Market Overview

The month of July is off to another strong start. Through the first couple of weeks, the TSX Index is up by 3.53% and is en route to its fourth consecutive month of gains. The Bull List is once again proving how it outperforms when the markets are in a bull run. Month to date, the Bull List is up by 4.87% and it is now nearing break even on the year (-2.42%). Our Dividend Bull list is slightly underperforming, up by 2.34% in July.

Thus far, every stock across our Bull Lists but two are in the green in the first half of July. NFI Group (TSX:NFI) and Polaris Infrastructure (TSX:PIF) are the only ones in the red with losses of -0.78% and -1.66% respectively. There has been no notable news of note, and no reason to be concerned here.

In terms of gainers, most performed quite well. TFI International (TSX:TFII) is continuing its strong run. The company is up by 10.06% in July and is now up by 21.18% on the year. The company has been one of the strongest non-tech companies on the TSX Index. Despite the run up, we still believe it has room to grow. It is currently trading at only 14 times forward earnings, 0.87 times sales and 2.42 times book value.

Another outperformer, Kirkland Gold (TSX:KL) is riding strong gold prices. Kirkland Lake remains one of the best valued in the industry and there is plenty of upside in the gold sector. Our Top 20 is littered with gold stocks for a reason.

We expect strong growth rates in the industry will be sustained by the high price of gold. Speaking of which, consensus is that the price of gold will be sustained for some time as the economic outlook looks bleak. On Wednesday, the Bank of Canada announced it expects GDP to drop by 7.8% in 2020.

Shifting focus, we have our eyes on Dividend Bull List pick Capital Power (TSX:CPX). The company is reporting earnings on July 30, and it is typically at this time of the year that the company announces its annual dividend raise.

Will it raise? Management seems optimistic. In the last quarter it had this to say:

“Based on our forecast, we are on track to be near the midpoint of our 2020 AFFO target range and on track with our dividend growth guidance while continuing to monitor the impacts from the COVID-19 pandemic.”

Capital Power has a targeted dividend growth rate of 7% through 2021. Considering its statement, it will be disappointing if the company does not announce a raise by the end of the year.

*Mat Litalien is long TFI International and Capital Power. Dan Kent is long TFI International and Kirkland Lake Gold.

Genx Portfolio Reviews

As we move forward with our semi annual portfolio reviews, we hit our GenX batch of portfolios.

Although these portfolios haven’t performed as well as our Millennial ones (you can read their review here) they’ve still performed admiringly well, with two portfolios extensively outperforming our benchmark index, the TSX, since inception on December 27th 2018.

If you remember from our Millennial reviews, we felt Shopify was at a price point where we couldn’t wait until these reviews to sell of some positions in both these portfolios and the Boomer portfolios. It turned out to be wise, as the stock has fallen nearly $140 a share since.

As such, we’ve got some cash available in the GenX Moderate and Aggressive portfolios. So, lets get started!

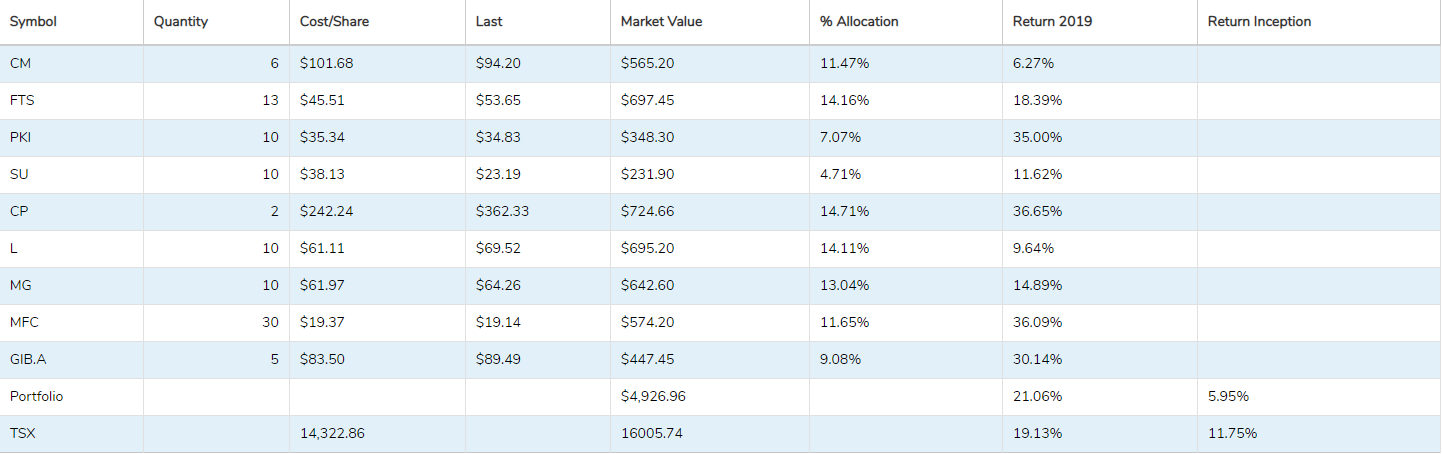

GenX Conservative

The GenX Conservative portfolio is actually the worst performing portfolio here at Stocktrades Premium, and one of the only ones not outperforming its benchmark.

Canadian Imperial Bank of Commerce (TSX:CM) and Manulife Financial (TSX:MFC) make up around 22% of the portfolios equity allocation, while Parkland Fuels (TSX:PKI) and Suncor Energy (TSX:SU) make up around 12%.

Overall, low exposure to tech (around 9% allocation with CGI Group (TSX:GIB.A)) and 34% exposure to the Canadian oil and gas and financial sectors and you have the reason for the portfolio’s underperformance.

However, most of the companies in this portfolio continue to pay dividends, and that is primarily what this conservative portfolio is hoping to achieve, is solid income. The portfolio consists of industry leaders like Canadian Pacific Rail (TSX:CP), Magna International (TSX:MG) and Fortis (TSX:FTS), all of which are dependable income companies.

The only one to cut its dividend has been Suncor, and it’s actually been the worst performing stock in this portfolio by a landslide. As a result, it’s total allocation has dropped to around 4.5% of the portfolio. We’re not comfortable selling Suncor off at this low of levels, but with the dividend cut coming so fast, we don’t have much confidence in the company moving forward either.

If you’re looking to model after this portfolio, we’d suggest going with another major Canadian producer as an alternative, like Canadian Natural Resources (TSX:CNQ) or Imperial Oil (TSX:IMO), two companies that have kept the dividend going.

Overall, there isn’t much to do with this portfolio besides wait for an economical recovery. We’d expect stocks like CM, SU, PKI, MG and MFC to continue to lag the overall markets moving forward. However, if collecting income is a priority for you, which it should be if you’ve chosen a conservative approach, then this portfolio is doing just fine.

We’d expect volatility moving forward to be less than its GenX counterparts.

No changes will be made to this portfolio at this time.

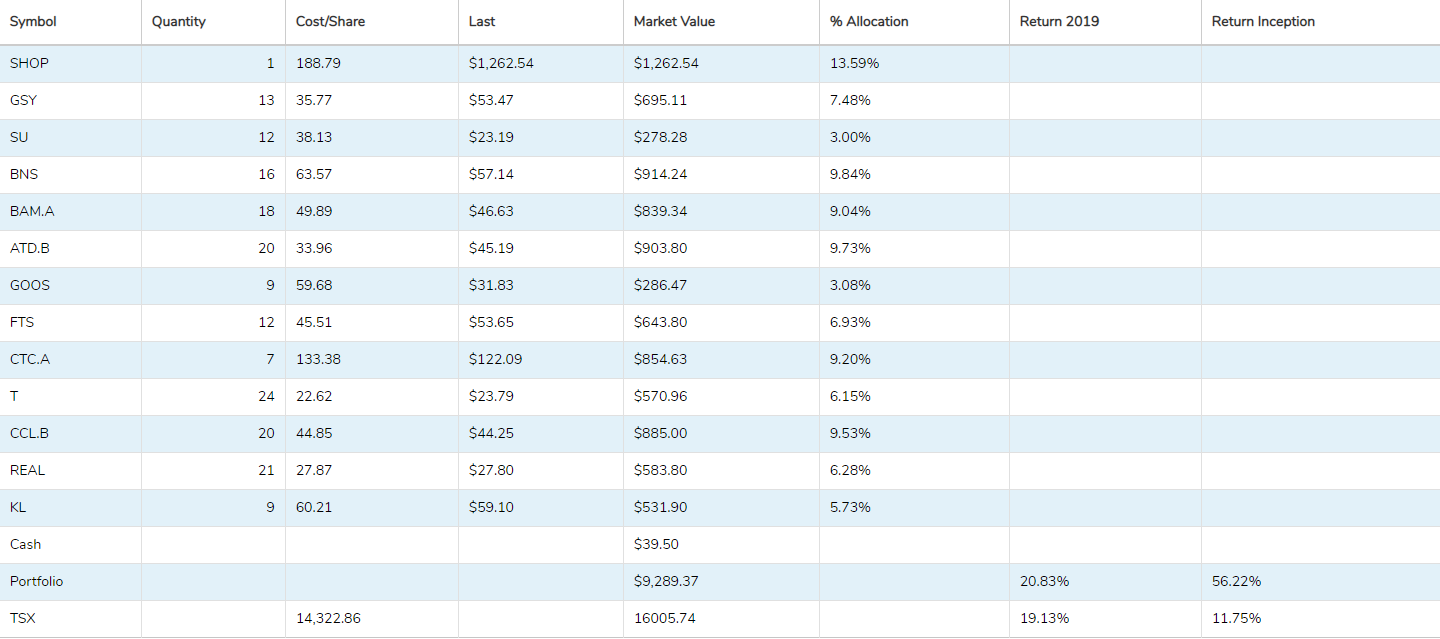

GenX Moderate

The GenX Moderate portfolio has posted returns of 56.48% since inception, outperforming the TSX by over 4500 basis points. This significant outperformance was led by strong investments in Shopify (TSX:SHOP), Alimentation Couche-Tard (TSX:ATD.B) and Goeasy Ltd (TSX:GSY).

Again, Suncor is an issue in this portfolio with not only a dividend cut but a steep drop in price, and although hindsight is always 20/20, we optimally would have went with Canadian Natural Resources in its place. Nonetheless, we’ll hold on to Suncor now until the company recovers in price, and maybe provides a boost to its slashed dividend.

Despite this portfolio’s outperformance, it contains a few stocks that are lagging the overall market in terms of returns. Bank of Nova Scotia (TSX:BNS), Brookfield Asset Management (TSX:BAM.A) and Canadian Tire (TSX:CTC.A) have all been hit hard by the COVID-19 pandemic, and we’re actually going to take this opportunity to add to all three stocks.

As we mentioned in the Millennial reviews earlier this month, we sold 2 shares of Shopify on July 1st for $1397.61. The portfolio had a little extra cash in it as well, so we’re currently sitting with just over $3133.10 in cash.

Sale – 2 shares of Shopify (On July 1)

Purchase – 3 shares of CTC.A @ $120.89 for a total of $362.67

Purchase – 6 shares of BNS @ $57.11 for a total of $336.66

Purchase – 8 shares of BAM.A @ $46.86 for a total of $374.88

We’re also looking at adding a defensive option that’s trading significantly below 2020 highs, and that is CCL Industries (TSX:CCL.B). The company is one of the highest ranked dividend stocks on our dividend safety screener, and it’s been extremely reliable over the last two decades.

Although it’s yield is small at 1.64%, the company has raised dividends for 18 straight years and has a 5 year dividend growth rate of 25.32%. If you’re unsure of what CCL does, they create labels, media products, label solutions and film materials.

They supply product to reliable industries such as healthcare, automotive markets and consumer packing. The company’s Return On Equity of 16.5% is one of the best in the industry and with a current ratio of 1.8 (nearly 2 times more current assets than current liabilities, indicating strong short term health), we believe the dividend is safe.

To add to this, the company is trading at a 33% discount to both its 5 year price to sales average and trailing price to earnings. CCL Industries is a strong value and dividend growth play, perfect for this medium risk portfolio.

Purchase – 20 shares of CCL.B @ $44.85 for a toal of $897

Another purchase in this portfolio will be to gain more exposure to tech due to our selloff of Shopify, and is actually one of our most recent Bull list additions, Real Matters (TSX:REAL).

The Bank of Canada just recently announced it will maintain current interest rates, which bodes exceptionally well for the housing market. With Real Matters being a tech stock that focuses on the real estate sector, the company should be able to continue to drive top and bottom lines like it has been doing recently. We won’t speak much on the stock inside of this review, as we have a full report on it here.

Purchase – 21 shares of REAL @ $27.87 for a total of $580.50.

And finally, as you saw in our Millennial portfolios, it’s very important to have exposure to gold right now. With the economy predicted to perform poorly over the short to mid term, gold is set to outperform. As such, we’ll be adding a relatively small position of Kirkland Lake (TSX:KL) to this portfolio. Again, considering Kirkland Lake is a recent Bull list addition, we won’t speak on it much inside of this review. Instead, you can read the full report here.

Purchase – 9 shares of KL @ $60.21 for a total of $541.89

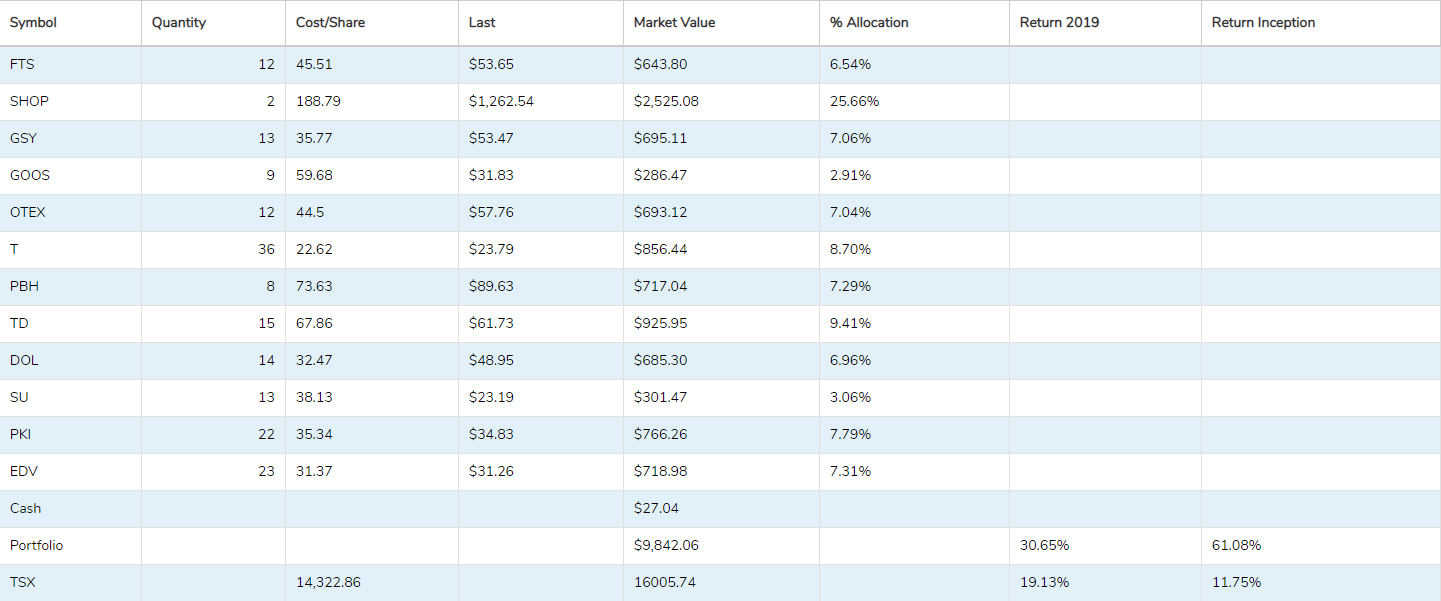

Genx Aggressive

The Genx Aggressive portfolio is another model portfolio that has performed exceptionally well, with overall returns of 55.71% compared to 12.09% of its benchmark index, the TSX.

The stock contains a large amount of exposure to the Canadian tech sector with positions in Shopify and OpenText (TSX:OTEX) and it also holds some of the strongest growth plays in the consumer staple sector as well with Dollarama (TSX:DOL) and Premium Brand Holdings (TSX:PBH).

As with our other GenX portfolios, a dividend cut and a significant dip in price for Suncor has caused the position to shrink to only 3.17% of the portfolio, but we’re comfortable with that right now. Canada Goose (TSX:GOOS) is also another stock very prominent in these portfolios, yet it has struggled significantly due to COVID-19 and China unrest. However, we have confidence in the stock moving forward, as it has been one of our longest standing Bull list stocks.

Our first order of business in this portfolio will be topping up our position in Telus (TSX:T). Telus is a foundational pick here at Stocktrades for 2020 and the stock is currently trading at a 5% discount to its 5 year average price to sales, and a 10% discount in terms of trailing price to earnings. As one of the more pure-play telecom companies as well, we feel Telus is the best exposure to both the emerging telehealth and 5g sectors.

Purchase – 10 shares of T @ $23.74 for a total of $237.40.

And with more top ups, we’ve decided to add to our TD Bank and Parkland Fuels positions. As of right now, the Canadian economy and the price of oil is holding both these stocks back. We know adding to these positions, patience will pay off eventually. Both are rock solid companies.

Purchase – 7 shares of TD @ $61.83 for a total of $437.24

Purchase – 9 shares of PKI @ $34.70 for a toal of $312.30

Like most of our other portfolios, we’ll be adding gold exposure to the GenX Aggressive as well. However, instead of Kirkland Lake we’ve decided to go with a more aggressive play in Endeavor Mining (TSX:EDV).

Endeavor recently purchased a company that Stocktrades Premium members who were around in early 2019 would remember, SEMAFO. SEMAFO is an African mining company and was a Bull List pick last year. The purchase ended up being very lucrative for shareholders who purchased in early 2019. After the acquisition, Endeavor broke into our Top 20 stocks and has been in the top 5 for the last couple of weeks.

In terms of forward estimates, the stock is undervalued. The company is looking at forward production of over 1 million ounces, with all in sustaining costs in the $845-$895/oz range. If the company can hit these production targets, it stands to generate significant cash flows. So much so that we could realistically expect a dividend from the company fairly soon.

Purchase – 23 shares of EDV @ $31.37 for a total of $721.51

**Writer Daniel Kent is long GOOS,SU,PKI,TD,T,KL,BNS,CTC.A,MFC