48 | 0.58 | 4.70 | 35.42% |

| IIP-UN.TO | 2.38 | 0.52 | 4.56 | 32.79% |

| KMP-UN.TO | 2.08 | 0.98 | 8.92 | 45.54% |

| MRG-UN.TO | 0.97 | 1.00 | 8.22 | 41.52% |

| ERE.UN | 0.78 | 2.25 | N/A | 47.55% |

An interest coverage ratio of 2.0 or greater is usually considered good – for REIT’s, we’ve seen the average start to creep up over the years thanks to record low interest rates. In terms of the Residential REIT industry, the current average is 2.35.

Interest coverage ratio is used to figure out how much FFO (funds from operations) a company generates compared to the interest outstanding on it loans. For example, we see above that Canadian Apartment REIT has a ratio of 3.48, meaning for every $3.48 in FFO it owes $1 in interest from its debt. Obviously, a ratio below one signals the company may not be able to pay down debt.

Canadian Apartment REIT is the clear stand out here with an attractive Interest Coverage ratio of 3.48 while MRG and ERE’s ratios which are below 1 certainly raises some red flags.

A quick note on stocks as well, when calculating interest coverage ratio, you’d typically use EBITDA, not FFO.

In terms of debt, there are three areas we look at

Debt to Assets (D/A), Debt to EBITDA (D/EBITDA) and Debt to Equity (D/E). In general, the accepted ranges for REITs include a D/A between 30-50%, D/E ratio of 3.5 to 1 and D/EBITDA of 6 to 1.

All five are within the D/A range and all five have very attractive D/E ratios – so no issues here. In terms of D/EBITDA, there are notable differences. Both IIP and CAR.UN have very attractive D/EBITDA ratios, whereas KMP and MRG are a little high. Worth noting, ERE has negative EBITDA over the last twelve months, so its ratios cannot be calculated.

Next let’s turn our attention to growth

There aren’t many high-growth REITs which is one of the reasons why we added Minto REIT last year. We liked the company’s combination of valuation and growth which offset the low yield. Thus far, with the REIT being up more than 24% since adding it, our thesis is well in tact.

| Revenue Est 2YR AVG |

EPS Est 2YR AVG |

|

| CAR-UN.TO | 6.48% | N/A |

| IIP-UN.TO | 24.98% | 13.86% |

| KMP-UN.TO | 21.54% | 8.87% |

| MRG-UN.TO | -5.08% | 1.34% |

| ERE.UN | N/A | N/A |

There are no estimates for ERE and MRG is looking at negative earnings and low, single-digit revenue growth. The clear winners here are both IIP and KMP which are expected to see impressive growth rates over the next couple of years.

Once again – details are important. Despite IIP’s impressive 25% average earnings growth estimates, it is important to note that this is inflated by a 55% increase in Fiscal 2021 followed by ~5% decrease in Fiscal 2022.

In other words, lots of volatility expected for IIP earnings in the coming years. For all the others, growth is consistent in both Fiscal 2021 and Fiscal 2022.

Given this, KMP is the clear stand out in this area and is likely why the company jumped into our Top 20.

Finally, we turn our attention to valuation

Traditional valuation metrics such as P/E, P/S and P/B don’t really mean much when comparing REITs. We prefer to look at two key metrics – P/FFO and Net Asset Value (NAV).

| P/FFO | NAV per share | Discount to NAV | |

| CAR-UN.TO | 18.80 | $ 49.10 | -14% |

| IIP-UN.TO | 32.10 | $ 8.25 | -90% |

| KMP-UN.TO | 22.59 | $ 16.52 | -18% |

| MRG-UN.TO | 11.18 | $ 37.59 | 56% |

| ERE.UN | 12.01 | $ 8.52 | 50% |

On average, Residential REITs are trading at 15.42 times FFO and as we can see, there are pretty significant differences among our five. The three largest REITs are all trading at a premium to this average, whereas the smaller players are trading at a discount to the average.

This is not all that surprising. Usually, the larger companies in the space command a premium and we can see that playing out here. I’d also suggest that ERE and MRG are trading at bigger discounts since they have been impacted more than the others over the course of the pandemic. I also circle back to that interest coverage ratio and lack of growth as being issues.

In terms of valuation calculations, Net Asset Value is one of my favorites. To calculate NAV, we use the following formula:

NAV = (Net Operating Income/Weighted average Capitalization Rate) – Long-term Liabilities

To find the capitalization rate, one must dig through the financial statements but most, if not all REITs do post their weighted average Capitalization (Cap) rate. By taking the NOI (net operating income) and dividing it by the Cap rate, you are effectively getting the REIT’s asset value. Then you subtract its liabilities from its balance sheet to get the NAV.

From there it’s simple, as taking the NAV and dividing it by the number of shares outstanding and compare to the current price.

Not surprisingly, the same three are trading a premium and the same duo at a discount. At one point, most REITs were trading at a discount to NAV but that was an anomaly which impacted the entire sector last year.

The big outlier here is InterRent which is trading at a pretty significant premium to NAV.

As a result, we have a new addition to the Dividend Bull List

Typically, we don’t go into such detail when we announce our Bull List stocks. Most members want simple, not complex reasonings for purchasing stocks.

However, we wanted to guide members through our thought process for REITs, which can be tricky. We tried to make this piece as easy as possible, and we imagine there is still questions. So, feel free to utilize the Q and A or the Discord.

We are currently working with Ycharts as we try to develop a REIT Screener, similar to our Growth and Dividend screeners.

Since REITs aren’t directly comparable and many traditional metrics don’t make sense, we have struggled with their inclusion in both the Growth and Dividend Screeners. For example, our new Dividend Bull List stock ranks very low on the screener, despite having a very safe distribution.

Our REIT screener has been a year in the making and we are hopeful to have something available over the next few months.

With that said – which Residential REIT will be added to our Dividend Bull List? This was a very tough call. We could have easily went with CAP.UN or even IIP.UN, but instead we are going to add Killam Apartment REIT (KMP.UN) to the list.

While Killam’s financial position is a little weaker than the others, it is still on strong footing. We also already have a low yielding REIT in Minto – which by the way is arguably better financial position that any of the residential REITs we’ve looked at. It was simply left out of the comparison due to its inclusion already.

When you combine Killam’s much higher yield, decent valuation and very attractive growth rate, we believe Killam is well positioned to outperform the industry. It also provides a nice complement to MI.UN for those looking for exposure to the industry, but one with a higher yield.

And, as we will explain more in depth in the report below, it is perfectly reasonable to include both Killam and Minto in a diversified residential REIT portfolio, as they are exposed to much different markets.