It’s been an interesting last few weeks, to say the least. Often, in the span of a few hours, we can go from tariffs being implemented to delayed to potentially even doubled.

There have been few “normal” market environments since the launch of Stocktrades Premium in 2018. We had the pandemic and global lockdowns in 2020/2021, sky-high inflation and the fastest pace of rate increases in history in 2022, and now we’re facing the threat of some of the largest tariffs implemented by the United States since the early 1900s and one of the most confusing trade wars in a long time.

Many are asking me to comment on the potential impacts of tariffs. However, it is nearly impossible for me to do so because they seem to change daily.

However, there is one company in particular that I own and is also on the Bull List that I will be removing due to the potential tariff threats. I will discuss this in detail and get into the final batch of earnings commentary this quarter.

In terms of portfolio moves, I am still waiting on my money to be sent to Questrade. There has been some difficulties in terms of some old Constellation Software warrants that were not transferable and ultimately messed up the transfers.

Of note, if you missed my bank commentary last week, it was a must-read. I’ll drop a link below so you can read that.

Click here to read the most recent bank earnings overview.

I’ve decided to remove Savaria from the Bull List, with a caveat

Savaria has been a staple on the Bull List here for many years and has been a company I have owned since 2017. Until the recent news about tariffs, the company had been an exceptional performer over the last half-decade, outpacing both the TSX Index and the S&P 500.

The difficulty the company is faced with now is the threat of tariffs. Because Savaria deals with a lot of accessibility products like wheelchair ramps, stairlifts, and vehicle accessibility modifications, it has a lot of input materials and costs related to metals such as aluminum and steel.

As a result, the company is particularly prone to tariffs. The company’s most recent conference call stated that “the majority of the business is not exposed to tariffs.” However, the majority could mean anything over 50%, which still leaves a potentially sizable amount impacted. The vagueness of this and the fact that the company expects significant pressures over the short term if tariffs stick around make me a bit uncertain about the future.

Keep in mind that I am not selling Savaria at this point. The thesis for this company is still well intact. There has just been a bit of a roadblock here regarding tariffs and economic policy, and I am not comfortable with any sort of “buy” status. I am looking to hold the company until the issues are resolved.

I’m certainly not going to sell my position based on pure speculation in regard to the tariffs and their lasting impacts. Still, I also acknowledge that if they linger for long, Savaria would have to eat either the tariff, which would impact margins, or pass them on to the consumer, which could ultimately hit sales.

The caveat here is that if the tariffs were to be short-lived or potentially overblown, Savaria would quickly return to the Bull List.

I will keep everyone in the loop in this regard.

Earnings

Jamieson Wellness (TSE:JWEL)

Jamieson closed out Fiscal 2024 on a high note. Although revenue came in short of expectations, earnings of $0.80 topped estimates by a penny. The company issued some upbeat guidance, albeit with some caveats, which I’ll get to in a bit. First, I want to discuss the overall results.

Revenue grew by 8.4% on the year and earnings by 3.8%. Interest expenses still continue to weigh heavily on the company (see chart below), making up nearly 20% of its total operating income.

As rates continue to decline in 2025, we are likely to see some relief on that front, but the company certainly does need to prioritize getting that debt down from the 2023 acquisition of youtheory.

There was some nice margin expansion on the year, with gross margins improving from 34.5% to 37.6% and operating margins from 14.1% to 14.5%.

Its expansion in China continues to be notable, with revenue growing by 77.9%. This will slow in the coming years as the company continues to expand its market share in the country. However, it is deploying a large-scale marketing strategy and e-commerce platforms in China to accelerate growth.

The company has barely tapped into the market there, and there is certainly room for notable expansion; it just gets a bit difficult to predict at this point with the current tariff environment.

In the fourth quarter, the company reported 11%~ growth in its Jamieson Canada segment, 25%~ growth in its youtheory segment (primarily the US), and 38% growth in its Chinese segment. Overall, the bulk of its business is firing on all cylinders, and free cash flow is starting to improve over 2023 numbers.

The company released its Fiscal 2025 guidance, expecting to grow:

5%-8% in Canada 5%-15% in the United States 25%-30% in China

Its other international markets outside of China are expected to grow around 20%~. It expects earnings per share to come in between $1.82-$1.93, which would be growth of anywhere from 13%-20%.

The market initially reacted positively to this guidance, but the stock sold off after the conference call. If I were to guess, it was the commentary on tariffs. Jamieson did not include any particular impact of tariffs in its guidance.

The company mentioned that the large majority of its business isn’t exposed to tariffs. However, there could be some pressures over the short term as U.S. customers could be facing tariffs on products imported into the United States. This would no doubt impact the margins of that segment of the business.

Overall, it was a solid year, and I will be keeping an eye on the company in terms of tariff impacts. Its Canadian business and business in China should be well insulated, and the thesis is intact.

You can read our full report on Jamieson here

Alaris Equity Partners (TSE:AD.UN)

Alaris reported a relatively inline fourth quarter to close out Fiscal 2024. Of note, the only metric I typically look to in terms of analyst estimates is EBITDA. On that note, the company came in relatively inline, with EBITDA of $41.5M, just shy of expectations for $42M.

When we look to the year as a whole, the company deployed around $139M in capital. However, subsequent to year-end, it invested an additional $118M, bringing its total to around $249M over the last twelve months. This would have been one of the higher rates of capital deployment Alaris has witnessed since 2021.

The company earned $46.9M in partner distributions on the quarter and $194.2M on the year. This works out to be a 19% increase on a year-over-year basis.

This isn’t necessarily organic growth, however, as the bulk of the growth on the year was just a resumption of the distributions from LMS Steel. If you remember, the company ran into a ton of difficulties over the last while due to rising steel prices that effectively destroyed its margins and it was unable to make distribution payments.

This seems to be behind them now, which is a good thing because, during this period of time, Alaris remained relatively flat in share price as LMS is a reasonably sized partner and the market was a bit spooked.

The company’s book value now sits at $24.15, a notable increase of $3.03 over the course of the year.

The company provided some commentary on its stock price relative to book value, highlighting the fact that it will now look to buy back shares aggressively. This is not something we’ve typically seen from Alaris, and it is likely they’re doing this at the expense of distribution growth, believing it will provide more value.

I sold my shares of Alaris back when it hit 0.9x book value, which was its historical average. However, due to the increase in book value coupled with its recent drawdown due to the worries about the US economy, the company is now starting to look attractive again on a valuation basis, trading at only 0.79x book.

If it can revert back to historical averages of 0.9x, that would work out to be a share price of around $22, or 14.1% upside without dividends accounted for.

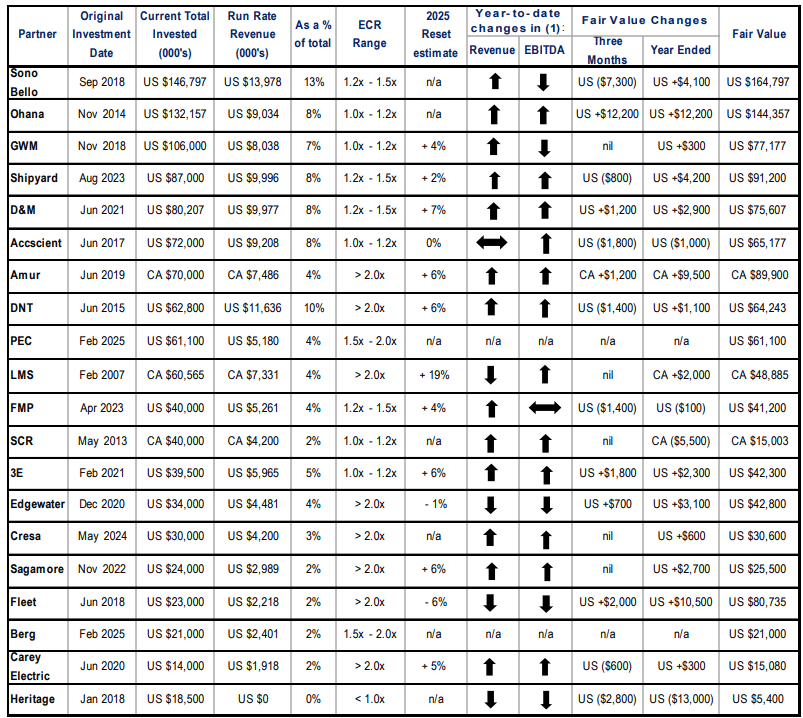

One of the main things I like to do with my quarterly overviews of Alaris is review its partners. This is no doubt one of the more important aspects of being a shareholder of the company, as it will give you an indication as to how healthy its underlying investment portfolio is.

14 out of its 20 partners have increasing sales, and 14 of the partners also have increasing EBITDA. When we look to its largest partners, as you can see by the “As a % of total” section, the bulk of its more critical partners are reporting increases in profitability. We can also see the vast majority of its portfolio has comfortable earnings coverage ratios.

The one main area I want to highlight from the management’s commentary, however, is this:

“90% of our investments are with US companies that are doing business strictly in the US. Because they are service companies, they do not relying on the import or export of goods. In addition to this, because our revenue and assets are in US dollars, we are in a good position if the Canadian dollar continues to weaken”

The company is not immune to the wild swings in economic data we are likely to see over the next few years under Donald Trump. However, they should be somewhat immune to the impacts of tariffs despite being a Canadian-listed company.

You can read my full report on Alaris here

Tourmaline Oil (TSE:TOU)

It was an interesting 2024 for Tourmaline. Amidst natural gas pricing weakness in early 2024, the company deployed nearly $2.8B into strategic acquisitions.

The first one, which would have been in the latter part of 2023, was Bonavista Energy for $1.34B. The second would be Crew Energy in October of 2024, where the company paid $1.1B. And the third and final was in December of 2024 when the company paid $300M~ for Todd Energy.

In addition to this, the company continued to pay out not only its base dividend but special dividends of $0.50 every quarter in 2024. These acquisitions should help bolster the company’s cash flow generation in the future, which ultimately should benefit shareholders.

However, it did likely cost some investors in terms of overall dividends paid in 2024. I’ve highlighted a chart below of dividend payments by Tourmaline over the years. We can see that 2022/2023 were big years. I expect the blue line to continue to tick upwards in 2025 if they don’t deploy as much capital towards acquisitions, but don’t expect it to get up near the levels seen in early 2023.

Total production, which is measured in barrels of oil equivalent, hit a record on the year, coming in at 579,173 BOE, an 11% increase year-over-year. NGL production and natural gas drove most of this increase, while oil production only increased by about 2%. I’ve highlighted a chart below of the company’s natural gas production, which is one of the more important KPIs of the business.

The company is still heavy in natural gas production and likely always will be, with 77% of production coming from this area. As a result, it is going to be more exposed to natural gas pricing. Because of the decline for the bulk of 2024, sales from the production of natural gas fell by 31%. Oil sales increased by 1%, and NGLs by 30%. Overall sales declined by 12%.

It is unlikely we see this same environment in 2025 unless natural gas takes a steep turn downwards. In fact, revenue will likely come in much higher. Realized prices for natural gas for Tourmaline fell by 30% YoY, but prices are, at this point in time, 35% higher than their realized prices throughout the entire year in 2024.

The company ramped up its free cash flow guidance for 2025, expected to now come in at $3.62 per share. This is significantly higher than their previous guidance, which ballparked FCF in the $1.1B range.

The company mentioned that it is in a “much better position to increase returns to shareholders in 2025 versus 2024,” likely meaning acquisitions may be taking a back seat and most cash flows will be paid back to shareholders via dividends or share buybacks.

However, Tourmaline has not been a company that is known for buying back shares, so I’d put my money on large special dividends in 2025.

If acquisitions come along, however, don’t be surprised if the company chooses to act. As an industry leader that generates a substantial amount of cash flow, it can continue to deploy that cash flow into acquisitions in order to fuel increased shareholder returns in the future.

Overall, it was a relatively rough year for Tourmaline in 2024, but this was due to nothing more than poor natural gas pricing, not operations. It should be in a good position to drive strong returns in 2025 if prices continue to accelerate or even stay where they are now.