First, I’d like to wish you a Happy New Year and thank you for your continued support. Ultimately, I cannot do what I do without the support of our members.

It has been a tough year for a lot of Canadians financially. So, the fact you can find room for a Stocktrades membership means a lot to me.

I will continue providing rock-solid investment content, guidance, and education moving forward in 2025 and beyond.

With investors itching to spend their TFSA and RRSP contribution room, I’m going to keep this month’s newsletter simple and speak about some of my favourite funds moving forward in the coming year.

First, however, let’s go over some ways to maximize value for yourself here as an ETF Insights member in 2025.

How to maximize value as an ETF Insights member

Our ETF Insights platform is intentionally simplistic, as most who choose the ETF route don’t want to be obsessing over the markets on a daily basis.

However, there are a ton of features available on the website to help you unlock the most value possible and maximize the benefits when it comes to your portfolio.

The first one, and arguably the most valuable, is the Question and Answer page. This is where members can log in and ask any market/investing-related questions they have.

The second is my ETF Screener. There is no other screener on the market like the one I have developed here at ETF Insights, and it can significantly reduce the amount of time you have to spend hunting for particular ETFs. If you don’t know how to use the screener or have some specific questions regarding the screener, utilize the Q&A to get them answered, or follow the tutorial video on the screener itself.

The third is my ETF reports. Throughout the month of January, I’m going to be updating all of my current ETF reports, plus adding more of my favourite funds in the start of 2025.

And finally, there is our monthly newsletter, the one you’re reading right now. Just know that you can also head back to the website and read prior issues of the monthly newsletter, many of which have timeless information inside of them.

Some of my favourite ETFs heading into 2025

There is no question the markets are becoming expensive, at least from a historical basis. Many investors are hesitant to invest out of fear of a major correction.

As I always say when it comes to timing the market, you’re either wrong or you get lucky. If your investment time horizon is long, you’re better off ignoring all thoughts outside of building a diverse portfolio and holding it indefinitely.

As your time horizon gets shorter, things become more difficult. Investing at market peaks for someone with 30+ years left to invest is way less intimidating than for someone with 5 years left before retirement.

A prime example of this would be an investor purchasing an S&P 500 index fund in 2007. Fast forward 18 years, and that investment is up over 430%.

However, at one point, it was down over 55%. So for someone with a 5 year horizon, things could certainly get ugly rather quickly.

A few months ago, I produced a newsletter on the attractiveness of fixed-income ETFs. For someone with a shorter horizon, it may be wise to head back and have a read of that and consider adding some fixed-income items to your portfolio.

In general, I strongly advocate for investors to ignore the noise and instead dollar-cost-average into a basket of high-quality assets.

Which leads perfectly into some of my favourite ETFs for 2025. I’ll attempt to cover all areas of the market, along with some niche funds.

Canada – BMO Low Volatility Canadian Equity ETF (TSE:ZLB)

If you’ve been following me for long enough, you would know that I’m not a huge advocate for indexing to the Canadian markets.

I believe we have too many cyclical companies here in Canada that are too dependent on commodities. This leads to outstanding returns during times of prosperity, a prime example being oil stocks in 2021/2022, but also leads to significant underperformance during poor periods.

Case in point, XEG, arguably the most popular Canadian energy ETF in the country, has returned close to half of what the TSX has over the last decade. It looks even worse when we compare it to the S&P 500, which has provided 4X the returns of XEG.

For that reason, I believe there is a place for actively managed funds in Canada, and I’m a huge fan of ZLB. I also believe 2025 will be a fairly unique opportunity when it comes to ZLB, as it posted a rare year of underperformance relative to the Toronto Stock Exchange in 2024.

Now, keep in mind that returning 18% in a single year is hardly “poor” returns. But, relative to the TSX, which returned just over 20%, it did underperform.

The bulk of this underperformance can be attributed to the fact that it is a low-volatility fund. During periods of heavy speculation and high valuation in the markets, low-volatility blue chips are often ignored.

However, if you look to the image below, you’ll see that ZLB has consistently provided better risk-adjusted returns than the index over the last decade. When we look to the Sharpe Ratio, which measures risk adjusted returns, the higher, the better. You’ll see ZLB has outpaced the TSX 60.

What this means, in a nutshell, is that you have achieved better returns with lower risk owning ZLB over XIU, a TSX 60 index fund.

In addition to this, the rising price of gold and other precious metals pushed materials companies higher on the year, and materials companies make up a decent portion of the TSX.

I won’t go over too much of the details of ZLB as a whole, as I have a full report for the fund on the website which you can view here.

Instead, I’ll more so speak on my core thesis for the fund in 2025.

Valuation relative to earnings

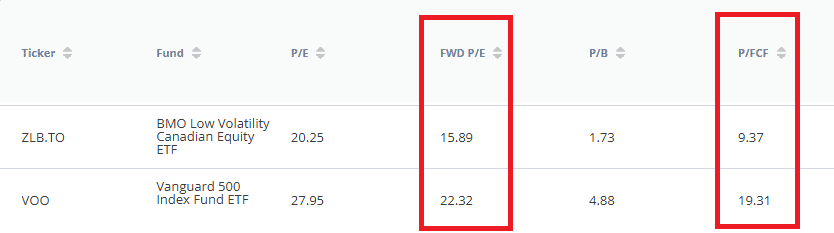

Thanks to my ETF screener, you can view overall valuation metrics for each particular fund. At only 15.8x expected earnings and 9.5x trailing free cash flows, the basket of 52 holdings that ZLB holds are trading at relatively cheap valuations.

These valuations are compared to expected growth, of course, as the stocks inside of the fund are expected to, on average, grow earnings by 8.4% next year.

When we look to a fund like VOO, an S&P 500 ETF, it is expected to grow earnings by around 9% in 2025. Yes, this is a higher rate of earnings growth. However, the key thing here is the valuation.

At 22.5x expected earnings and 19.5x trailing cash flows, VOO is trading at substantially higher valuations than ZLB, despite a small gap in terms of earnings growth.

The potential reasonings behind this

There are numerous reasons why this valuation gap could exist. There is no question that our current political climate is a bit of a mess. Our dollar is currently in the tank, and the potential for tariffs on goods due to Donald Trump’s win no doubt looms large.

However, I believe a lot of the stocks inside of this actively managed fund from BMO are not going to be impacted all that much by tariffs and will also continue to benefit heavily from interest rate declines here in Canada, of which I have little doubt we see more of in 2024.

I believe it is a solid fund for those who don’t want to index in Canada, but also don’t want to pick stocks

ZLB gives you exposure to 50+ of the best names in the country, many of which have been some of the best performers in the country as of late. It contains a nice mix of grocers, utilities, waste collection companies, discount retailers and more.

And, with current valuations, it’s on the cheap side.

United States – BMO MSCI USA High Quality Index ETF (ZUQ.TO)

As I’ve always stated, I am a big fan of factor funds, particularly those that are the “high quality” variety. What these funds aim to do is isolate out a particular basket of companies and target the ones with the highest “quality” factors that often lead to outperformance.

Think earnings growth, returns on equity and invested capital, strong debt ratios, etc.

In my opinion, the BMO MSCI High Quality Index ETF is one of the better options for investors looking for a more concentrated approach to US equities instead of buying the S&P 500.

ZUQ posted a significant beat over the S&P 500 in 2024, returning over 35% versus the S&P’s 25%. However, the bulk of this was due to currency fluctuations. The currency-hedged version, ZUQ.F.TO, outperformed the S&P 500 by about 3% in 2024, which is a more accurate representation of the performance of the underlying holdings.

Make no mistake about it, however, currency fluctuations are currency fluctuations and losses/gains from them must be accounted for.

As always, I won’t go over the basics of the fund because I have a full report on it available here. Instead, I’ll go over the 2025 thesis.

Valuations relative to the S&P 500

As always, I used the ETF screener to isolate the S&P 500 versus ZUQ to have a peek at the underlying valuations of the funds.

At this point, ZUQ is more expensive than the S&P 500, trading at 24x expected earnings versus 22.5x.

However, when we look at expected growth, the 6%~ premium in valuation starts to make sense.

ZUQ’s underlying holdings are expected to grow revenue by 11.3% and earnings by 10.14% in 2025. When we compare this to the S&P 500’s 6.21% revenue growth and 8.7% earnings growth over the same timeframe, we start to see why the fund may be a bit more expensive.

This does make sense, as ZUQ takes a more concentrated approach to its holdings and targets companies that offer high returns on capital and historical earnings growth, which can be a major contributing factor to future earnings growth.

Lower quality companies inside of the S&P 500 will ultimately drag valuations down, and what ZUQ aims to do is remove exposure to those companies.

To hedge or not to hedge?

For the longest time, I have been firmly in the territory of the idea that hedging makes little sense unless your time horizon is short.

This is because, over time, currency fluctuations tend to even out and all you’re left without is the hedging fees you paid to the fund.

However, with our dollar cracking 70 cents, we at least need to start asking ourselves if this theory still makes sense.

With unhedged ETFs like ZUQ, you own both the currency and the underlying holdings.

This means that if the dollar continues to weaken, you will outperform on a constant currency basis with ZUQ.

However, if the Canadian dollar strengthens, you will underperform. Look to the chart below. You will see during times of Canadian dollar strength, ZUQ.U outperforms (2021), and vice versa.

Let’s assume the S&P 500 returns 8% next year. If the Canadian dollar strengthens to $0.745, your 8% return will be wiped out. Alternatively, if the dollar weakens to $0.64, you’ll earn double (8% S&P 500 return and 8% currency return).

If one were to force me to answer, I would still lean to the side of being unhedged. I’m not particularly bullish on the Canadian dollar and the economy as a whole, and I believe the dollar is headed lower in 2025. However, predicting currency movements is a fool’s game, and I could easily be wrong.

If you’re worried about an increasing CAD, hedging makes sense at this point, and in this case, ZUQ.F.TO is a great fund for it. If you feel the CAD is going south, I like the unhedged version of ZUQ.TO as well.

International – TD International Equity Index ETF (TPE.TO)

TPE is not a fund featured here at ETF Insights, but it is one I will be developing a new report for shortly.

TD has a multitude of funds here in Canada, though the company is not particularly known for being a popular fund manager. But the more and more I look into a fund like TPE, the more I like it.

It is already hard enough for investors to navigate their way through the North American markets. So, for international exposure, I think it is almost a no-brainer to go the passive ETF route, particularly with an index fund like TPE.

The fund holds around 900 companies, many of them mega-cap global giants, including Novo Nordisk, ASML Holdings, SAP, Nestle, AstraZeneca, Shell, and Toyota.

Valuations are much lower, but returns have been lackluster

Despite all of the premiere companies I listed above (plus about 893 more), valuations for international equities remain much cheaper than not only the S&P 500 but the TSX as well.

Take, for instance, the 13.7x expected earnings that TPE trades at relative to the 22.5x of the S&P 500 and 15x~ of the TSX.

Interestingly enough, the stocks inside TPE are expected to post similar growth rates in terms of revenue and earnings as the S&P 500.

So, why the discounted valuations? The U.S. economy has historically grown at a faster and more stable pace compared to many international markets, making U.S. companies more attractive.

U.S. companies also generally have higher levels of transparency, corporate governance, and investor protections compared to many international markets.

And finally, investments in international stocks expose investors to currency fluctuations. Weak or unstable local currencies can reduce the attractiveness of international equities, leading to valuation discounts.

Overall, TPE is an outstanding fund for international equities, but I expect discounted valuations to remain

Lots of investors want diversification when it comes to international equities. I believe TPE provides a rock-solid option that primarily includes large and mega-cap companies in developed markets.

How much of your portfolio you designate to international equities (if any) is completely up to you. But I do like TPE for this type of situation.

Overall, I do like these 3 funds heading into 2025

ETFs have made the process so much easier for those who do not want to fuss with individual stocks.

Single-click diversity and the ability to dollar-cost-average into some of the best corporations in the world with just a few actions is certainly attractive.

The top 3 funds are some I have my eye on for 2025, but this is far from the only ones. In fact, there are so many new ETFs hitting the market these days it can make your head spin.

This is exactly why I started ETF Insights, to separate the good from the bad, because there is a lot more bad than good.

Happy New Year, and I’m excited to deliver you even more outstanding content moving forward in 2025.