Although the Canadian markets are closed today, we are seeing some extensive volatility on the US markets that will likely spook many investors.

As I write this, the S&P 500 is down by more than 4% and the NASDAQ by nearly 6%. As I have reiterated for quite a few newsletters now, I felt the US markets were getting quite frothy in terms of valuation and that it was a “when, not if” situation regarding a correction.

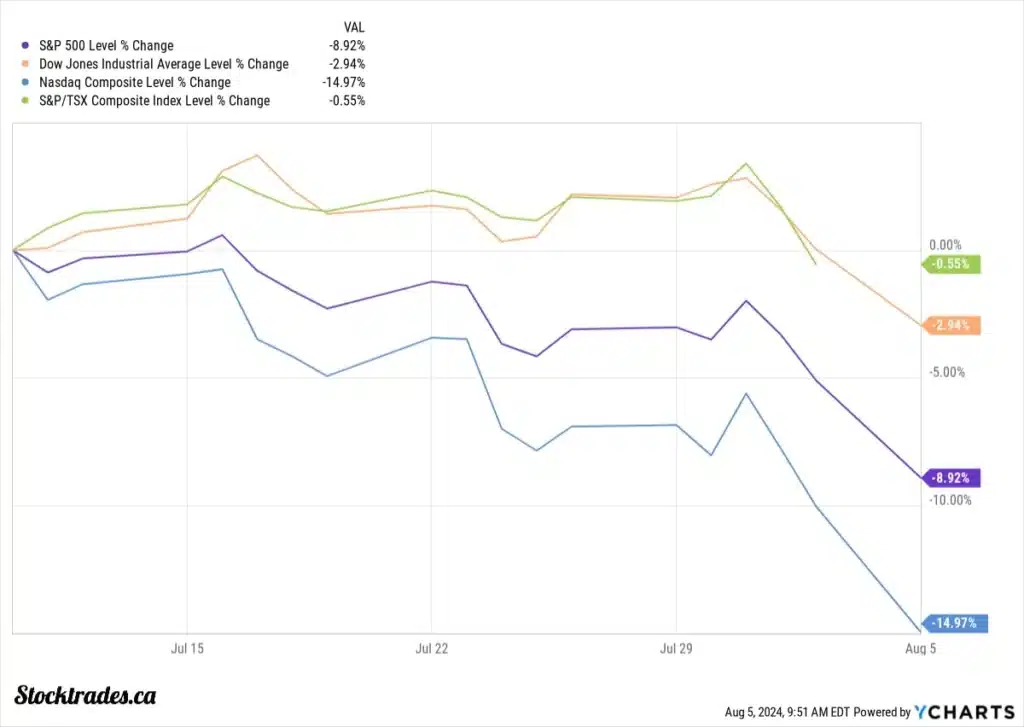

Since July 10th, the NASDAQ is down 15% and the S&P 500 9%. The TSX, on the other hand, is down just 0.5%.

At this point in time, a weak jobs report last week is stoking fears that the United States may have waited too long to cut interest rates.

There was little doubt that the market was pricing in a soft landing of the US economy, which, although still possible, is looking like it is far from guaranteed.

Yen carry trade risk

The other reason for the rapid decline in US stocks is quite complicated, and I’ll attempt to explain it as easily as possible.

There has been a popular strategy over the years to borrow Japanese Yen and then invest that money into other assets that can earn you profits over and above what you are paying to borrow the Yen.

The reasoning for this is fairly simple. Japan has had low interest rates for a long time, and the Yen is also typically a stable currency.

They call this a “carry trade,” and this is executed mostly at the institutional level. Keep in mind, however, that institutions are the ones that truly cause the markets to move.

If the costs of borrowing Yen increase or the Yen strengthens relative to the US dollar, the profitability of this carry trade reduces. Japan just raised interest rates for the first time in 15 years.

As a result, you will see a selloff in US equities as institutions look to possibly cover their trades and reduce their exposure to the Yen.

In addition to this, the Japanese markets suffered their largest single-day loss since the 1987 stock market crash, one of the worst crashes in history. This alone is enough to spook the markets on a global scale.

Berkshire selling a large chunk of Apple

Although this likely wouldn’t be notable enough to move the entire market, if there was ever a signal of US market valuations getting a bit extensive, it would be Foundational Stock Berkshire Hathaway (BRK.B) reducing its position in Apple by 55%.

Berkshire has sold a total of 505 million Apple shares this year, 115 million in the first quarter and a whopping 390 million in the second quarter.

While Apple is still the company’s largest holding, the large reduction in Berkshire’s position is a bit of insight into the mind of one of the greatest investors of all time.

Although he had stated the sale of Apple shares in the first quarter was due to “tax reasons,” the sale of 390 million additional shares in the second quarter tells me that it was likely more than that.

What to make of all of this

I will sound like a broken record here, but as long-term investors, we should try to avoid concerning ourselves with the short-term movements of the markets.

Whether we bought a stock last week, last month, or even last year, the approach should be long-term. Concerning yourself with how a stock has moved over the short term can lead to panic-driven decisions, which is why the vast majority of retail investors underperform the markets.

There is almost no doubt we will see significant volatility in the coming weeks. Ultimately, long-term investors who are in the accumulation stages of their investing careers should welcome lower prices, no matter how uncomfortable it may be because of the decline in your current holdings.

After posting one of the strongest months for my portfolio since the start of 2023, it is highly likely those returns will be wiped out in a matter of a day or two. Most investors would fret over this. However, I’m completely fine with it. If the drawdown is extended, I’ll welcome the lower prices so I can continue to buy for cheaper.

My portfolio moves

I made one move last week, adding a sizable chunk to my Amazon (AMZN) position based on a decline post-earnings.

The timing does seem poor, as I could have got Amazon at an additional 5%~ discount today. However, I’m happy with the price I paid on Friday as I believe Amazon is one of the more attractive mega caps on the US markets at this time.

I won’t speak much on Amazon in this section of the newsletter but I will instead get right into our earnings commentary, as this should give you a good idea as to why I ended up pulling the trigger and bumping my Amazon position up to 5%~ of my total portfolio.

Earnings

Amazon (AMZN)

Amazon reported a strong quarter in terms of headline numbers. Still, softer than expected guidance and a warning about the potential health of consumers caused the stock to dip by double digits post-earnings. Of note, I took advantage of this dip and added a reasonable chunk to my Amazon position.

Revenue of $148B came in $800M shy of estimates, but earnings per share of $1.26 came in well ahead of expectations for $1.06. Amazon Web Services revenue came in at $26.3B and its Advertising segment came in at $12.8B. These were small beats and misses on expectations, respectively. Overall, the company’s AWS segment grew revenue at a 19% clip year-over-year, while Advertising revenue grew by 20%. On the retail side of things, sales grew by 5%.

As I’ve always mentioned, the core thesis when it comes to Amazon is the rapid development of AWS and Advertising along with the “moaty” retail end of the business that is not entirely immune but well-sheltered from competition.

The company stated that they fell short on their revenue estimates, and attributed most of it to lower ASPs, or Average Selling Price. They mentioned they are seeing a notable consumer shift of buyers trying to select the cheapest product that suits their needs rather than ordering more expensive ones. They mentioned on the conference call that they are continuing to see this type of pressure on ASPs in the third quarter.

In terms of guidance, the company stated revenue is likely to land somewhere in the $154-$158B range, and operating income to land somewhere in the $11.5-$15B. This would represent 8-11% growth on the revenue side of things and on the bottom end of guidance, flat operating income. This guidance was short of expectations, and combined with the above comments on Average Selling Price, this is why I believe Amazon took a bit of a nosedive on earnings day.

Overall, to me it was a pretty solid quarter. I welcome the weakness and will likely add to my position. I viewed Amazon as cheap even prior to this 10%+ dip, so I am happy to add at lower prices.

Starbucks (SBUX)

Starbucks reported another soft quarter as macro-headwinds continue to impact the company. Revenue of $9.11B missed estimates, albeit by a miniscule amount, and earnings per share of $0.93 came in line with expectations.

When we look to year-over-year overall sales, they’re down 1%, with same-store sales declining by 3%. The harshest impacts on a same-store-sale basis came from its China segment, which witnessed same-store sales drop by 14% as both foot traffic and overall transactions continue to decline.

The issues weighing on the company in China are particularly intense, as Chinese consumers have traditionally been much less “spend happy” than North American consumers. When times get tough, they tend to scale back spending at a much quicker rate than North American consumers, and this can be reflected in the fact that overall consumer spending makes up a much smaller portion of China’s GDP than the United States.

Although China represents a strong growth vertical for the company, investors must accept that the country will be exceptionally volatile during times like this on the company’s results.

The company’s loyalty program continues to grow, with 7% year-over-year growth. This is likely a direct impact of consumers wanting to scale back spending and save every penny possible, as the loyalty program does reward frequent customers with free drinks and food.

On the new product end, the company reported that its Boba drinks, or “Bubble Tea,” as many like to refer to it, were so successful the company could not keep up with demand and had to scale back marketing efforts.

The company reiterated its guidance for relatively flat revenue growth and earnings growth in the low single digits.

Overall, the market reacted positively to the quarter, as many of the struggles it is facing at this point were predicted by the company themselves, somewhat softening the blow. I’m still bullish on Starbucks and will continue to add as prices remain attractive. I do not believe the economic situation will last forever, and Starbucks has a strong enough brand among many consumers that they will return once they see some sort of relief when it comes to interest rates.

Probably some of the most notable news on Starbucks as of late isn’t earnings, but that global hedge fund Elliott Management has taken a stake in the company as an activist investor. The total position is unknown but is said to be “large.” Up until this quarter, most of the talk was rumour, but the CEO stated in this quarter’s conference call that it is indeed true.

The hedge fund wants an expansion of Starbucks’ board, but to my surprise, has pitched an apparent offer where the current CEO could stay. In a way, this makes sense, as he has only been in place since 2023, but there was a lot of bad press on how he butchered last quarter’s conference call, so I had expected if they wanted changes to the board, it would include a new CEO.

TFI International (TSE:TFII)

TFI posted a strong rebound quarter in Q2. Revenue of $3.2B came in line with estimates, and earnings per share of $2.36 topped expectations of $2.21.

Operating income increased to $208M from $192M in the second quarter of 2023, highlighting that despite significant economic weakness and lower demand for freight, TFI International has been more than able to offset this with new acquisitions and efficient operations.

The company grew revenue in its Less-Than-Truckload segment by 1.4%, its Truckload segment by 77% (acquisition-driven), and its Logistics segment by 24% (partially acquisition-driven).

The lack of growth in the Less-Than-Truckload segment is not unusual. We’re seeing a reduction in consumer spending, and as a result, there is lower demand for freight. We can expect this to be cyclical and should rebound on a pickup in economic activity as interest rates continue to decline.

The company’s free cash flow came in at $151.4M on the quarter, a 9.4% jump from the second quarter of 2023. In terms of earnings per share, it reported a 6% decline.

Overall, the results are pretty much what can be expected from the company, considering the current environment. The fact it has been able to put up such impressive numbers during times like this highlights the fact that it is one of the most efficient trucking companies in North America. It should be able to rebound well on a pickup in consumer spending and overall economic activity.

In terms of its outlook, it is much the same. The company remains extremely cautious in its overall commentary, highlighting that economic uncertainty prevents it from making concrete statements about results. At this point in time, we simply need to rely on the company’s strong history of execution to get through the rough environment, and shareholders should be able to reap the rewards of an inevitable pickup in activity.

You can click here to read our full report on TFI International