Before we dig into this week’s newsletter, I want to give another routine warning about potential social media scams.

There are many people that try to imitate me. Whether it’s on X, Facebook, Discord, or any other social media platform. One of the things (but certainly not limited to this) that they will tell you is that you can copy my trades and profit.

The scammers try to convince you to make a deposit and then they report fake gains in your account. They do this in an attempt to get you to deposit more money. If you ever try to make a withdrawal, you will never get your money.

Please know that I will NEVER direct message you on any social media platform or Discord. Ignore these messages, as I do not want to see members lose money to such horrible scams.

With that said, let’s get into it.

Budget 2025 and the potential tailwinds for particular stocks

This will not include any political arguments for or against the budget. Whether you agree with the levels of spending or not, there isn’t much we can do besides get out and vote when the time comes.

However, from an investment point of view, there are a lot of interesting elements here. For right now, I’m going to focus on the large-scale infrastructure spending that is expected to come from this budget, and how two Bull List stocks are rock-solid ways to get exposure to the long-term tailwinds that should come from the spending.

In fact, both of these options were added to the Bull List previously because of an expected ramp up in infrastructure spending.

If we look to the chart below, we can see a total of $115B in investments over the next 5 years in infrastructure. So, it looks like this thesis is coming true.

However, it is important to keep in mind that this $115B is simply the government’s portion in terms of grants, incentives, and investments.

When we consider the impact this money would have on private corporate investment, it becomes even more attractive. Have a look at the table below. When we consider third party investment, infrastructure spending is expected to exceed $315B over the next half decade.

Public transit, green infrastructure, utility upgrades, data centers, roadways. All of these are expected to see a ramp up in capital.

Now, obviously there is execution risk here. The government needs private capital to make this happen. If corporations are not confident in making investments in Canada, they simply won’t make them, even on the back of government grants and subsidies.

But, I have a good feeling that the companies I’m going to speak about below are going to be net beneficiaries of extensive infrastructure upgrades in this country, and this is precisely why I own both and highlight both here at Stocktrades Premium.

WSP Global (TSE:WSP)

WSP is a Bull List Stock here at Premium, and one I own personally. If you’d like, you can read the full Bull List report on WSP here.

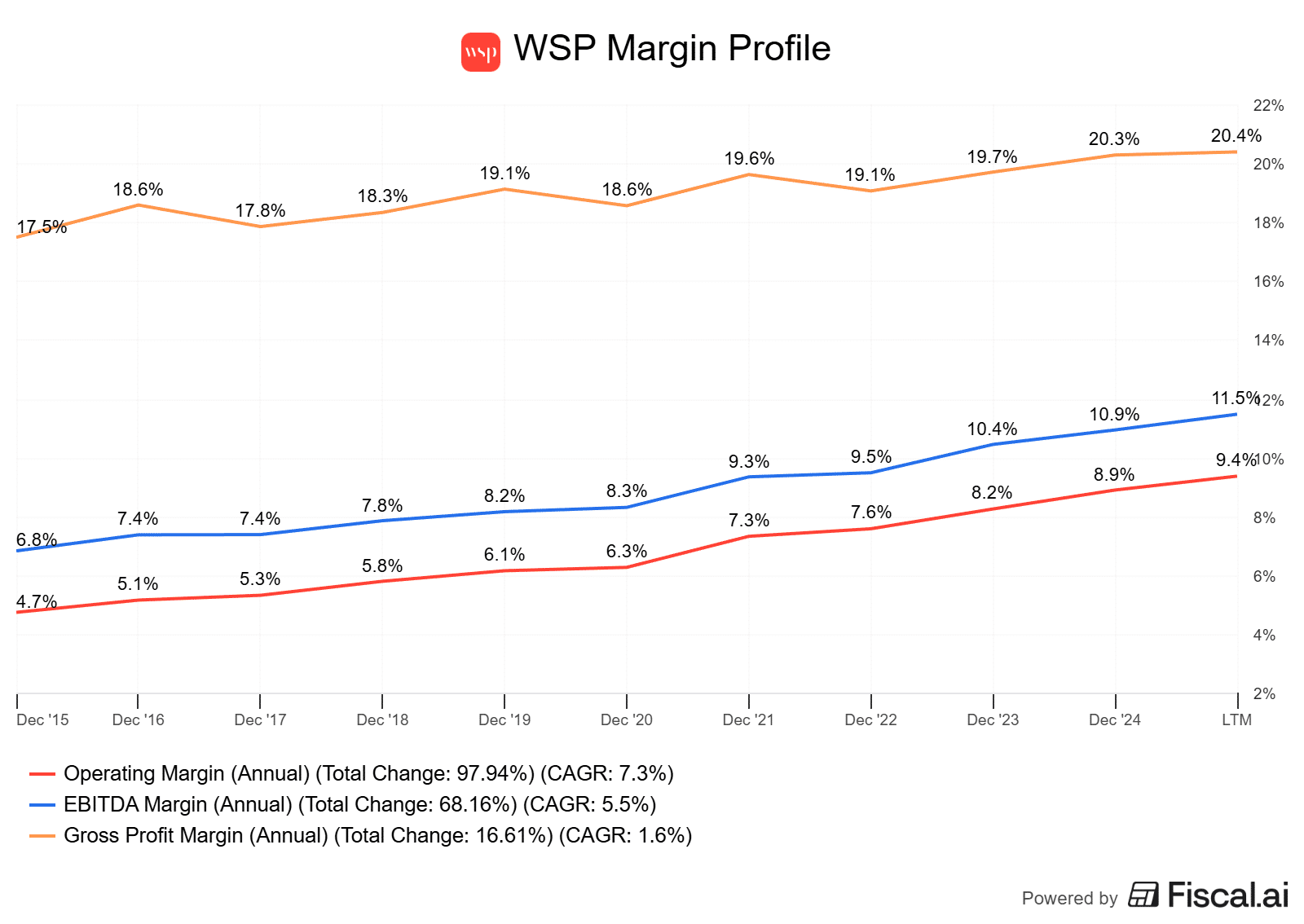

WSP earns its money through professional consulting, design, and civil engineering projects with predictable fee income. One of its main strengths is its scale. The company has a global reach, over 70,000 employees, and a strong public/private backlog and revenue base. In fact, it’s a near split as you can see by the chart below.

Budget 2025 leans heavily into sustainable infrastructure and public transit upgrades. This aligns well with WSP Global’s core strengths.

The opportunity rests in public‑sector contracts for transit, water systems, and city resilience programs. If Ottawa follows through on promised funding for public transit expansion and municipal upgrades, WSP’s local network of project offices gives it a clear delivery advantage as well.

This large-scale infrastructure rollout is about as good of timing as it gets for WSP. This is because the company is becoming much more efficient at picking up new contracts than it has historically. One of the main confirmations of this is the company’s backlog. It continues to grow by double-digits and now makes up 11 months worth of revenue.

WSP’s 2025–2027 action plan shows it is targeting more than a 40 percent increase in revenues and a 50 percent gain in adjusted EBITDA over three years, with free cash flow increasing more than 70%.

These goals seem a bit crazy for a blue-chip large cap. However, it is likely the company is expecting to secure a lot of new contracts in the coming years as well. Add this to the fact that margins are currently sitting at all-time highs and still expanding, and you have a recipe for success.

WSP’s mix of design & planning services along with ESG infrastructure consulting fits the budget plans almost perfectly. The swing factor is win‑rate. WSP needs to continue securing new major projects at the pace it has been over the last while. If it does, I believe there is market-beating potential here.

The company is having a rough year, which is a bit odd to me, as its results have been exceptional. However, I don’t really mind. It allows me to accumulate a rock-solid compounder at some of the more attractive valuations its traded at since the start of the pandemic.

Toromont Industries (TSE:TIH)

I’m not someone who focuses too much on charts or trends. However, when I added Toromont to the Bull List, a portion of the thesis was that when valuations got as low as they did when I added it, it tends to go on a large runup in price.

This looks to have worked out thus far, as the company is up 45%~ on the year.

The undervaluation thesis isn’t there anymore, but that doesn’t mean this company isn’t an outstanding option right now.

The swing factor now is how much of Budget 2025’s infrastructure build‑out converts into higher equipment orders. I believe this will happen.

Toromont makes money in straightforward ways: selling, renting, and servicing Caterpillar heavy machinery used across construction, utilities, and mining.

It also has a smaller segment, CIMCO, that designs, fabricates, and installs industrial and recreational refrigeration systems. Think of grocer refrigeration systems, and systems for skating and curling rinks. As you can tell by the booking chart below, it’s the smaller portion of the business.

On the equipment side of things, rentals and maintenance generate repeat cash flow and stabilize earnings when new builds slow.

The opportunity from Budget 2025’s infrastructure focus is fairly simple. Public infrastructure projects, transit builds, data centres, and utility upgrades will require an extensive amount of construction machinery.

If government spending lifts heavy equipment demand by even mid‑single digits, there are not a lot of players here in Canada that supply the equipment outside of something like a Toromont or a Finning. And there is little question that the government will be looking to funnel that money into Canadian corporations.

Now, some might be asking, why Toromont over Finning? Geography, primarily. Finning is the heart of the West. If we’re talking about oil and gas or precious metal mining, they excel. This is why they have done so well recently.

Let’s have a look at Finning’s exposure:

Now Toromont:

You’ll notice a key difference. Toromont holds the rights to the most important areas for this particular budget: Ontario, Quebec, and Atlantic Canada.

They control the population centers where the bulk of federal transit, housing, and healthcare infrastructure spending is targeted. When the government announces a massive transit expansion in the GTA or a new port terminal in Montreal, that money flows directly into Toromont’s backyard.

It is also important to remember the economics of this business. The “infrastructure ramp-up” doesn’t just boost revenue today. It locks in margins for the next decade.

When Toromont sells heavy machinery for a government project, they are effectively securing a 10-to-15-year stream of high-margin parts and service revenue. By accelerating the purchase of new fleets today, the government is inadvertently padding Toromont’s most profitable revenue lines for years to come.

So, how do we handle this stock now that the deep-value gap has closed? Fairly easy.

We shift our mindset from “turnaround trade” to “long-term compounder.” The easy money has been made, but the long-term money is just getting started, in my opinion.

Toromont is no longer a table-pounding bargain, but it remains a high-quality buy that is nicely aligned with the country’s policy moving forward.

The risks? Although Toromont does have a dominant share in the east, that does not stop competitors from targeting the same government contracts, pressuring bid margins. I don’t see this is as a detrimental risk, but it’s a risk nonetheless.

And in addition to this, if the construction cycle turns or public budgets tighten, fleet utilization could drop fast. Remember, the bulk of the government’s investments in infrastructure are through incentives and grants. We still need private capital to flow into Canada to kickstart a lot of these projects and get the economy rolling.

Overall, however, I am happy for this to be a company I buy and continue to accumulate over the years. It is highly likely to be a mainstay on the Bull List.

Wrapping it up

To wrap this up, I want to clarify why I chose to highlight these two specific companies out of the dozens of industrials that could benefit from Budget 2025.

When you look at WSP Global and Toromont Industries side-by-side, you aren’t just picking two random stocks; you are effectively buying the entire lifecycle of an infrastructure project.

WSP is the gatekeeper. They capture the federal dollars before a single shovel hits the ground.

They get paid to navigate the environmental assessments, design the transit lines, and manage the complex bureaucracy.

Toromont is the “muscle.” Once WSP gets the permits approved, Toromont steps in to supply the equipment that moves the earth and gets the job done.

Obviously, there are a lot more companies here that could benefit. For example, we can look to a company like Aecon (TSE:ARE), who would be the picks and shovels of infrastructure expansion. They’re the boots on the ground doing the actual work.

However, back to WSP and Toromont, you are effectively setting up a toll booth on the $315 billion (public + private) spend that we expect to see over the next five years. With WSP, you get paid during the planning phase. With Toromont, you get paid during the execution phase.

I know infrastructure isn’t flashy. It doesn’t move like a tech stock, and it certainly doesn’t offer the instant gratification we’re used to these days.

However, Canada is a massive, difficult country to build in. That difficulty is exactly what helps WSP and Toromont. It is incredibly hard for new competitors to come in and replicate Toromont’s parts network in Northern Ontario or WSP’s relationships with municipal planners. These are wide-moat businesses.

The risks I mentioned, that being execution delays and reliance on private capital, are certainly real. We all know that government announcements don’t always translate perfectly into reality.

However, the sheer volume of capital allocated in Budget 2025 provides a reasonable margin of safety. Even if only half of these projects break ground on time, the order books for these two companies are going to see positive benefits.

Ultimately, while the headlines argue about the deficit, I prefer to focus on who gets the contracts. In my view, these are the two names that could benefit over the next half decade.