Bull List Report – Jamieson Wellness – TSE:JWEL

Jamieson Wellness – JWEL.TO

Jamieson Wellness Inc is engaged in the manufacturing, distributing, and marketing of branded natural health products, including vitamins, minerals, and supplements. The company operates in two segments: The Jamieson brands and The Strategic Partners. The majority of its revenue comes from the Jamieson brand segment. Some of its brands are Jamieson, Progressive, Precision, and Iron Vegan. Geographically, The majority of its revenue is derived from the domestic market.

|

Focus area |

Score |

|

Valuation |

76 |

|

Profitability |

47 |

|

Risk |

22 |

|

Returns |

0 |

|

Dividend |

71 |

|

Outlook |

95 |

|

Debt |

50 |

|

Growth |

81 |

|

Overall |

62 |

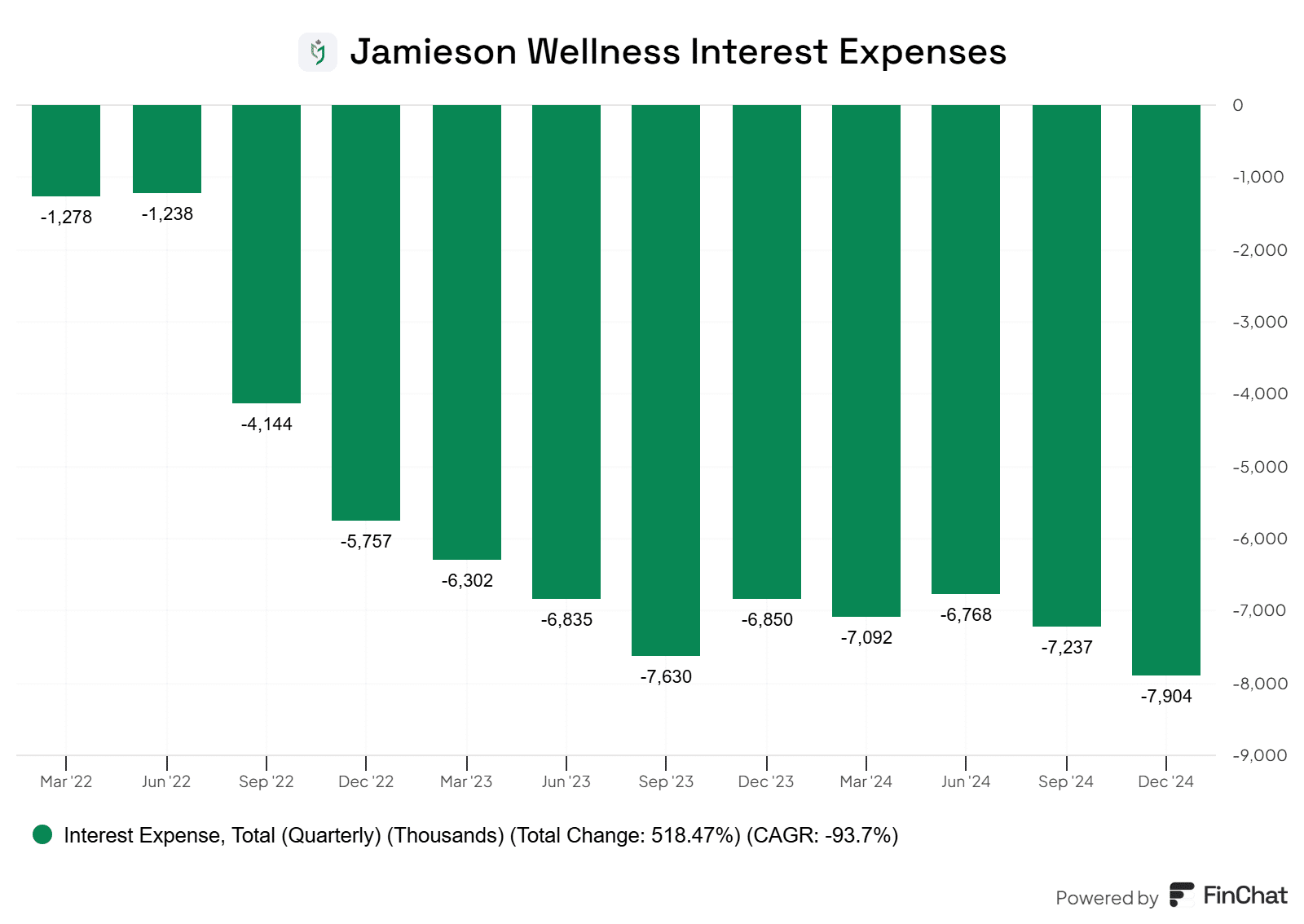

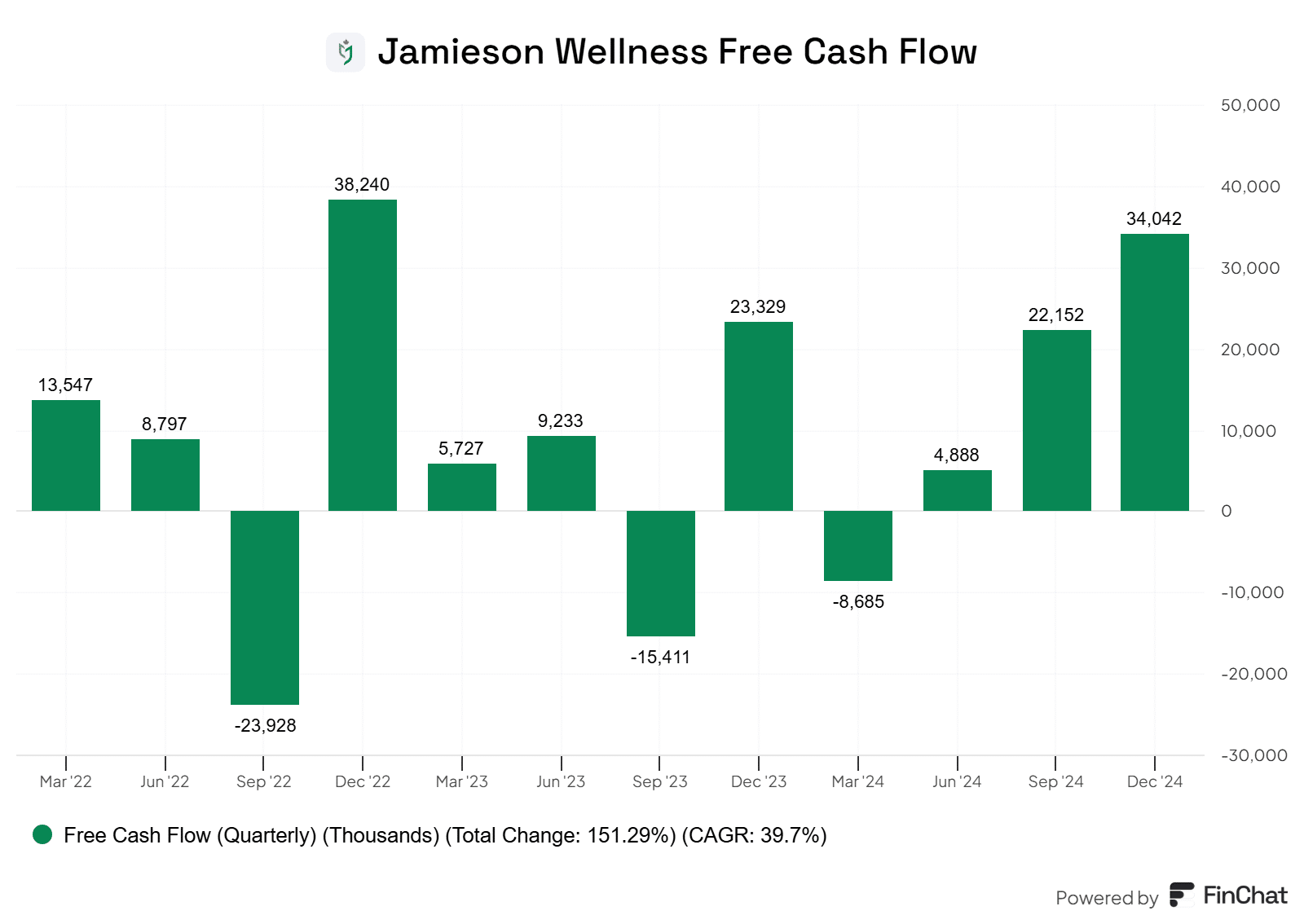

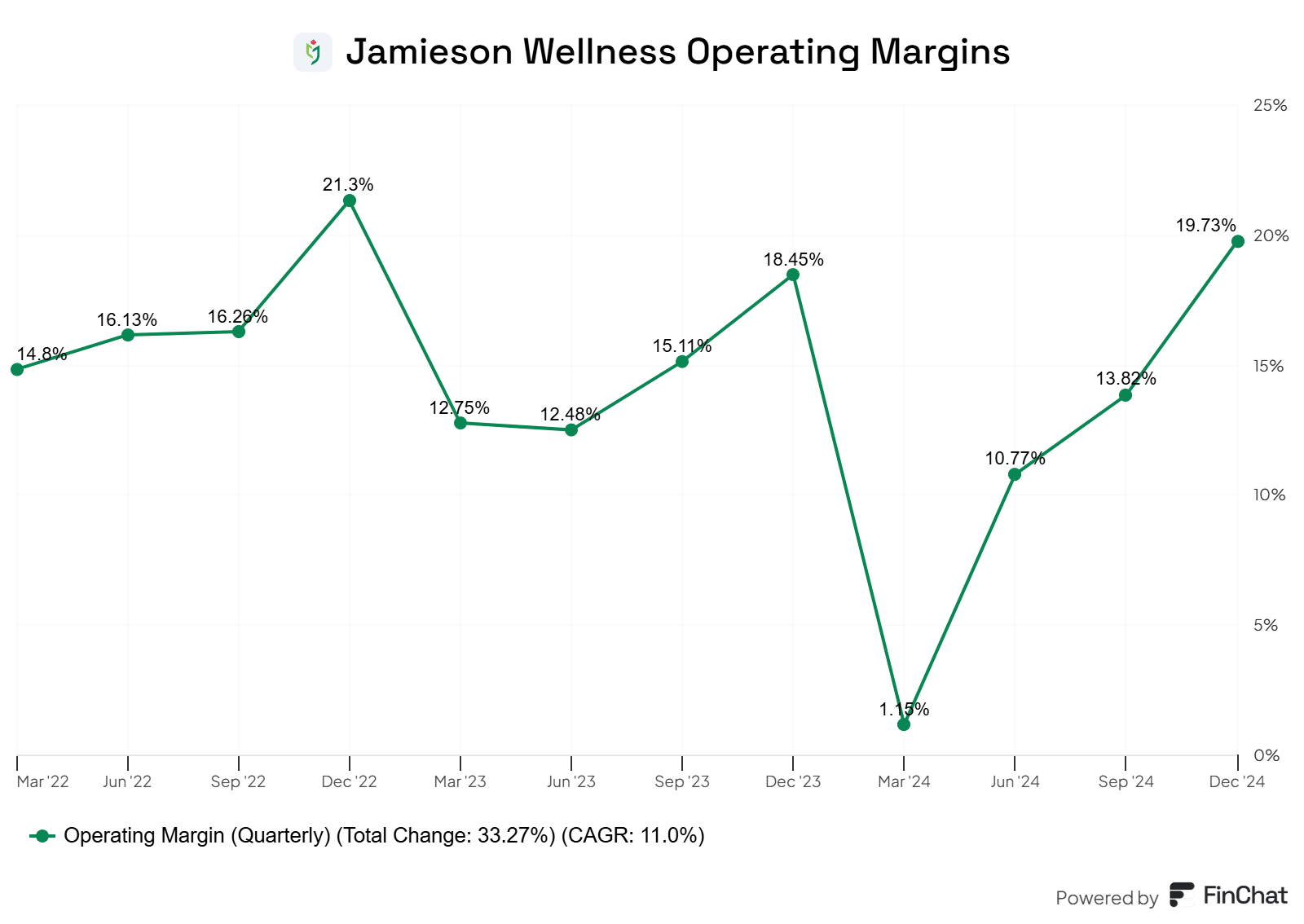

Unfortunately, Finchat does not track KPIs or Segments for Jamieson. However, I’ve placed some key data in the charts below to watch.

Disclaimer

By utilizing this report, you agree that you are a Stocktrades Premium member, and you agree to our terms and conditions and privacy policy. You acknowledge that any distribution of this report outside of Stocktrades Premium could result in the immediate cancellation of your Premium subscription. You also agree to the following:

This stock report is solely for informative purposes, and does not represent a buy or sell recommendation. The information expressed in this report is the opinion of the analyst about the subject company and our database of stocks in general. The information the analyst used to compile this report comes from sources we believe are reliable. Stocktrades Ltd however makes no warranties of any kind as to the completion or correctness of the information within this document.

All information in this report is accurate as of the date of this report, and all data contained within this report of the subject company is of the analyst’s best judgement at the date of the report. The information contained in this report is subject to change without notice. The information provided in this report is provided for informational purposes by Stocktrades Ltd and Stocktrades Ltd assumes no legal responsibility or liability. Anyone using this report assumes full responsibility for whatever decision is arrived at by using the details of this report.

Stocktrades Ltd. assumes no liability or legal responsibility for the resulting actions and or consequences of using outdated information. No version of this report outside of the original located at www.stocktrades.ca/premium/ is to be considered to contain live, or accurate information. These reports are updated quarterly and it is the users responsibility to insure they have the most recent updated version.

You may not alter or distribute this report in any way without the full consent of Stocktrades Ltd.

The decision to purchase or sell of a security depends on a multitude of individual factors such as but not limited to risk tolerance, financial situation, and investment objectives.