What is a SPAC (PART 1)

Given the strong response to our IPO Centre, we figured now would be a good time to introduce readers to the concept of the SPAC (Special Purpose Acquisition Company). These stocks are all the rage south of the border and have led to some pretty significant gains.

You might have heard of companies such as Multiplan, Fisker and Hyliion which are all high-growth companies operating in disruptive markets. They are all being taken public via one of the U.S.-listed SPACs. Trading in these SPACs has been considerable, and lots of new investors are jumping into these without a full understanding of what they entail.

Although some are working out, many more are falling flat.

So what is a SPAC?

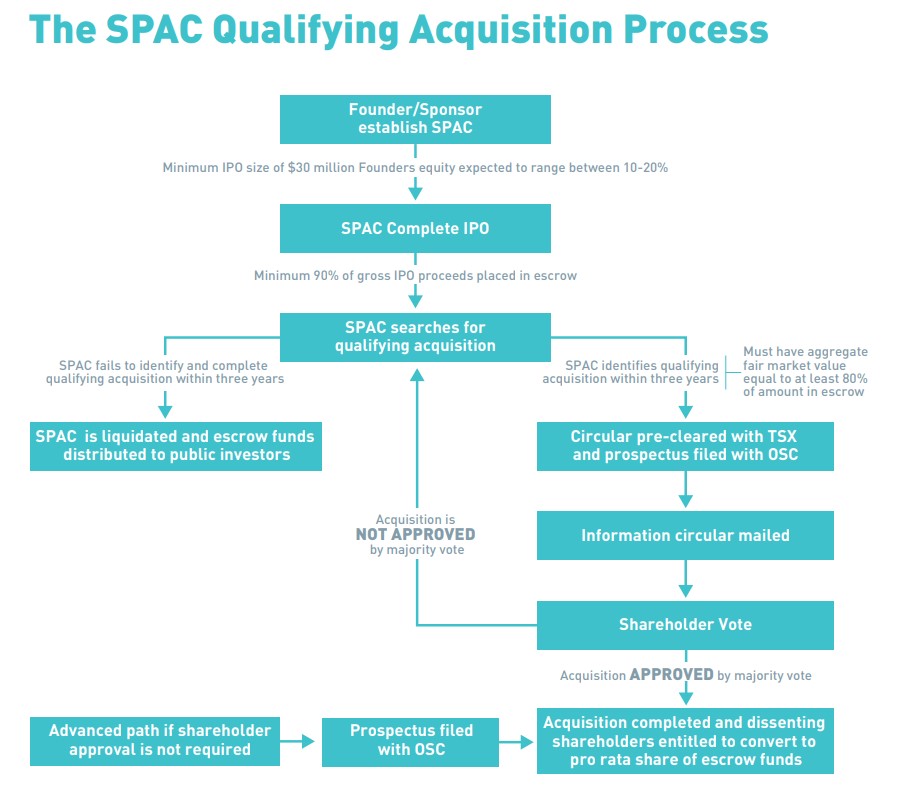

Also referred to as a “blank cheque” company, they are created to raise money through an initial public offering (IPO) to buy another company. In some ways, it is similar to private equity in that the SPAC raises funds (via IPO), and a team of experts then uses those funds to make an acquisition.

The money raised in the IPO is put into a trust account and is to be used only to make an acquisition or to return money to investors in the event the SPAC is unable to close on a deal.

Typically this amounts to 90% of the funds raised, the remaining 10% is often used as working capital for the company. It is important to note however, that SPACs have no existing business strategies or operations.

There are several benefits to going public via SPAC

For the company being acquired, it enables rapid expansion through quicker and more efficient capital than your typical IPO. It also provides retail investors a unique way to get in on the ground floor in some of the private, high-growth companies that they typically would not have access to.

Finally, there is a requirement that the Founders equity be between 10-20% of the IPO and must not sell their stock until the completion of the acquisition. The specific terms are found in the prospectus.

This however, is a positive as it means those who have initiated the SPAC have skin in the game.

How does it work?

Typically, the SPAC files a prospectus which includes how much capital in intends to raise ($30M minimum for TSX), how many units it intends on selling (minimum 1M) and the price per unit.

A Unit is comprised of one common share and at most two Warrants. A stock Warrant enables the holder to purchase a common share at a future date, at a given price.

In Canada, each Unit must be priced at a minimum $2.00 per unit, and there can be a maximum of 2 warrants per unit.

The most common instance we’ve seen lately are units priced at $10.00 which consist of one share and one, or one/half warrant.

Example: 1 Unit = 1 Common Share + 0.5 Warrants @$11.50

In this case, an investor who buys into the IPO with $1,000 would have 100 Units.

This means that the 100 Units would include 100 Common Shares and 50 full Warrants. These warrants give the holders the rights to buy the common shares at a price of $11.50 per share.

Once the transaction closes, the Units begin trading on the TSX Index under a pre-determined symbol with a “XXX.U” at the end of the ticker.

After a set period of days, the Units split into the Common Shares and Warrants (XXX.W) of the SPAC. Up until this time, when investors purchase the SPAC Unit on the open market, they are locking in both the common shares and warrants. Once this deadline passes, then investors are either buying the common share or the warrant.

Strategies of a SPAC

Each SPAC will have a different strategy, and that strategy is typically laid out in the prospectus and subsequent releases.

For example, Canada’s most recent SPAC is targeting the financial sector, and the alternative lending industry in particular. It is also important to note, that the sponsors cannot launch the IPO with a deal already in place and they aren’t necessarily bound to make an acquisition in that industry.

There is typically an ‘out’ clause here, but they would lose credibility very quickly if they shifted strategies.

Once the IPO transaction closes, the team has 3 years (36 months) in which to make an acquisition. In the event no acquisition is made, all the money in the interest-bearing escrow is returned to the shareholders.

It is important to note, that this applies only to the common shares and not the warrants. In other words, if the IPO price was $10.00 per unit, shareholders would receive close to, or all the $10.00 per share in cash in the event management fails to make a deal.

****The Warrants expire worthless****

This is an important distinction to make, and one that has left many SPAC investors with 100% losses on their investments. If you are going to invest in the warrants, be prepared to lose your initial investment.

Furthermore, it doesn’t matter what you pay for the shares on the open market – the shareholder is only entitled what is in escrow, which is close to the initial IPO price.

In our example, that is $10.00 per share. On the one hand, if you are paying $15.00 per share and they fail to land a deal, you are only getting ~$10.00 back in return.

Throughout the life of the SPAC, it may or may not indicate certain targets it is looking at acquiring. It will also issue non-binding letters of agreement which typically drives price movement. This gives investors insight into the potential acquisition target as the two sides conduct their due diligence. Since it is a non-binding letter, one or both parties may walk away.

Usually, there is upside to the stock when a non-binding letter is in place.

The closer the company gets to an acquisition, the higher the stock price climbs

If they walk away however, the price drops down to around IPO levels.

In the event the SPAC signs a binding letter of agreement to purchase a company, then formal approval process will begin. This typically requires the SPAC to receive public shareholder approval. We single out “public” for a reason as the Founders are unable to vote. The acquisition must receive majority approval from public shareholders.

If the majority decline, then the transaction will not proceed. If it does receive approval, then those who voted against will have the option to convert their securities for their pro-rata portion of the escrow funds. Once the transaction is approved, then the SPAC and acquired company merge into a TSX listed company – likely under a new symbol.

In this case, the share price is likely to rise as the markets will view it as a ‘good’ deal. If it wasn’t, the shareholders would likely vote against the deal.

Here is a nice chart to summarize these points:

Should you invest in an SPAC?

As you can see, these are for investors with a higher risk profile. Investors are essentially banking on a team to make a viable and attractive acquisition. In the event, the SPAC fails – investors have essentially locked up all that capital for no gains. Worse yet, if they bought at a higher price on the open market, then they are likely in the red.

In the SPAC space, a strong management team and one that is well capitalized is critical. If there are insufficient funds, then it is likely to get outbid for attractive targets by larger funds and pension plans – this is especially true here in Canada.

Research south of the border suggests that those SPACs which are larger market cap outperform those with a smaller market cap. Furthermore, management teams which have closed on previous SPAC acquisitions are more likely to be successful than those who are first-time Founders.

Let this digest for a moment – this was a lot of information to process. Next week, we will talk about the Canadian SPAC market and current TSX-listings.