Now that we are on the other side of earnings season, we figured it would be an excellent time to look at the latest Ycharts Fund Flow report, which summarizes the newest fund flow data.

The reports reveal the categories, funds, and ETFs with the most significant cash inflows and outflows each month, plus additional historical periods.

In just a few pages, these reports give insight into where the market is trending, which can be a helpful tool to gauge market sentiment.

We have found these reports extremely useful as part of our research, and if you’ve got time to read them, they are well worth it.

There are four reports in total. I’ll link to them below.

The latest reports were released recently, and the data is reflective as of the end of February.

Canada Overview

Let’s kick things off with a look at what is happening in Canada. For today’s purposes, we’ll focus on the Strategy Flow document, which reflects the combined outflows and inflows of both Mutual Funds and ETFs.

You can always check out the individual Fund Flow reports linked above for a more detailed breakdown.

Here is a snapshot of the two most important tables. If these tables are blurry or hard to read in this e-mail, I’ve listed links below where you can see them in full size. Alternatively, you can also reference the reports above.

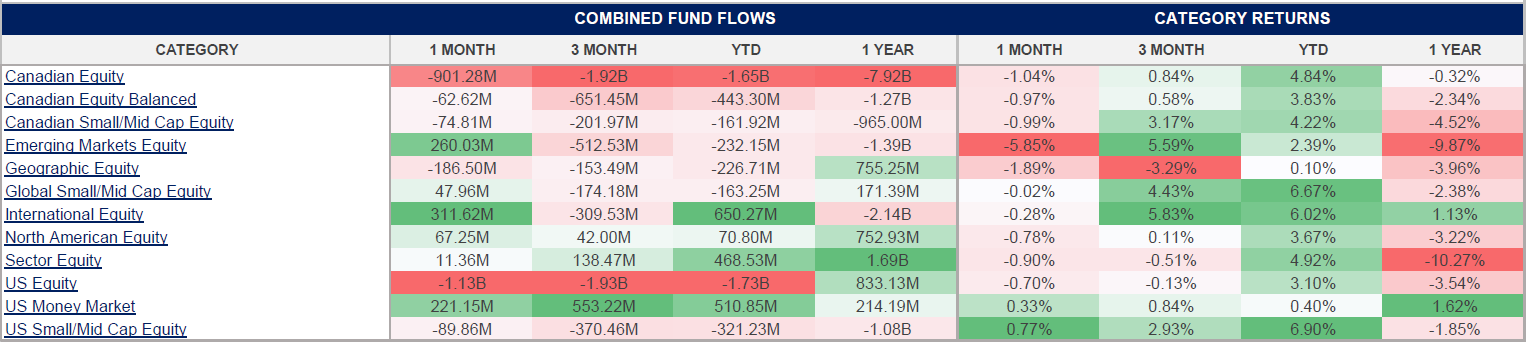

Equity Fund Flows

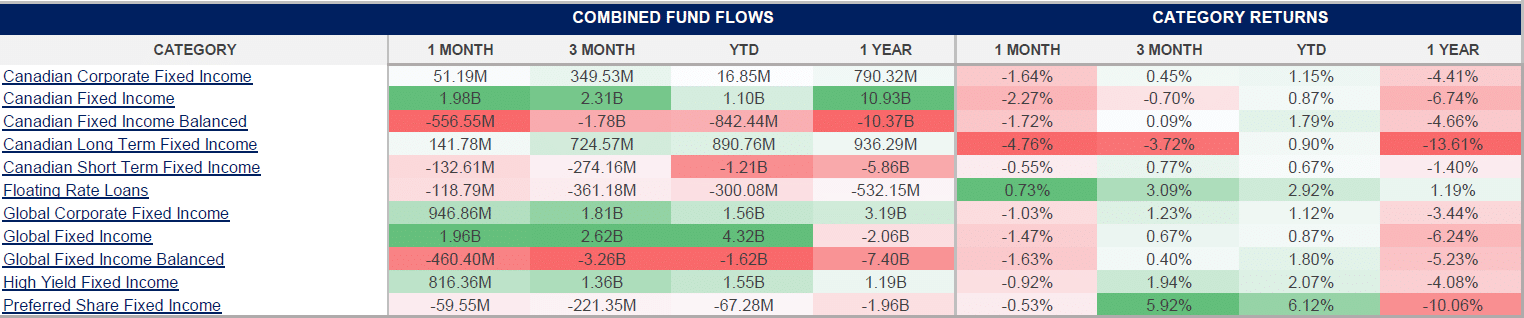

Fixed Income Fund Flows

{kind=link}

{kind=link}

First, let’s look at the equity side and bring your attention to Category Returns.

The most significant outlier is the -5.85% in emerging markets, and only two categories were in the green: US money market funds and US small/mid caps. On the year, we see small to mid-cap equities outperforming almost across the board.

This is a sign that the markets have gone a bit more risk-on during February, and we’re even seeing it as we enter April. We have also seen this ourselves, with many of our smaller Bull List picks delivering outsized returns since the fall.

Is this a sign of a market turnaround? It’s difficult to say and likely too early to call. Canadian equities saw nearly another billion in outflows, and on the year, both Canadian and US equities continued to show weakness.

However, one promising element is that small-cap US and Canadian stocks are having a solid start to 2023. Because of their riskier nature, small-caps tend to bottom out earlier than their large-cap peers. Rising small-cap stock prices can indicate a market turnaround.

Canadian Fixed Income

Switching our attention to Fixed Income, Canadian Long Term Fixed Income continues to underperform, which is not surprising in an environment of rising rates.

Remember, as rates rise, the value of lower coupon bonds drop, hence the negative returns on longer-term bonds that are likely paying out lower than average yields.

The longer the bond’s maturity date, the more exposed it is to interest rates. This is why you see short-term fixed income outperforming long-term extensively over the last year.

However, when we ignore returns and instead look to money flowing in and out of fixed income options, we can see large-scale inflows over the last 1, 3 and 12-month time frames.

Fixed income has become a viable option for many for two reasons. First, attractive yields. This has not existed for decades, and for the first time, investors can lock in desirable yields without purchasing stocks.

Secondly, many investors are likely purchasing fixed income with the idea that bonds and other fixed-income investments should increase in value when rates go down.

Overall, on the Canadian end, there is a clear shift here: investors are hesitant to buy stocks at this point. They are opting for safer, more reliable investments such as money market funds and other forms of fixed income.

As investors with long-term time horizons, we understand that these periods of uncertainty are often the best time to ignore the noise and accumulate stocks.

US Overview

We get a little more data breakdown with US reports, and here is a good graph that touches on the risk-on sentiment we mentioned earlier.

In February, large caps saw ~$29B in outflows, and small/mid caps were in positive territory. However, we still see significant overall outflows due to considerable market uncertainty.

This graph below is pretty telling. At this moment in time, investors are selling off equities in favour of money market funds and fixed-income investments.

A Money Market fund invests in short-term assets like cash or cash equivalents and US Treasuries. Money market funds are intended to offer investors high liquidity with a very low level of risk.

Once again, this shift is not surprising as investors are still struggling with existing uncertainty.

Anecdotally, we have seen it ourselves as there has been much discussion about CASH and HSAV ETFs. Investors like the idea of being able to park their cash in a relatively safe product while the markets sort themselves out. And while pre-pandemic, these funds yielded relatively nothing, they are now very attractive, with yields (capital appreciation in the case of HSAV) at nearly 5%.

While this data is reflective of February, we had the banking crisis hit the markets in March. Once released, we will be sure to share those reports, as it will be interesting to see how the fund flows differ.

One area that is sure to be quite different is the sector inflows. Financials led the way in February, but we are likely to see a pretty significant turn in this sector in March.

We can also see that the energy sector was hit the hardest in February, as widespread fears of a recession are causing the price of oil to drop.

The bottom line

Overall, these reports tell us that although the markets seem to be turning a corner, the fact that so much money is flowing out of equities and into fixed-income investments should be a sign that investor hesitancy is still alive and well.

While the markets are having a decent start to the year with the TSX (+3.69%), the S&P 500 (+7.03%) and the Nasdaq (+16.77%) all in positive territory for the first quarter, we feel we will need a pretty clear cut direction on inflation, the economy, and the current banking situation in the United States before we see large cash inflows return to stocks.

For now, investors can accumulate outstanding companies at cheaper valuations.