US Foundational Stocks

US Foundational Stocks

Previous data

Holdings

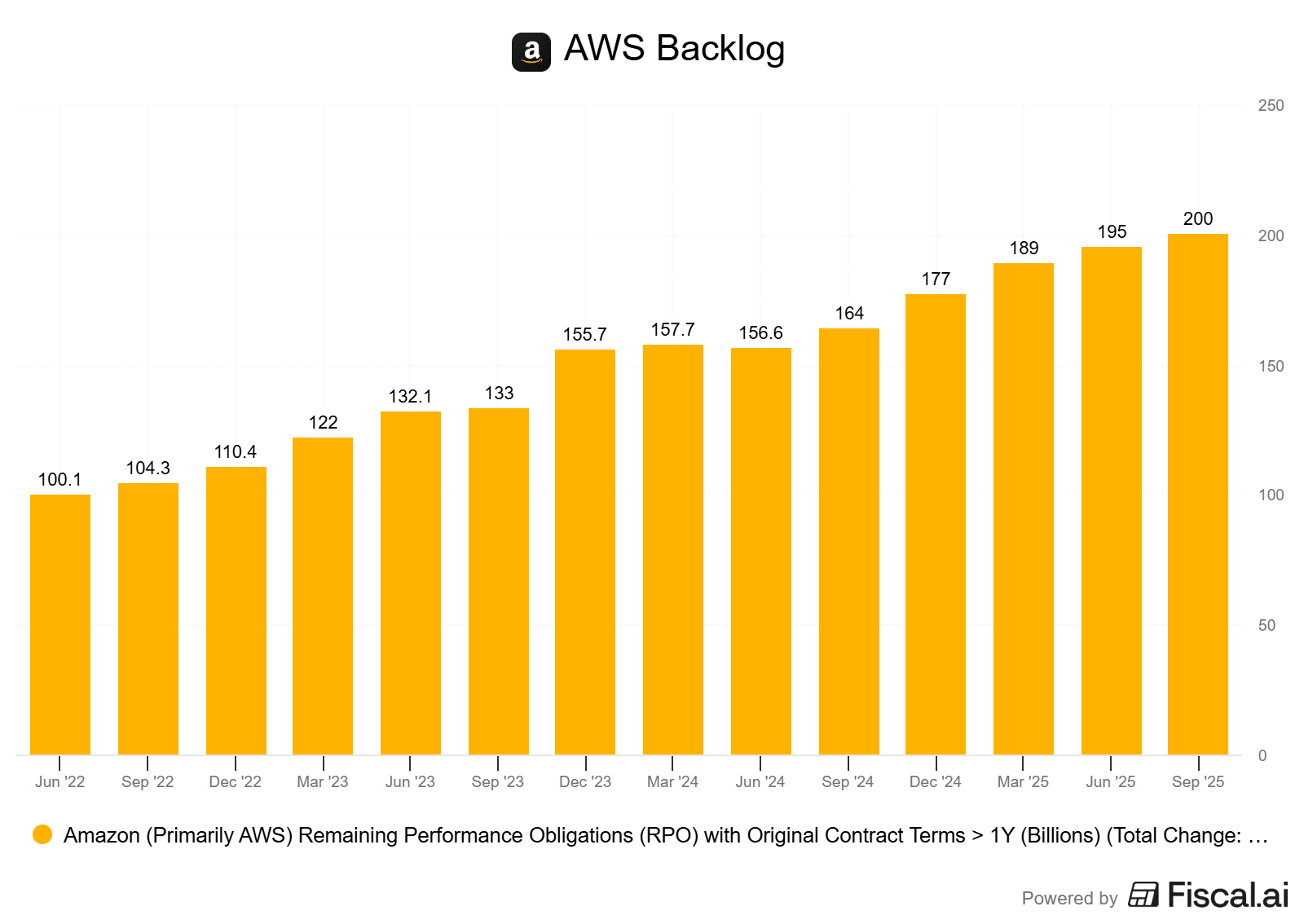

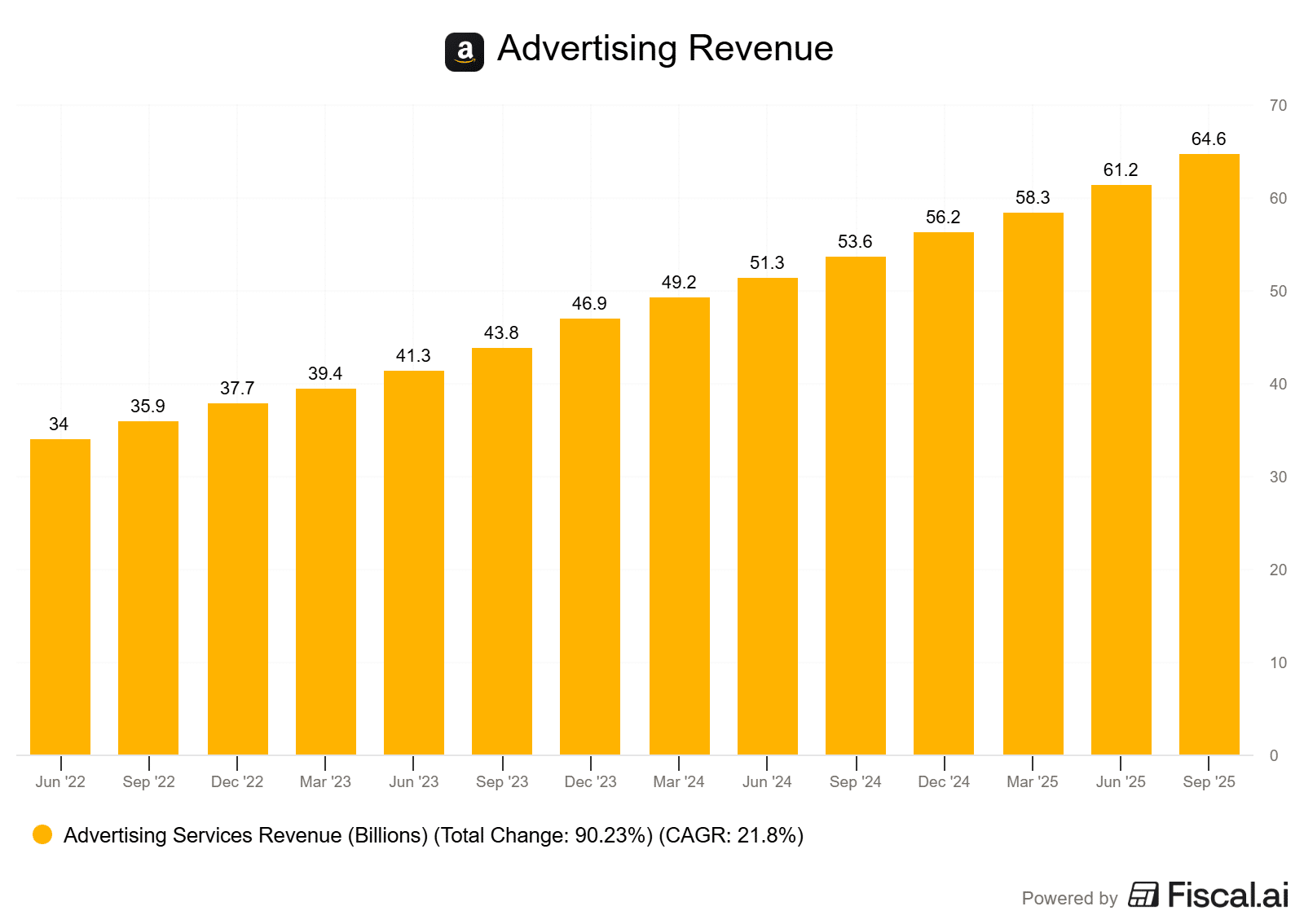

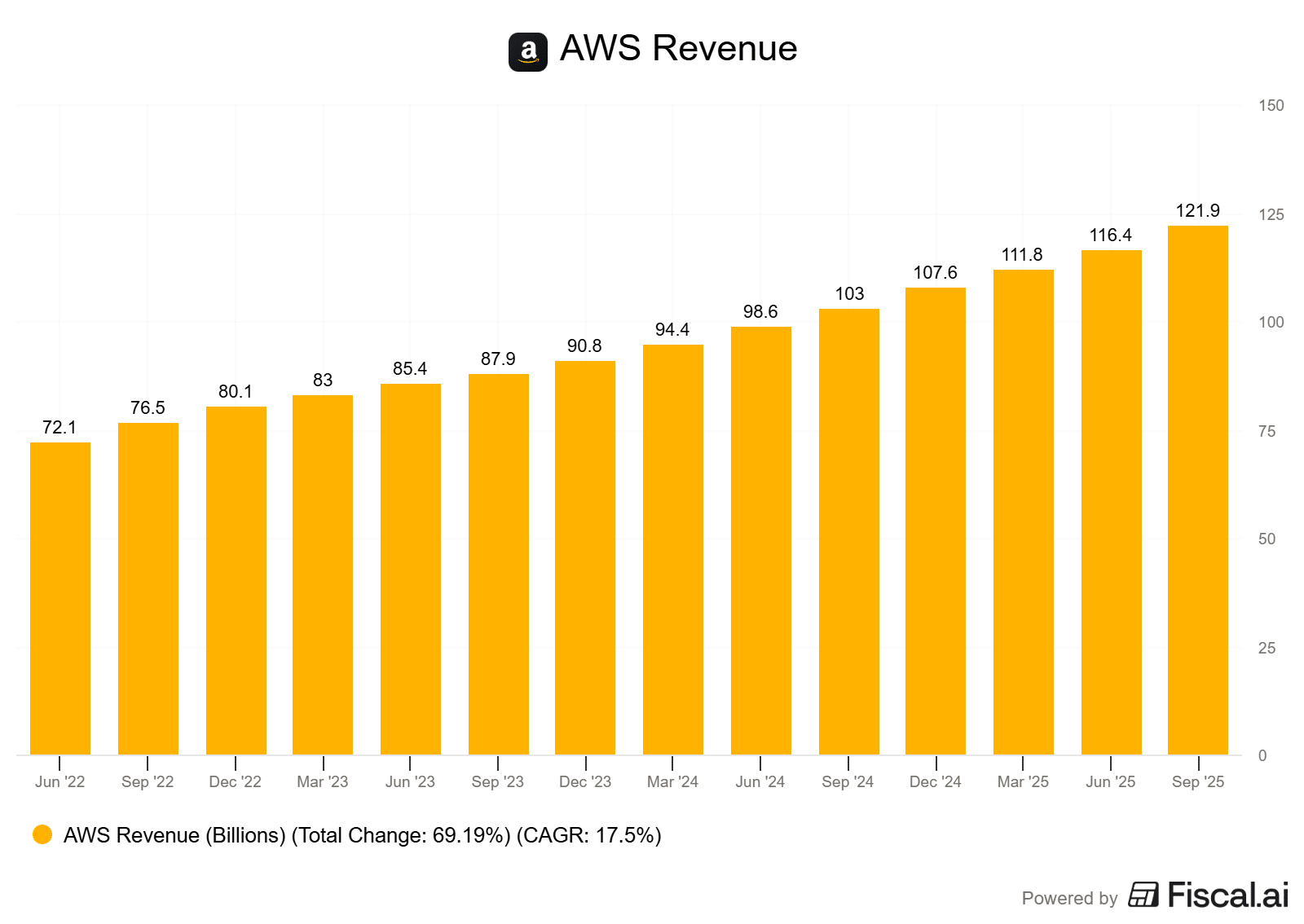

- Amazon (AMZN)

- Alphabet (GOOG)

- Home Depot (HD)

- Berkshire Hathaway (BRK.B)

- Blackrock (BLK)

- UnitedHealthcare Group (UNH)

- Starbucks (SBUX)

- Lockheed Martin (LMT)

- Pepsi (PEP)

- Visa (V)

Holdings

- Amazon (AMZN)

- Alphabet (GOOG)

- Home Depot (HD)

- Berkshire Hathaway (BRK.B)

- Blackrock (BLK)

- UnitedHealthcare Group (UNH)

- Starbucks (SBUX)

- Lockheed Martin (LMT)

- Pepsi (PEP)

- Costco (COST)

Holdings

- Amazon (AMZN)

- Alphabet (GOOG)

- Home Depot (HD)

- Disney (DIS)

- Blackrock (BLK)

- Pfizer (PFE)

- Starbucks (SBUX)

- Lockheed Martin (LMT)

- Pepsi (PEP)

- Costco (COST)

Holdings

- Amazon (AMZN)

- Alphabet (GOOG)

- Home Depot (HD)

- Disney (DIS)

- Blackrock (BLK)

- Pfizer (PFE)

- Starbucks (SBUX)

- Lockheed Martin (LMT)

- Pepsi (PEP)

Happy New Year! The updated list of US Foundational Stocks will be live on January 18th.

Changes from 2025

Pepsi (PEP) removed

The decision to remove Pepsi from the Foundational Stocks is no doubt because of a change in thesis. While the company’s ownership of both Frito-Lay and its beverage division was long considered a strategic moat (and the reasoning I added it to the Foundational List) that allowed it to outperform pure-play competitors like Coca-Cola, that same diversity has recently become the primary headwind in its removal.

Inflation forced aggressive price hikes across the snack portfolio, but unlike the relatively inelastic demand for beverages, snack foods reached a price ceiling that triggered a sharp decline in volumes. This decoupling proved that while consumers are willing to sacrifice the $2.50 for a Coca Cola versus the $2 it was pre-pandemic, the large price gap between a bag of Doritos and say Loblaw’s President’s Choice brand is simply too much. People are opting for the cheaper alternatives.

Beyond the immediate pricing pressures, the long-term thesis is also being challenged by the rapid adoption of GLP-1 weight-loss medications. These drugs specifically suppress cravings for the high-sodium and high-sugar products that make up the bulk of Pepsi’s food segment. When you combine this shifting health sentiment with the increasing quality and lower cost of “off-brand” snacks, the valuation historically given to Pepsi’s diversified model becomes much harder to justify.

Starbucks (SBUX) removed

Starbucks had been a long-term holding for me, and a company that performed exceptionally well for a long time. However, I believe it is a prime example of the fact that no company is truly a buy-and-hold forever.

Over the last few years, the business has faced some large operational setbacks. Some were beyond its control, such as large-scale inflation. This inflation caused a substantial cooling in terms of consumer spending. When groceries were accelerating in price by 9% a year, a simple way to cushion that blow was to cut out expensive lattes.

The company has struggled for a while now, and its removal from the Foundational Stock List would have come last year, had the company not hired former Chipotle CEO Brian Niccol to turn around its operations. Now, I am usually not one to invest in turnarounds whatsoever. Why? Because turnarounds rarely turn things around. The vast majority of the time, they will simply burn up a ton of cash trying to change the identity of a business.

However, Niccol was a situation of particular interest to me, as he had quite literally turned Chipotle around from a struggling business to one of the fastest-growing quick-service chains in the US.

Fast forward a year later, and Starbucks is still spinning its tires. There is next to no same-store sales growth, and the company’s lofty goals of turning this business around involve a lot of cash outlays, so margins are getting hit hard.

They could realistically still turn things around. However, my main concern here is that they will, as mentioned, dump a ton of money into the business with zero results.

Keep in mind, Starbucks is really not that bad of a company. The majority of struggles here are industry-wide. Let’s have a look at Chipotle:

The story is similar across the majority of quick-service restaurants. Consumers have just stopped spending money.

Yes, one could argue that the cheaper ones are surviving well. Look at Restaurant Brands International’s Tim Hortons segment. It is doing well. However, expensive QSR’s are struggling mightily.

2026 US Foundational Stocks

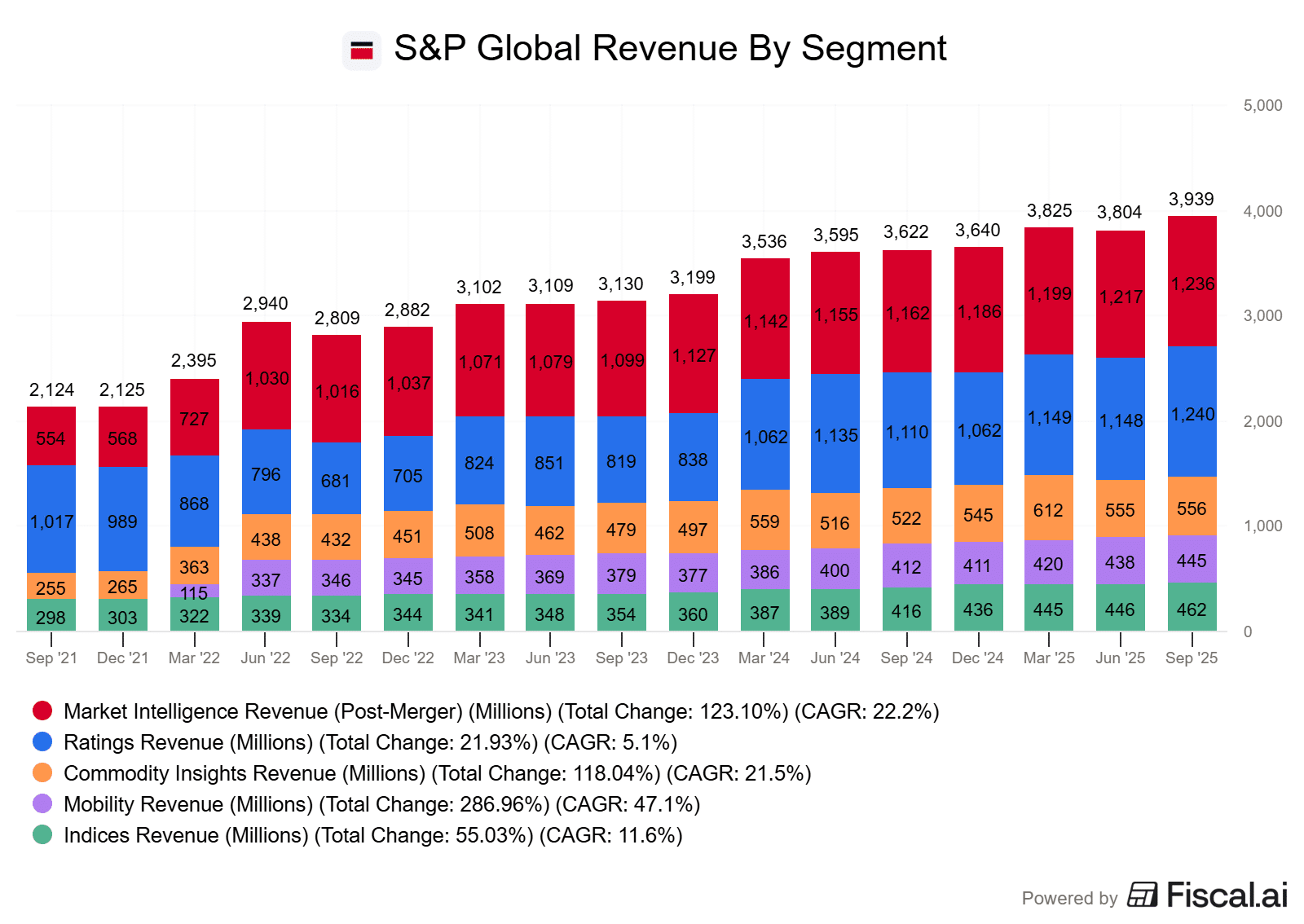

S&P Global (SPGI)

S&P Global, Inc. engages in independent credit ratings, benchmarks, analytics, and data to the capital and commodity markets worldwide. Its Market Intelligence segment provides multi-asset-class data and analytics integrated with purpose-built workflow solutions. The Ratings segment is involved in credit ratings, research, and analytics, offering investors and other market participants information, ratings, and benchmarks. The Commodity Insights segment focuses on information and benchmark prices for the commodity and energy markets. The Mobility segment offers solutions serving the full automotive value chain, including vehicle manufacturers, automotive suppliers, mobility service providers, retailers, consumers, and finance and insurance companies. The Engineering Solutions segment engages in advanced knowledge discovery technologies, research tools, and software-based engineering decision engines to advance innovation, maximize productivity, improve quality, and reduce risk.

Think of S&P Global (SPGI) not just as a company, but as a “toll collector” for the entire world’s financial highway. If a big company or even a government wants to borrow money by issuing bonds, they almost have to go to S&P Global to get a credit rating first. It’s essentially a requirement for them to get the best interest rates.

Because there are really only two or three companies in the world that everyone trusts to do this, S&P sits in an incredibly powerful position with a massive moat. It is nearly impossible for a new competitor to just show up and steal their business. Think of a new company entering the space and issuing credit ratings. Who is going to give those ratings any weight over a company like S&P, which has done it for decades? If you’re looking to get access to debt, you go to S&P or Moody’s for a rating. It’s that simple.

This isn’t just about debt, either. If you’ve ever invested in an S&P 500 index fund, you’re using their product. Every time an investment fund or a bank uses that famous “S&P 500” name to build a product, they have to pay S&P a fee. It’s an amazingly simple model. They own the benchmarks that the whole world uses to measure success, and they get paid just for being the gold standard.

What makes this a great long-term hold for regular investors is that it’s a sticky business. Once a bank or a hedge fund starts using S&P’s data and software (like their Capital IQ platform) to run their daily operations, they almost never switch. It’s too much of a headache to retrain everyone and move all that data, which gives S&P incredible pricing power.

They can raise their rates slightly every year, and most customers will just pay it because they have to. Plus, they’re currently cleaning up the business by spinning off their automotive data branch (the people who own CARFAX) into its own company. This is a smart move because it lets the main S&P business focus purely on high-margin financial data and indexing, which is where the real growth is, in my opinion.

Looking forward to 2026, S&P is also positioning itself to be the leader in the “private” side of the markets. Things like private equity and private credit that aren’t traded on a public exchange. They recently bought a company called With Intelligence to make sure they own the data for those markets too. You’ll notice a trend here at Stocktrades Premium, and that is if there is a major financial company that is diving deep into the private markets, it’s likely featured here. Brookfield (BN), Blackrock (BLK), and now S&P Global (SPGI).

Do I think private credit/equity are the best investments for retail investors? Absolutely not. However, they’re ridiculously popular right now, and are attracting a ton of capital from retail and institutional investors. So when I see institutions moving toward them, I know they’re “going to where the puck will be,” and not where it has been.

They’re also leaning hard into AI. In the case of S&P, it’s not just being used as a fancy word in its quarterly earnings. They’re using it to help analysts read through thousands of pages of financial reports in seconds, which makes their software even more valuable to the pros.

With a history of raising their dividend for over 50 years straight and a habit of buying back their own stock, they are a classic compounder with a large economic moat. You might not see it double overnight, but because it’s the essential infrastructure for global finance, it’s the kind of stock you can buy and let work for you for decades.

- Private Markets. For a long time, the best data was only available for public companies. Private markets had zero transparency. Today, more money than ever is flowing into “private” investments like equity or credit. And when this happens, people demand data for them. S&P Global recently spent $1.8 billion to acquire a company called “With Intelligence,” which is basically the “gold mine” of data for these private funds. As private markets continue to gain popularity, watch to see how S&P Global continues to leverage this.

- AI agents. A lot of tasks in the financial space were mundane, but necessary. The situation is changing here. S&P Global’s AI agents can perform complex tasks, like constantly monitoring 10,000 different companies for tiny signs of credit risk or automatically building a custom investment index for a bank. This makes their software, like Capital IQ Pro, so useful that financial pros can’t imagine doing their jobs without it. Keep tabs on how they continue to build this out in 2026, as it could be a real money maker for years to come.

- Direct Indexing. The new trend for 2026 is Direct Indexing. This is where investors or big institutions want a “personalized” version of the S&P 500. Maybe they want the index but without any tobacco companies, or with extra weight on tech. S&P’s new IndexBuilder platform allows these investors to create their own custom mini indexes in seconds. This turns their standard product into a premium service, allowing them to charge more for the same underlying data.

- Refinancing Cliff. Between 2020 and 2021, many companies took advantage of rock-bottom interest rates to borrow massive amounts of money. A huge chunk of that debt is scheduled to mature in the next few years. By 2026, debt maturities are expected to jump to nearly $3 trillion. These companies must refinance that debt to keep their businesses running. For S&P Global, this is a massive tailwind. Every time one of those companies goes back to the market to “roll over” their old debt into a new loan or bond, they need a fresh credit rating.

S&P Global’s business is relatively simple. There are no complex KPI’s to keep track of. For that reason, the best thing for you to keep track of is simply the revenue the company generates from each segment and how those segments are growing.

SPGI reports earnings in early February. At that point in time, I will provide commentary on its earnings.

Lockheed Martin (LMT)

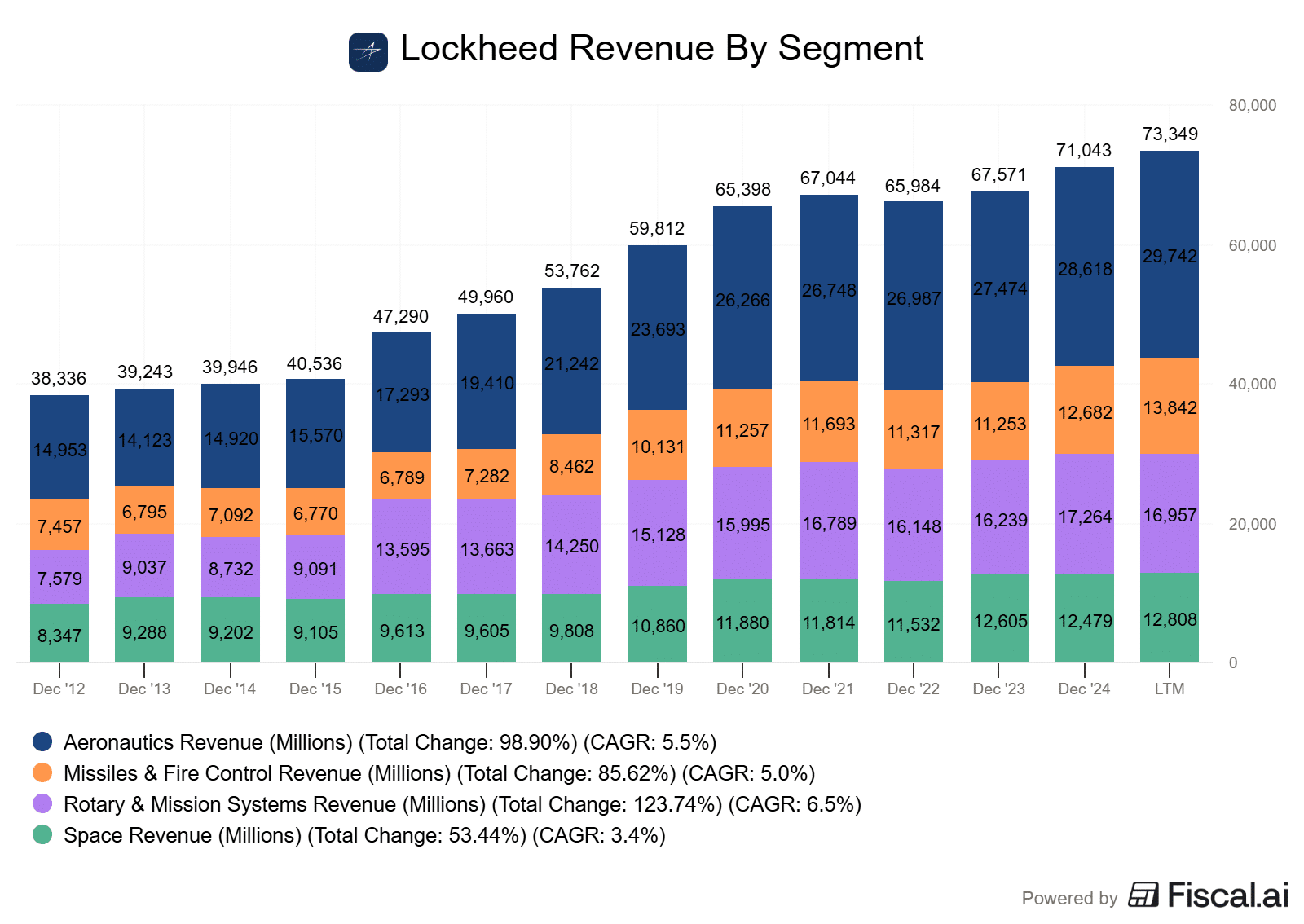

Lockheed Martin is the world’s largest defence contractor and has dominated the Western market for high-end fighter aircraft since it won the F-35 Joint Strike Fighter program in 2001. Lockheed’s largest segment is aeronautics, which accounts for upward of two-thirds of its revenue from the F-35. Lockheed’s remaining segments are rotary and mission systems, mainly encompassing the Sikorsky helicopter business; missiles and fire control, which creates missiles and missile defence systems; and space systems, which produces satellites and receives equity income from the United Launch Alliance joint venture.

The world seems to be stuck in perpetual conflict. This is why a company like Lockheed Martin deserves a spot on the Foundational Stock list. I am fairly confident that if it wasn’t for some comments Elon Musk made about the F-35 in late 2024, we would have a market outperformer over pretty much any time period in the last half-decade.

Now, different tailwinds are emerging for Lockheed. It has transitioned from a steady-state industrial play into an aggressive high-growth “Sovereign Tech” narrative, primarily driven by a short-term shift in policy from Donald Trump and the Republican Party.

As we enter 2026, the company is the primary beneficiary of a historic security premium, driven by the administration’s “One Big Beautiful Bill” Act and a recently ramped-up $1.5 trillion defence budget for 2027. This 50% increase in planned spending moves defence beyond a cost-management task and into an aggressive growth play with the US Military. Lockheed just so happens to be at the center of the “Golden Dome” Initiative for national air and missile defence.

I do believe the thesis for this company could potentially change by the next election in 2028. However, it is still intact today. Not only from a mind-boggling budget (the $1.5T mentioned) in the US, but also the US’s aggressive push toward allies and their spending.

The United States is pushing hard for NATO allies to match defence spending to at least 3.5% of GDP, and this acts as a mandatory “Export Supercycle” for Lockheed’s F-35 program. Why? Because no matter what Elon Musk says, the F-35 is one of the only fighter jets of its caliber that is available on a global scale.

This demand is met by significantly improved operations. Lockheed has struggled with software issues and bottlenecking inventory. However, both of these issues are cleared up, and Lockheed has proven it can handle high-rate production. The company’s backlog now sits at a mind-boggling $179B, the highest in its history. Sure, this isn’t guaranteed work. However, they have a good track record of converting their backlog to revenue.

While Trump’s rhetoric regarding executive pay and buybacks is a bit worrying, the trade-off is an unprecedented scale of long-term government contracts and state-funded expansions that provide a unique hedge against broader economic volatility.

NATO allies and other Western countries have long-established defence procurement practices that prioritize security, reliability, and interoperability. What I am trying to say here is that no matter the price, countries will stick to nations like the US for defence equipment over somewhere like, say, China. This creates a considerable moat.

Some investors simply don’t want to participate, profit, or invest in conflict. I have been asked the moral question about Lockheed’s addition to the Foundational Stock List numerous times. However, I leave the company here for those willing to buy shares in an outstanding compounder. For those who do not wish to participate, I understand entirely.

Lockheed’s continuation on the Foundational List is primarily a GARP (Growth At A Reasonable Price) play. My thesis has shifted from one of long-term to more mid-term, as I do expect Donald Trump to pull forward a lot of growth for this company due to his erratic nature and extensive spending. If the Republicans do not win the election in 2028, I expect this could be scaled back. But until then, I’m a fan of this company, and it remains a core position in my portfolio.

- NATO 3.5% supercycle – I’m monitoring spending shifts in Europe and the Indo-Pacific. As the U.S. pressures allies to reach a 3.5% GDP spending floor. Any new F-35 orders from holdout nations or fleet expansions from existing partners will signal that the export supercycle is accelerating.

- Trump’s allocation demands – There are tensions between the administration’s demand for factory expansion to create more jobs and Lockheed’s traditional dividend/buyback profile. The key thing to watch here, if Trump does not allow Lockheed to buy back shares or pay dividends, is how well Lockheed invests that capital. New factories certainly create a tailwind of future growth. However, Lockheed is generally viewed as an income/buyback machine. So, it could lose some of its shareholder base if it is forced to reinvest that capital.

- The company’s backlog – Lockheed’s backlog is critical, as it can not only make future revenues more predictable and stable, but also give a glimpse into the overall demand for the business. The company’s backlog has often been one of the main focal points for many investors (and is listed in the KPI section).

- Geopolitical tension – Unfortunately, there are a lot of global tensions at this point. Lockheed Martin’s revenue growth often correlates with global geopolitical instability. Conflicts, military buildups, and rising tensions increase demand for defence systems. Case in point, the company surged more than 17% on Venezuelan news and Trump’s spending budget announcement at the start of 2026.

Lockheed has two main KPIs we need to track. For one, it’s backlog. Lockheed Martin’s backlog represents the total value of contracted orders that the company has yet to fulfill. The higher this is, the higher the chance the company will have consistent revenue in the future. With the Republican Party encouraging increased defence spending in 2026 and beyond, I believe this backlog will continue to grow. The second is simply the revenue and growth the company generates from each segment of the business. Right now, its rotary systems segment is the fastest growing. However, Aeronautics represents the highest portion of revenue by a wide margin.

November 3, 2025 – Lockheed Martin turned in a strong Q3. This is definitely a relief, as the company has had some rough quarters over the last year. Sales were up 9% YoY to $18.6B, earnings came in at $6.95, and free cash flow surged to $3.3B.

Perhaps more importantly, backlog hit an all-time high of $179B, underscoring the demand tailwinds across pretty much every one of its segments. The main thesis for a company like Lockheed here at Premium is the acceleration in military defense spending globally as geopolitical tensions continue to rise. And we are starting to see signs of that in Lockheed’s backlog.

Management raised full-year guidance for revenue, operating profit, and earnings while keeping free cash flow guidance the same at $6.6B. The dividend was bumped 5% and authorization for buybacks have been increased by $2B. Historically, Lockheed has been one of the most shareholder friendly companies in the United States, buying back shares at an extensive pace and paying out rock-solid dividends.

Aeronautics Revenue jumped 12% to $7.3B, largely driven by F-35 production. That said, there was some one-time events making growth larger than it seems. If we isolate this out, growth sat around 1%. This area of the business is definitely struggling a bit, and is one of the larger segments of the business. However, I do believe this will turn around.

Lockheed continues to lean into the F-35. 46 aircraft were delivered this quarter, and the company now expects 175–190 deliveries this year. Backlog stands at 265 aircraft, and Lockheed is working on adding new tech into the planes that will ultimately boost margins from sales.

Missiles and Fire Control (MFC) was the standout on the quarter in my opinion. Revenue climbed 14% and profits increased 12%.

Importantly, Lockheed landed a $9.8B PAC-3 deal and a $9.5B JASSM/LRASM contract. These are massive multi-year awards that should offer stability over the next decade. The growth story here in the MFC segment is real and has legs.

Rotary and Mission Systems (RMS) revenue was effectively flat and profits grew about 5%. The CH-53K heavy-lift contract ($10.9B over 5 years) is a big win but it is still very early. RMS is no doubt lagging the rest of the company. Investors need to pay particular attention to this segment, as it needs to accelerate in 2026 to contribute meaningfully to results.

Space Space revenues rose 9% to $3.3B and the backlog here is now $38B. It is nice to see this segment picking up the pace over the last while here, as it has historically been the slowing growing out of the bunch. Governments pushing more money into space-based missile defense and satellites should benefit Lockheed well, as it is one of the larger companies able to satisfy demand.

Lockheed’s deepening presence in space-based missile defense and next-gen satellite tech (like NG GEO and SDA Tranche 1) supports long-term strategic relevance. The company is also investing corporate-level R&D into a potential space-based interceptor demo by 2028.

Lockheed generated $3.3B this quarter alone, bringing YTD free cash to $4.1B. This kind of shows you how “lumpy” free cash flow can be overall, and why it’s important to span it out over an entire year. The full-year target remains $6.6B, and anything above that will be used to fund pension obligations for next year.

This company generates a boatload of free cash flow, so I would expect both dividend growth and share buybacks to continue.

Overall, Lockheed looks well-positioned to deliver mid single digit top-line and free cash flow growth. In my opinion, especially at these valuations, investors should view this as a high-quality compounder, not just a slow-growing dividend payer.

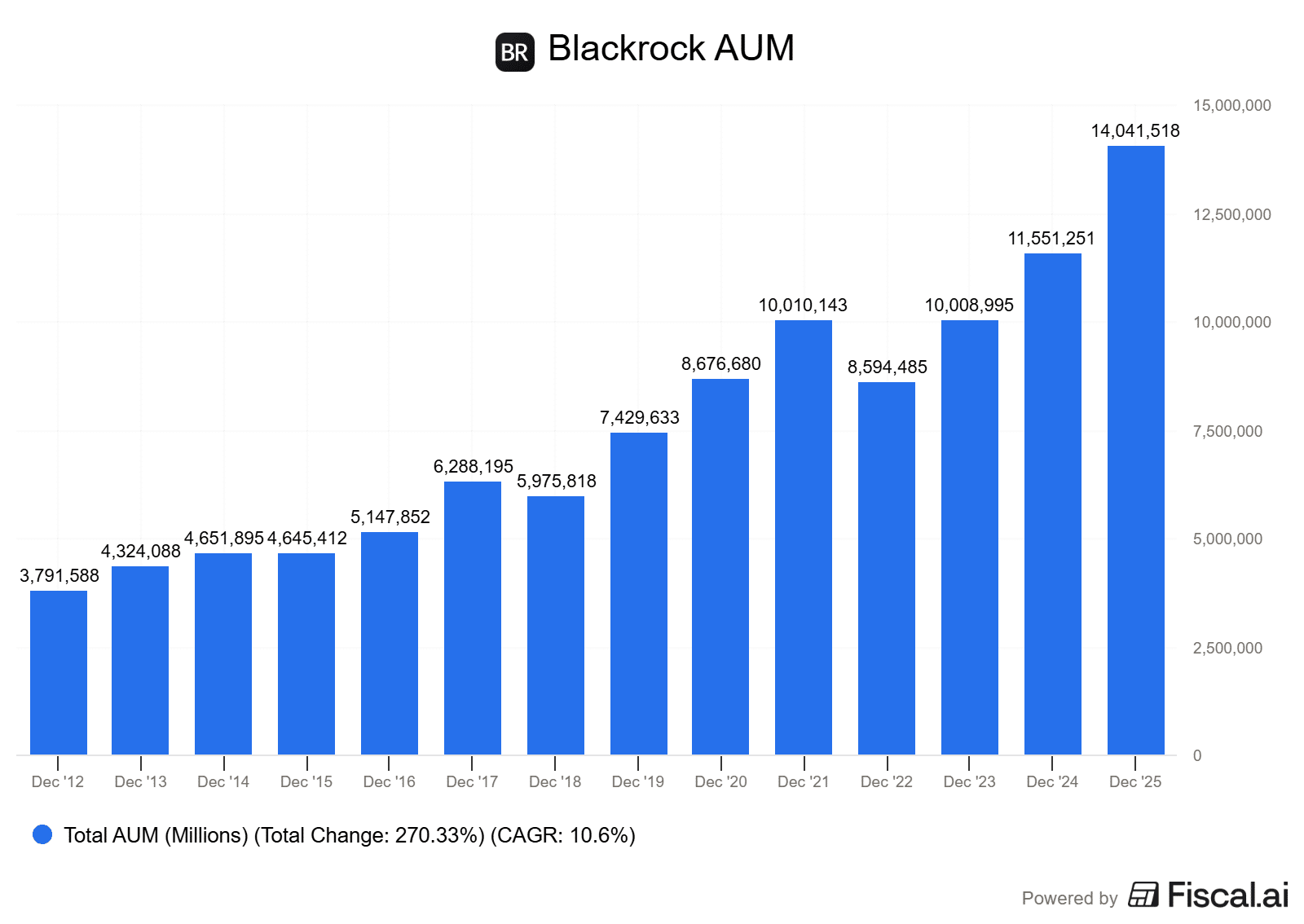

BlackRock Inc (BLK)

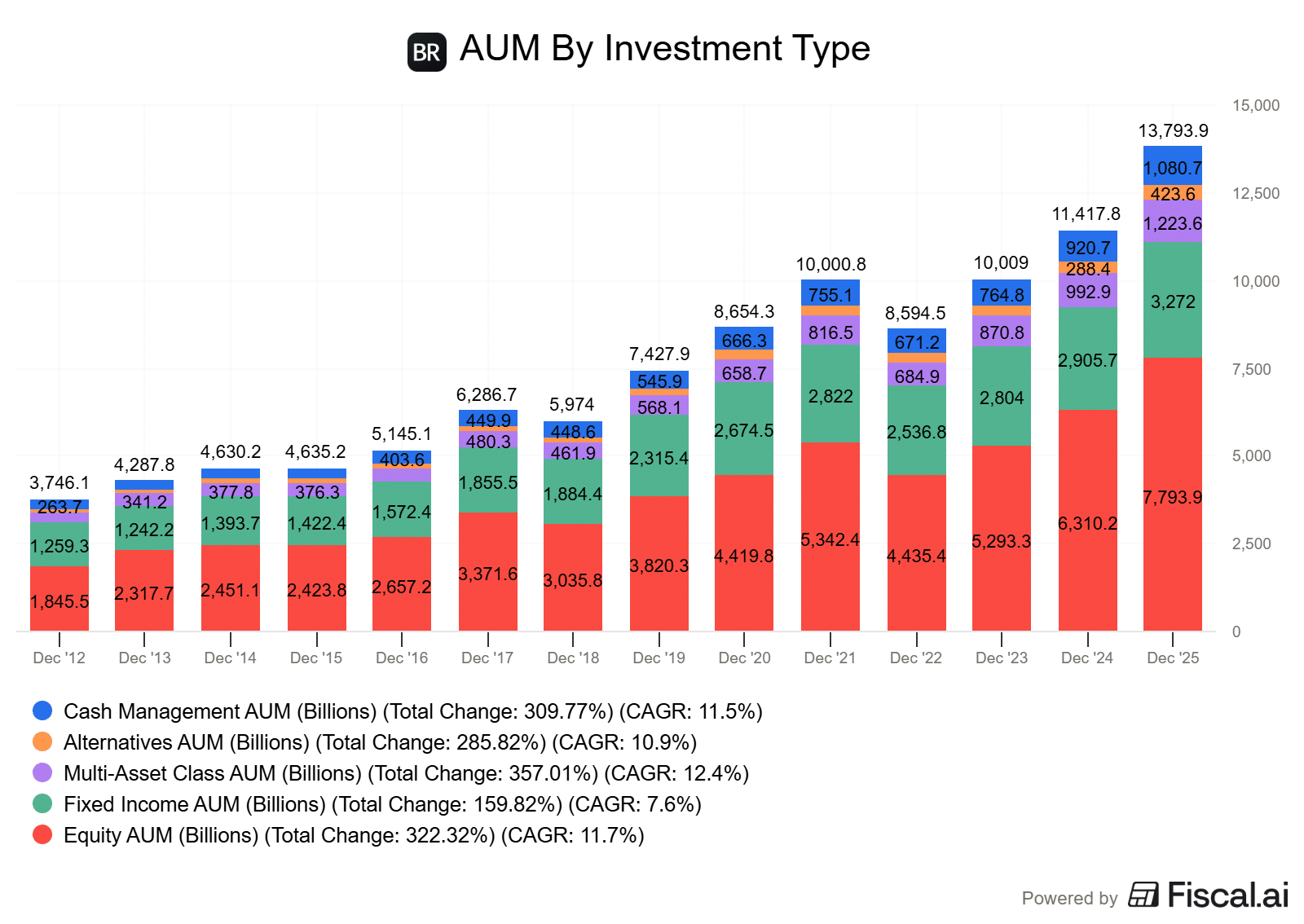

BlackRock is the largest asset manager in the world, with $11.475 trillion in assets under management at the end of September 2024. Its product mix is fairly diverse, with 55% of managed assets in equity strategies, 26% in fixed income, 9% in multi-asset classes, 7% in money market funds, and 3% in alternatives. Passive strategies account for around two thirds of long-term AUM, with the company’s ETF platform maintaining a leading market share domestically and on a global basis. Product distribution is weighted more toward institutional clients, which by some calculations account for around 80% of AUM. BlackRock is geographically diverse, with clients in more than 100 countries and more than one third of managed assets coming from investors domiciled outside the US and Canada.

Blackrock has reached a remarkable $14 trillion in assets under management. And although I mention this AUM every single year in my thesis, in my opinion, the story is no longer just about Blackrock’s scale. In fact, lots have said its scale would be its downfall. After all, there is only so much capital out there to collect fees on.

However, by leveraging its dominant iShares ETF ecosystem to fund its aggressive expansion into high-margin private markets, BlackRock is building an engine that is uniquely positioned to benefit not only from the massive popularity of the equity markets, but also from extensive infrastructure and artificial intelligence rollouts. I’ll explain more in the acquisition segment of this thesis.

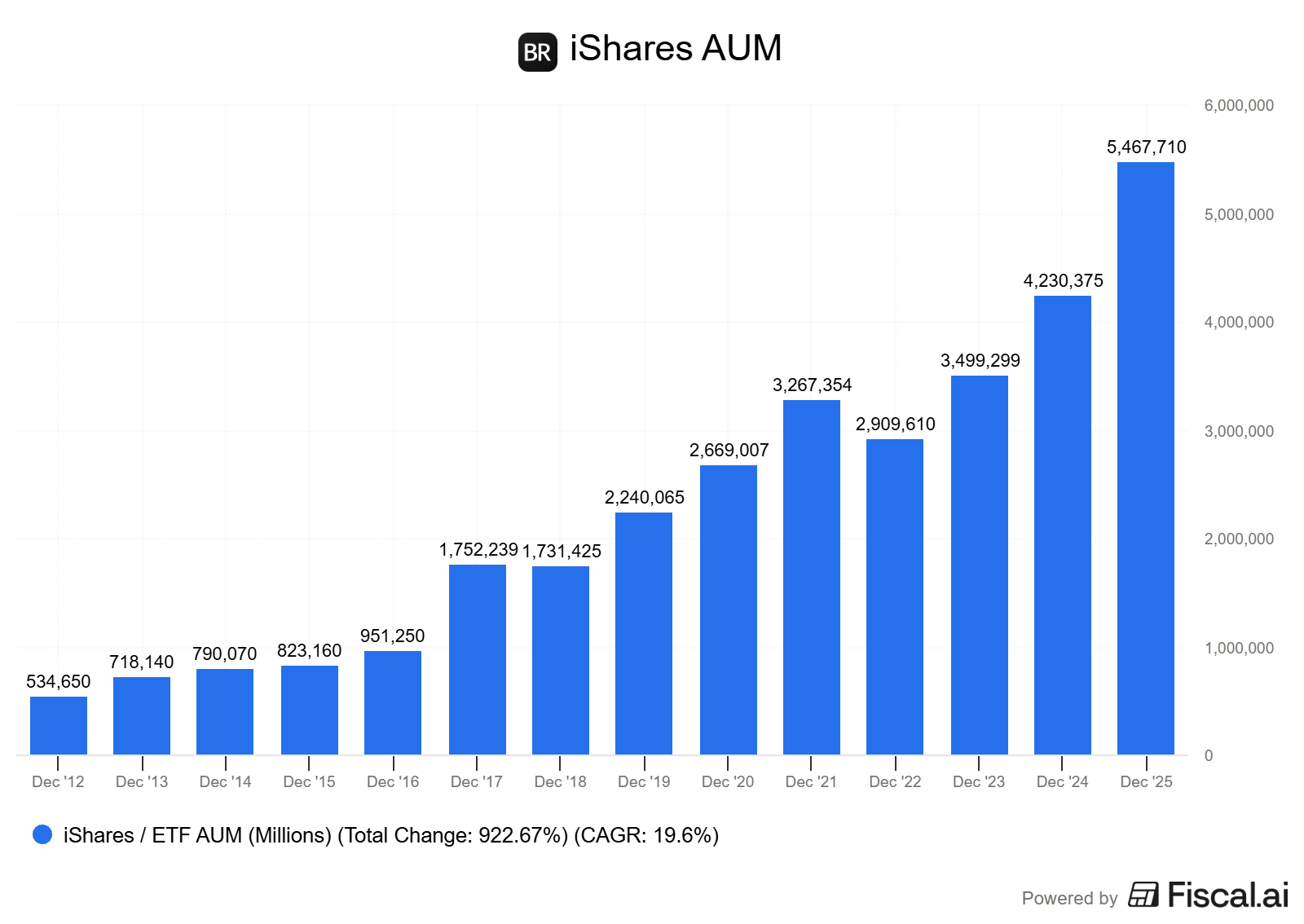

A pillar of my thesis remains the iShares suite of ETFs, which continues to be the gold standard in the industry. As of 2026, iShares holds a commanding market share, serving as the primary gateway for both retail and institutional capital entering the markets. More and more investors are turning to either ETF portfolios or core/satellite portfolios (core of ETFs, satellite holdings of individual stocks). For most investors, the first thing they ever see when it comes to ETFs is iShares. This is intentional, and is the result of years and years of successful marketing and positioning.

ETFs provide a massive, recurring base of low-cost, high-volume revenue that acts as a cash machine for the firm. Passive index funds, even with fees of 0.05% or less, are highly profitable because the fund is simply tracking a basket of stocks.

More importantly, BlackRock is now using the iShares brand to “democratize” private investments. By launching products that wrap private credit and infrastructure assets into ETF-like structures, the company is tapping into the multi-trillion-dollar retail and 401(k) markets, allowing average investors to access the types of alternative yields that were previously reserved for the ultra-wealthy.

Whether or not you agree with private credit/equity, there is no doubt that it is exploding in popularity, and Blackrock knows this. That is exactly why they’re expanding into the space in a big way.

The most transformative element of the current thesis, however, is BlackRock’s aggressive growth through strategic acquisitions. The 2024 purchase of Global Infrastructure Partners (GIP) and the 2025 integration of HPS Investment Partners have completely redefined the company’s Alternatives segment.

BlackRock has proven to be a master of the buy-and-build strategy. What I mean by this is they take specialized, high-performing firms and plug them into its global powerhouse. This has allowed the company to pivot rapidly toward the mega forces that are driving the market. That being, the financing of data centers required for AI, and the global energy transition. Blackrock can give investors exposure to this, while earning significantly higher management and performance fees than it does on its passive indexing products.

Finally, BlackRock’s dominance is reinforced by its technology moat, Aladdin, which has now integrated the data from its Preqin acquisition. The name stands for Asset, Liability, Debt, and Derivative Investment Network. I like to think of it as a gigantic simulation machine. It takes thousands of real-world variables, like a war in the Middle East, a sudden change in oil prices, or a massive storm, and runs millions of simulations to show an investor exactly how their money might be affected. Because so many different banks and insurance companies use it, Aladdin has become the common language of the financial world.

This allows BlackRock to offer a “whole portfolio” view that no other firm can match. This tech, combined with a record of successful acquisitions, has created a firm that is arguably more defensive than a traditional bank yet has the growth profile of a fintech leader. As BlackRock continues to use its massive balance sheet to acquire its way into new sectors, many will still believe the company is too large to grow at scale. However, savvy investors will know this company has plenty of room to grow.

This company is a bit more “cyclical” than any other on this list, not necessarily to the economy, but to the markets. So, expect some volatility. But in my opinion, this company is best-in-class.

- Acquisitions. 2026 will be the first full year that BlackRock will operate with the complete integration of Global Infrastructure Partners (GIP) and HPS Investment Partners. Investors should watch how BlackRock uses its massive global distribution network to scale up these businesses. If it does it well, investors should be hoping for more acquisitions, because there are plenty of them out there.

- AI and Energy Buildout. BlackRock is positioned to finance the world’s most capital-intensive projects. Through its new infrastructure funds, the company is targeting electricity and data center needs. In 2026, the trend to watch is the deployment of the $100 billion AI infrastructure fund launched with Microsoft. If there is large-scale success, the company will no question seek out more deals.

- Tokenization. Following the success of its BUIDL fund, which tokenized U.S. Treasuries, the firm is expected to expand this technology to private equity and real estate in 2026. The theory here is using blockchain to buy a piece of a private wind farm as easily and instant as buying a share of Apple. This trend reduces administrative costs and settlement times, further entrenching BlackRock’s technology as the essential bridge between “old finance” and the digital future.

- Private markets. As traditional banks face tighter regulations and higher capital requirements in 2026, BlackRock’s private credit arm has stepped in as the primary lender to mid-market companies and infrastructure developers. This trend is particularly valuable for my thesis because it provides a natural hedge. If interest rates stay higher for longer, BlackRock’s income from these private loans actually increases.

Blackrock is an asset manager. Because of this, the KPIs we want to follow are primarily related to assets under management. The larger it can grow in terms of AUM, the more fees it can charge to manage those assets and, thus, generate more profit. In addition to this, however, I have attached a KPI of the company’s iShares AUM as well, to give you an idea of how fast that is growing.

January 20, 2025 – BlackRock just put up a quarter that should silence anyone worried about the scale of this $14T asset manager. In fact, management mentioned that 2025 will go down as one of the best years on record for the company.

For years, the bears have argued that BlackRock was getting too big to grow, but the results show that the best asset manager in the United States is just getting better. Total revenue jumped 23% in the quarter and net inflows hit a whopping $342 billion, pushing the full-year total to nearly $700 billion.

This wasn’t just an interest in market activity pushing assets higher. Organic base fee growth accelerated every single quarter of the year, finishing at a 12% clip in the fourth quarter. It is clear that Larry Fink is successfully pivoting the company toward higher-fee territory. This was a much needed transition. If he hadn’t of laid out the groundwork for this half a decade ago, I would have agreed that the company was simply too large to grow as fast as it used to.

By folding GIP, HPS, and Preqin into the mix, which are key acquisitions in infrastructure, private markets, and the data for those private markets, BlackRock is no longer just the king of low-cost indexing. They are now a dominant force in these markets, areas that carry significantly higher margins than your standard S&P 500 fund.

They are going to where the puck is going, not to where it has been. This is clear by the Preqin acquisition. Why? Because this is a company that provides data on the private markets. Right now, private market data is scarce. However, as demand for these alternative assets increases, so to will the demand for the data to make them transparent. They’re thinking 2-3 steps ahead here, which I love.

The real story here is the shift in the fee-related earnings. While the margins might look messy on the surface due to all of the acquisitions and performance fee timing, the underlying business is becoming more profitable. Excluding the performance fee volatility, margins actually expanded to 45.5%. It is not surprising that margins are rising, considering the fact the recent acquisitions it has made bring a much higher margin profile to the business.

They are becoming the essential data and risk layer for the entire private markets industry. If the Department of Labor opens the gates for private assets in 401k plans, BlackRock pretty much owns the only gate into that area. They are already talking about a generational opportunity in fixed income as the yield curve steepens, and with $3 trillion already managed in that segment, they are perfectly positioned to capture the rotation out of cash.

The company hiked the dividend by 10% and plan to buy back another $1.8B in shares next year. If you were looking for signs of a slowdown, you didn’t find them here. BlackRock is entering 2026 with a base fee run rate that is 35% higher than where they started 2024. This seems absurd to say, because the markets increased by over 25% in 2024. However, they continued to run in 2025.

Visa (V)

Visa is the largest payment processor in the world. It also facilitates global commerce through the transfer of value and information among a global network of consumers, merchants, financial institutions, businesses, strategic partners, and government entities. It offers debit cards, credit cards, prepaid products, commercial payment solutions, and global automated teller machines. The company was founded by Dee Hock in 1958 and is headquartered in San Francisco, CA.

Last year, I called Visa one of the largest economic moats in the world, and as we look toward 2026, that moat isn’t just holding, it’s expanding. I’ve mentioned quite a few times that a company’s economic moat is well known, and the market reflects this in its price. Where the true value of the moat comes into play is management’s ability to flex it. I believe Visa is doing just that.

Visa has evolved from a simple credit card company into the primary settlement layer for the global economy. While the S&P 500 has been obsessed with AI, Visa has been quietly processing over $15T in transactions, growing its network to connect 175 million merchants across 200 countries. The fear that fintech or buy now, pay later would disrupt Visa has proven to be way overblown. Instead, Visa has simply absorbed these trends, providing the underlying payment rails that almost every fintech app actually runs on.

What makes this business truly special is how capital-light it is. To process those trillions of dollars in transactions, Visa only needs to spend about $1.5B on capital expenditures annually. When you realize they are generating $40B in revenue, you see the power of the model. They aren’t building factories or laying thousands of miles of cable every year. This massive operating leverage results in substantial free cash flow, which topped $21B in 2025. This cash machine allows them to relentlessly buy back shares and hike dividends regardless of the macro environment.

The most exciting part of the thesis for 2026 is the mainstreaming of stablecoins and digital assets. For years, people thought crypto would be a “Visa killer,” but the reality is the opposite. With the passage of the GENIUS Act in late 2025, we finally have the regulatory clarity needed for institutional stablecoin adoption.

Visa has jumped on this, launching its Stablecoin Settlement platform in the U.S. that allows banks to settle obligations in USDC over the Solana blockchain. This is a massive deal because it enables 24/7 instant settlement, moving away from the old five-day banking window. Visa is essentially turning the threat of crypto into a tool to make its own network faster, cheaper, and more dominant.

Beyond the tech, the core business is seeing a huge surge in credit card spending. Even with the administration’s talk of interest rate caps, Visa remains resilient because its model is based on transaction volume, not just the interest that the banks charge. We’re seeing a structural shift in developed markets where “agentic commerce”, AI bots shopping on behalf of humans, is becoming a reality.

Visa is already rolling out the “Trusted Agent Protocol” to authenticate these digital shoppers, ensuring that every time an AI buys something for you, Visa still gets its cut. Combine this with the massive $80T opportunity in cross-border B2B payments through Visa Direct, and you have a company that is still finding ways to grow double-digits despite its size.

Financially, the story is as clear as ever. We’re looking at 60%+ operating margins and a company that has reduced its share count by nearly 20% over the last decade. They just authorized another $30 billion for buybacks, proving they are still a machine for returning capital to shareholders.

Whether it’s a tourist tapping their phone in an emerging market or a multi-national corporation settling a million-dollar invoice via stablecoins, the odds are high that Visa is the one making it happen. It remains the ultimate foundational GARP play for anyone who wants exposure to global growth without the volatility of the latest tech fad.

- Credit card rate cap. Trump loves to hear himself talk, and his target at the start of 2026 was credit card interest rates. He wants them capped at 10%. Visa only makes money from the transactions, so the rate of interest doesn’t matter to them. However, in theory, rates capped at 10% would force banks to cancel/not lend to a large number of consumers, which ultimately could present volume headwinds. I would put the likelihood of something like this passing as regulation at next to 0%, but even the fears of it will cause pricing pressure.

- Cross-border volumes. These are the highest-margin segments of Visa’s business. They happen when someone swipes a card internationally. Imagine swiping your Canadian credit card for a USD purchase in the United States. Continued international growth will be key for the company moving forward, allowing for more adoption of its cards globally and higher fees from international transactions.

- Stablecoin settlement expansion: Follow the rollout of USDC settlement across Visa’s global banking partners. The trend to watch is how many traditional banks migrate their backend treasury operations to Visa’s blockchain rails to achieve 24/7 liquidity.

- Volume growth and take rate. Ultimately, these are the two main drivers of the business. Get transactions to be higher dollar values, and have higher take rates on each transaction, ultimately improving revenue and free cash flow.

At its core, Visa is a simple business. What you want to look for is 3 main KPIs. First, the total number of transactions processed. This is fairly self-explanatory. The more transactions processed through Visa, the more fees it can collect. The second would be total transaction volume. This is important because Visa’s “take rate” is in relation to its total transaction volume, which is ultimately the total dollar volume processed through its cards. The final KPI, cross-border volume growth, is the amount of volume that is processed from cards that are not in their home country. For example, if a Canadian travels to the US and uses their Canadian Visa. Visa charges fees for this, and it is a profitable side of the business.

Oct 29, 2025 – Visa’s first quarter of 2026 was a beat on both the top and bottom lines. Revenue came in at $10.9 billion, a 15% increase year-over-year, while EPS hit $3.17, slightly above estimates. The company saw an 8% increase in total payments volume and a 12% jump in cross-border volume, showing that despite a relatively rough economy, consumers were still spending over the holidays. While the high-end consumer segment grew the fastest, management noted there was no real deterioration in lower-spend bands.

The standout growth driver this quarter was Value-Added Services (VAS), which grew 28% and now accounts for half of the company’s total revenue growth. This move into high-margin services like advisory and risk solutions is helping offset a lower contribution from currency volatility. New Flows, including B2B and Visa Direct, also posted strong gains with revenue up 20%. On the expense side, you might notice a large uptick in expenses. However, these are largely one time costs related to marketing campaigns in the World Cup and Olympics. It’s not cause for concern.

Visa still returned $5.1 billion to shareholders through buybacks and dividends. This has always been an extremely shareholder friendly company, and I wouldn’t expect anything to change. The company reaffirmed its full-year guidance for low double-digit revenue growth.

Visa now has 17.5 billion tokens active, more than triple the 5 billion physical cards in circulation. This is significant because tokenized transactions see higher authorization rates and lower fraud. This is directly fueling its 28%~ growth in value-added services.

Management also spoke on agentic commerce, where AI agents complete purchases on behalf of users. With over 100 partners currently working with Visa, the company is positioning its token technology as the primary driver for AI-spending.

I find it harder to not talk about Trump during earnings season, and with Visa it’s simply unavoidable. President Trump has proposed a 10% cap on credit card interest rates to address the cost of living. It is important to remember that Visa and Mastercard are payment networks, not banks; they do not lend money or charge interest themselves, so they don’t lose interest income directly.

However, a cap could still hit them indirectly if it breaks the banking model. Banks use high interest rates to cover the risk of lending to people with lower credit scores; if they are forced to cap rates at 10%, many may decide it’s no longer profitable to lend to those millions of “risky” customers. If banks stop issuing cards or slash credit limits to avoid losses, the total number of transactions flowing through Visa’s network would drop. Essentially, the networks only make money when people spend, so if the banks pull back on credit, Visa loses the transaction volume that fuels its business.

The thing here is I do not think there is even a remote chance this goes through. It would be devastating to the banking sector, and Trump likely does not want to shake that boat.

Overall, it was steady as she goes for Visa, which is exactly what we want to see from a Foundational Stock.

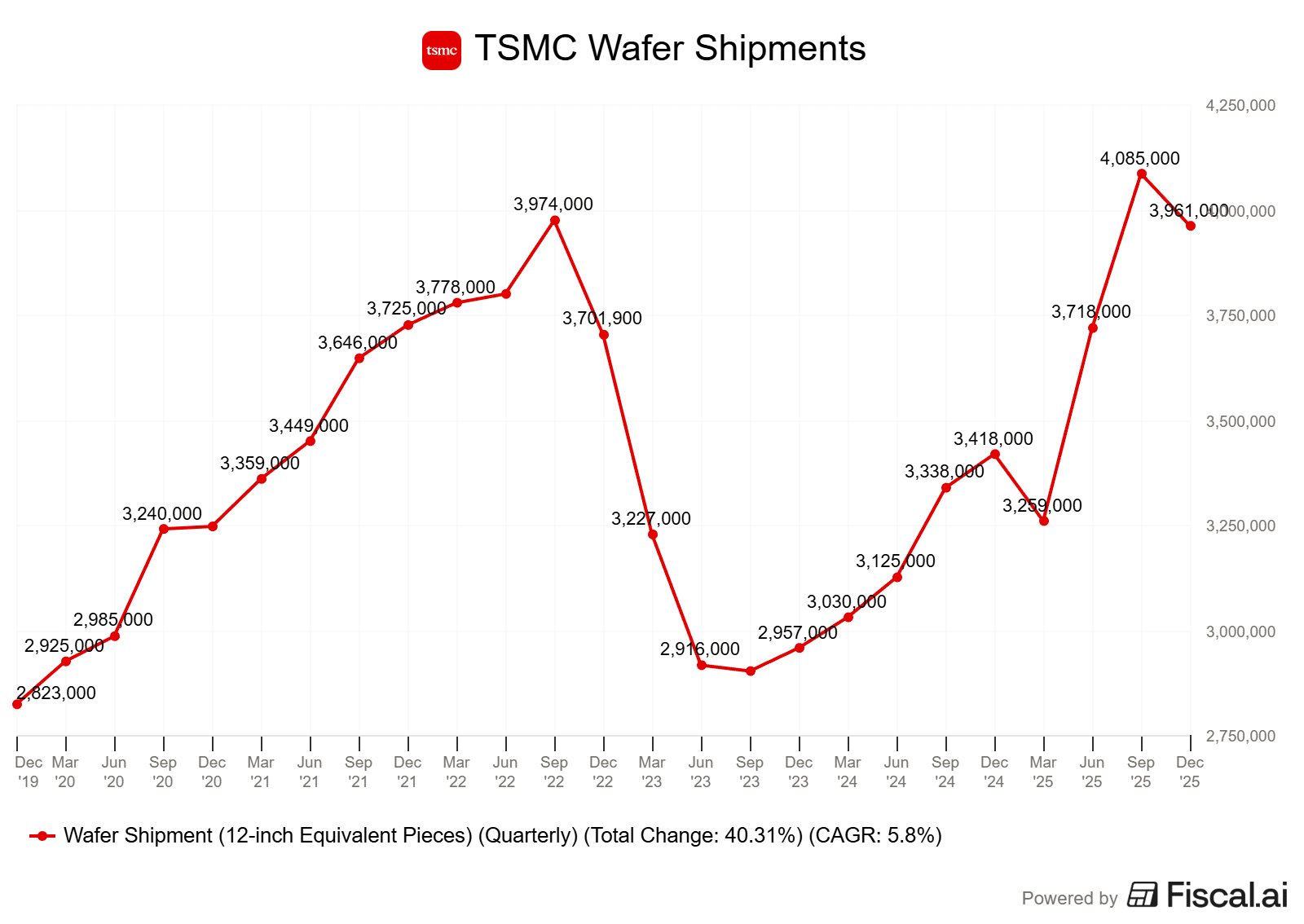

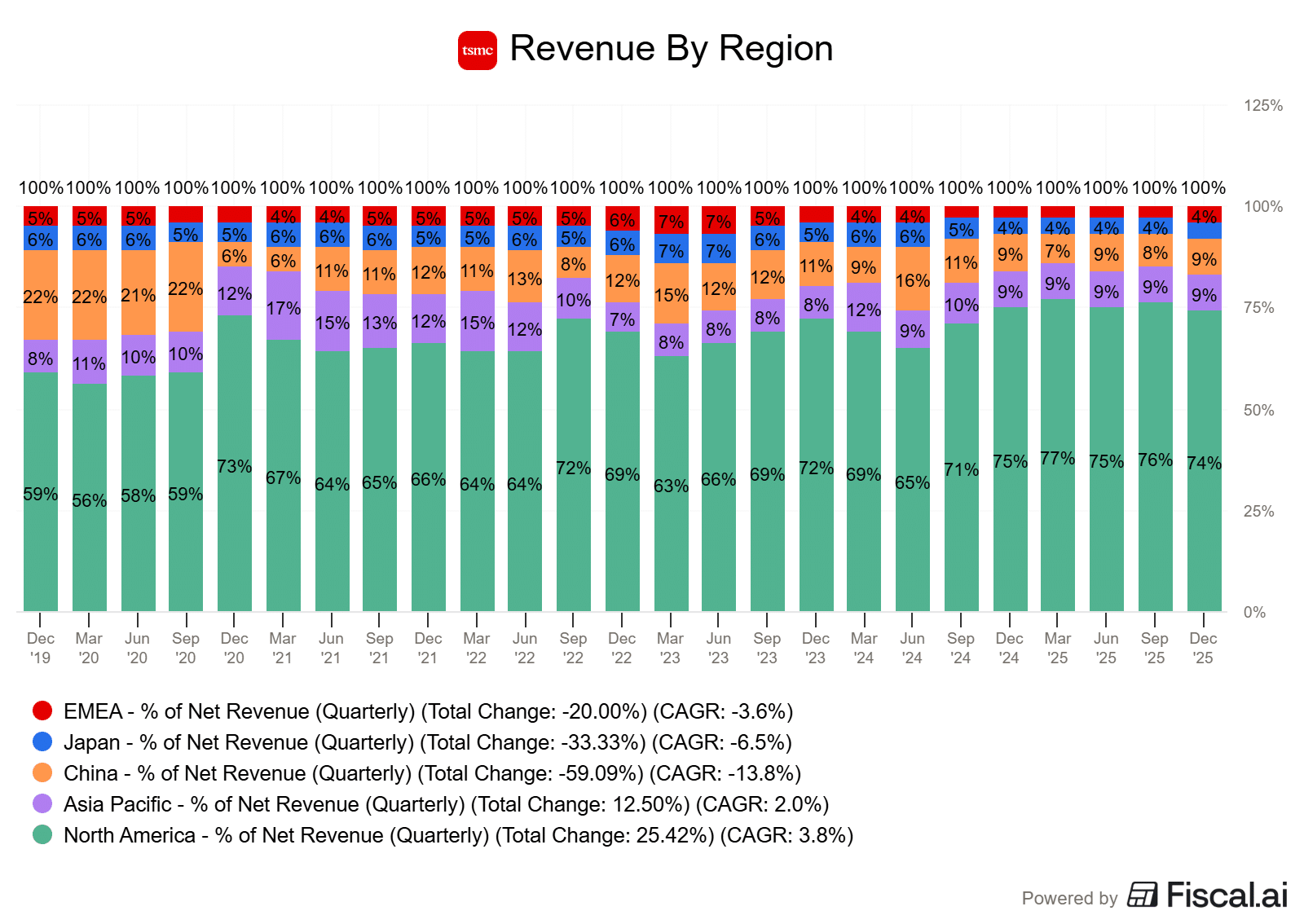

Taiwan Semiconductor (TSM)

Taiwan Semiconductor Manufacturing Co., Ltd. engages in the manufacture and sale of integrated circuits and wafer semiconductor devices. Its chips are used in personal computers and peripheral products, information applications, wired and wireless communications systems products, and automotive and industrial equipment, including consumer electronics such as digital video compact disc players, digital televisions, game consoles, and digital cameras. In more recent times, the company has been the backbone of the artificial intelligence buildout.

Taiwan Semiconductor Manufacturing Company (TSMC) is the indispensable backbone of the digital economy. At one point, Warren Buffett called this the most important company in the world. He owned it, but was forced to sell due to the heightened geopolitical situation. As a large conglomerate, Berkshire could not risk billions of dollars. However, as retail investors, we can be prudent with our allocations and grab one of the highest-quality companies on the planet at a discounted valuation. We just have to be willing to accept that relatively minimal risk.

That risk is a potential conflict in the Taiwan Strait, primarily involving China. The catastrophic nature of an event like that would suggest that the impact would extend far beyond TSMC, so it would not be the only equity affected.

TSMC serves as the primary manufacturing engine for virtually every major technology trend, from 5G and the Internet of Things to automotive electronics and, in recent times, the rapid adoption of artificial intelligence. As the world’s largest chipmaker, TSMC has secured a near-monopoly on high-end production. The company owns a whopping 71% market share. This dominance is underpinned by unmatched proficiency. This proficiency leads to higher margins, which leads to more money to hire more advanced staff and build better equipment, which leads to increased proficiency, etc. It is a snowball effect for the company.

The most notable part about this snowball is it allows the company to generate enough free cash flow to simply outspend its competitors. TSMC can pay for better staff, build better equipment, and stay miles ahead of any competitors. Despite being a $1.7T company, TSMC carries only $34B in debt, a number it could completely eliminate with less than a year of its free cash flow.

In January 2026, the company announced an expected 25% compound annual growth rate on revenue through to 2029. In addition to this, the company planned to spend around $56B in capital expenditures. To put this into perspective, TSMC’s planned spending over the next three quarters is projected to exceed the total capital expenditures of the last three years, combined.

What does this tell us? It tells us that TSMC has a supply problem, not a demand problem, and they’re attempting to build out as much supply as possible. If it can execute on this, 30%+ growth in top and bottom line sales is not out of the question.

While TSMC functions as the ultimate “picks and shovels” play, profiting from the production of chips regardless of whether the end-user software is profitable, the stock trades at a significant discount to peers like NVIDIA due to unavoidable geopolitical tensions as mentioned above.

Beyond geopolitics, investors must navigate the inherent boom-bust cycles of the semiconductor industry, where a slump in smartphones or PCs can cause lumpy earnings. However, this is being somewhat offset by an increased amount of activity in the space due to artificial intelligence. There is the potential for demand there to offset any decline in device-type demand during an economic drawdown.

TSMC retains high customer concentration, with Apple accounting for roughly 24% of revenue in 2024 and NVIDIA rapidly climbing the ranks. The company also faces execution risks as it attempts to replicate its efficiency in new, high-cost facilities in Arizona, Japan, and Europe. However, with competitors like Samsung and Intel still struggling to match TSMC’s yields, the company remains in a constant feedback loop: more success leads to more reinvestment, which leads to better yields and even more customers.

Ultimately, while the stock may face short-term volatility, the thesis rests on the fact that a world without TSMC is currently unimaginable, making its current valuation a rare “fair price” for the most important technology company on the planet.

- Volume Ramp. Investors should watch for yield stability and adoption rates of TSMCs new chips, as Apple and other major high-performance computing (HPC) clients have already booked a significant portion of its capacity. Success here will determine if TSMC can maintain its massive pricing premium over competitors like Samsung and Intel.

- Capital Expenditures. TSMC stunned the market with a 2026 capital expenditure budget of $52 billion to $56 billion. This is a 30% jump from last year, and is a direct bet on increased demand in regards to AI. The key watchpoint is whether this spending leads to a continued cycle of growth or creates an overcapacity risk if the hyperscalers cool down on orders.

- Margin Dilution. A lot of TSMC’s advantage was the fact it operated in Taiwan. Labor is cheaper, land is cheaper, and just in general, it is much cheaper to run a business. Now that it is expanding in places like the US and Europe, margins are going to inevitably come down. They just cannot operate at the same margins in North America as they can in Taiwan. The key thing to watch here will be whether they can offset the margin impacts with larger sales.

- The AI boom continuing. Although TSMC’s chips are in practically every piece of technology we use, let’s not kid ourselves. A large chunk of its revenue and earnings right now is coming from AI spend. Keep a close eye on how much the hyperscalers are spending, as this will directly impact TSMC.

I have attached a few KPIs for TSMC below. There are an abundance of them, but I feel I would overwhelm a lot of members digging deep into particular chips shipped. So instead, I will just show total shipments and revenue by region. These two will give you a good idea of how strong demand is. Outside of that, top and bottom line numbers are a good place to look.

January 20, 2025 – It was yet another outstanding quarter for TSMC. Revenue for the year jumped 36% to $122 billion and operating margins hit a staggering 50.5%. The shift to artificial intelligence is now blatantly obvious, as High Performance Computing (HPC) now makes up over half of the business. Pre-pandemic, this accounted for around 35% of revenue. It is now north of 55% and continuing to rise. Earnings continued to outpace revenue growth, growing by more than 45%, and with the company’s recent guidance (which I’ll get to in a bit), I expect this trend to continue.

If you were to draw a conclusions from this quarter in regards to TSMC that didn’t necessarily mention any actual numbers, it would be that the company has told you to stop worrying about whether or not we are in an AI bubble and instead worry about where the chips are going to come from to satisfy the demand.

While the pundits are arguing over whether AI demand is sustainable, Taiwan Semiconductor just signed off on a massive $56 billion capital expenditure plan for 2026. The amount the company is going to spend over the next 3 quarters will be more than the company has spent in the last 3 years combined. This isn’t speculative expansion, either. TSMC’s customers are saying build it, because we will use it.

The most telling part of the conference call was management’s admission that they are “nervous” about the massive investment step-up, but only because they feel the heavy burden of being the reason the world is bottlenecked when it comes to AI.

A lot of people believe it is power supply or data center supply that is the bottleneck. It’s not. It’s chips.

The company raised their long-term growth forecast to a 25% CAGR, primarily because of AI. A lot have been worried about the company’s expansion into Europe and Arizona. After all, it is a lot harder to operating a business with 50%+ operating margins in North America or Europe than it is Taiwan. However, the company is managing the 2-3% margin dilution with precision.

TSMC raised its profitability outlook, guiding for gross margin of 63% to 65% and an operating margin between 54% and 56%. This confirms what I had mentioned above, which is that earnings growth should continue to outpace revenue growth through margin expansion.

Overall, the message from this quarter is fairly clear. TSMC is the toll booth for the future of computing and artificial intelligence, and the line to get through is only getting longer.

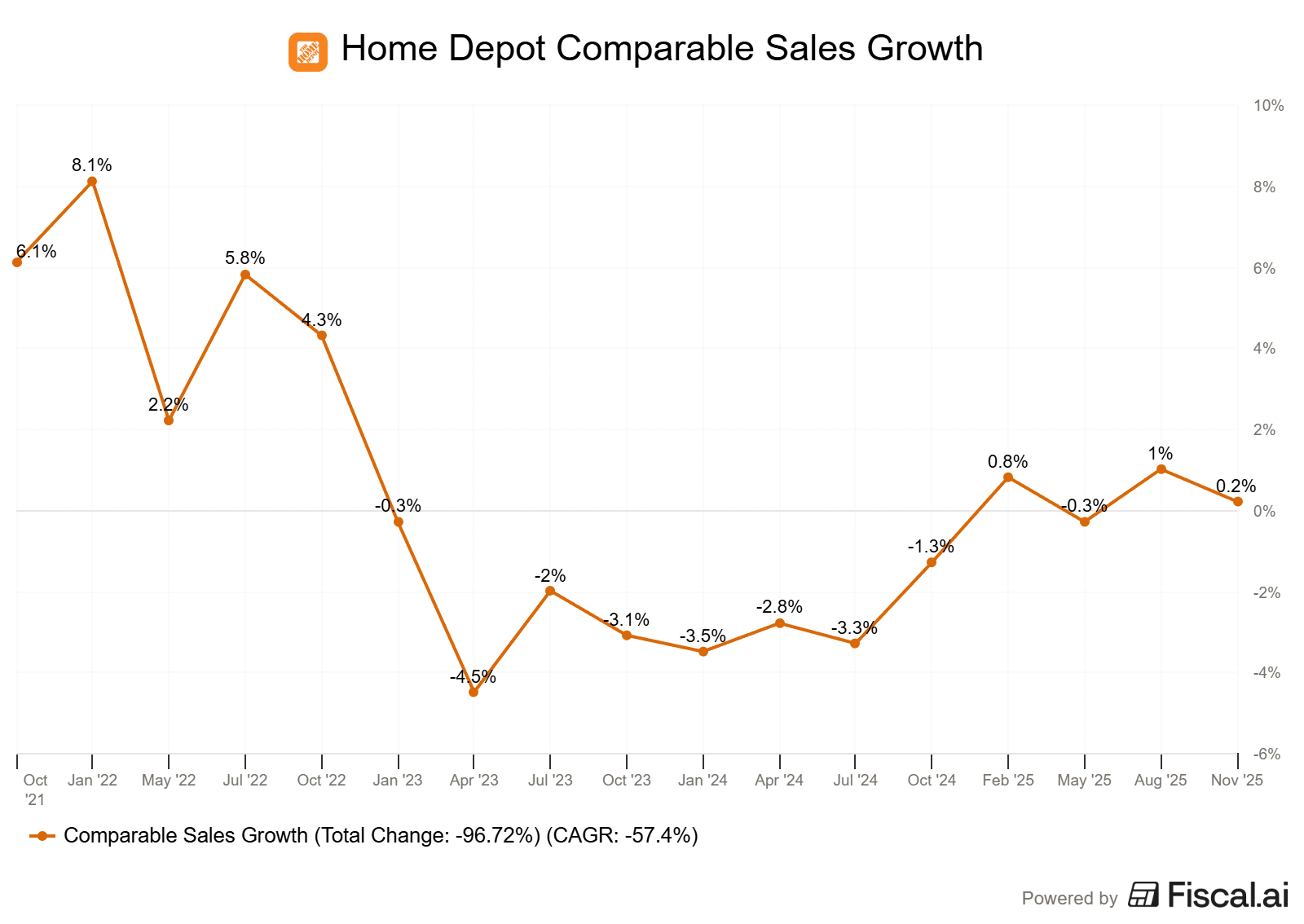

The Home Depot Inc (HD)

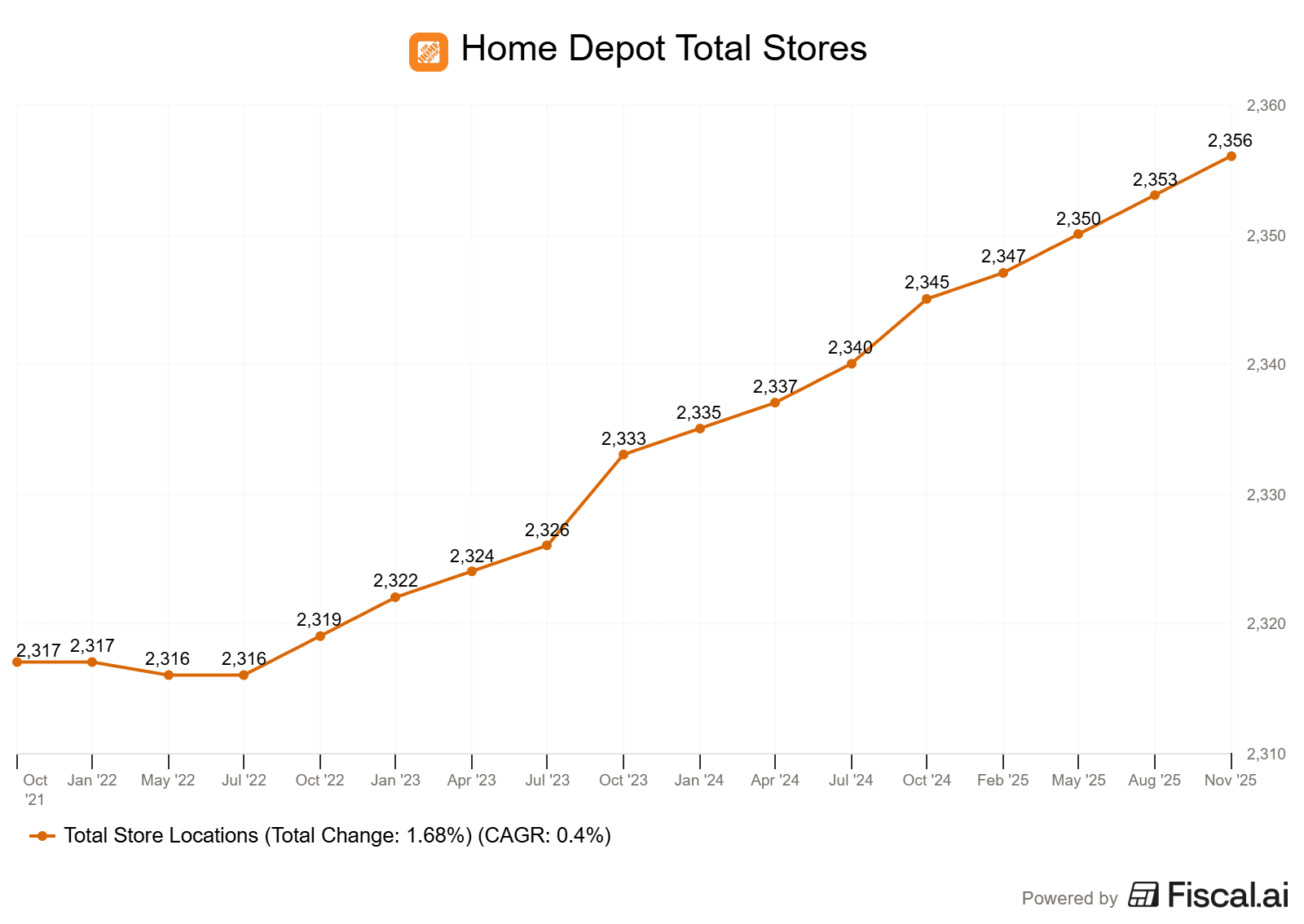

Home Depot is the world’s largest home improvement retailer, operating over 2,350 stores across North America and commanding a dominant lead in a massive $1.1 trillion total addressable market. The company serves two primary customer segments: the DIY homeowner and the professional contractor, the latter of which provides a critical “Pro” ecosystem that accounts for nearly half of its total sales. Home Depot’s massive scale allows it to maintain an incredibly capital-light model for its size, spending only about 2.5% of its sales on capital expenditures while generating over $159 billion in annual revenue. Ultimately, Home Depot acts as a high-quality compounder that leverages its physical footprint and advanced digital “interconnected” retail strategy to dominate the home improvement landscape.

As we move into 2026, the case for Home Depot is effectively a play on delayed gratification. For the past three years, the stock has tested the patience of even the most disciplined investors (myself included) as it navigated the “mortgage rate lock-in” effect, a phenomenon that essentially froze the housing market as homeowners clung to sub-3% rates from the pandemic. My main thesis here was that this lock-in effect would have plenty of people renovating their homes rather than selling to buy other homes. Remember, in the US, you lock your rate in for typically 30 years. a sub-3% mortgage rate for 30 years is an absolute dream scenario.

However, this just hasn’t worked out. High inflation, a weak economy, and general economic worries have resulted in a large-scale pullback of the consumer. This stagnation hasn’t weakened the company, however. It has actually allowed Home Depot to build what I call an eventual “coiled spring” of demand that is now estimated at over $50 billion in deferred home improvement spending.

Of course, Home Depot wouldn’t be exposed to all of this. But, with a 20%~ market share in this area, it certainly can grab a big chunk.

I have been incredibly patient on this one, accumulating for the better part of 3 years, waiting for the environment to turn around. My original thesis for Home Depot has not changed, perse, it has just been delayed a bit. I feel giving up on this company at this point in time, especially as rates are expected to continue to head down in the US, would be a mistake. Was I early? Certainly. But, I do not believe I am wrong. So, selling makes no sense for me.

What makes this different in 2026 is that we are finally seeing the transition from a retail-only giant to a dual-threat powerhouse. While the casual DIYer was sidelined by inflation and economic doubt, Home Depot spent nearly $24 billion to acquire SRS Distribution and GMS Inc. This wasn’t just about buying revenue, it was a strategic acquisition to capture the contractor side of home building and renovations. The roofing, drywall, and steel-framing contractors who handle the large-scale renovations that a trapped homeowner chooses over moving. By integrating over 1,200 distribution locations and 8,000 trucks, Home Depot has effectively widened its moat into the $1.1 trillion professional market, ensuring that when the recovery does begin, they own the entire supply chain from the retail shelf to the job site.

The company is a free cash flow machine, generating roughly $14B in free cash flow in 2025, which comfortably covers its growing dividend. Yes, it has paused share buybacks for now after a decade-long period of extensive buybacks, but this is primarily to pay for the acquisitions. I like this. Home Depot saw more value in outside building companies with depressed valuations than in buying its own stock back. Once it gets its debt in order, it will likely be able to resume buybacks.

We are looking at a business with a 30%+ return on invested capital that is essentially pre-positioning its inventory and logistics to handle a surge in high-ticket projects. Could this end up biting them if the turnaround doesn’t materialize for the next 3-5 years? Sure. However, the risk/reward here is relatively attractive, as I feel a lot of the current headwinds are priced into the company right now. For a business that has shown it can take investors’ money and reinvest it at exceptionally high rates of return, I’m willing to let this management team navigate this turnaround.

For those who can look past the short-term noise of mortgage rates and the economy, Home Depot remains the ultimate play on the “re-industrialization” of the American home. In my opinion, this is a foundational compounder that is simply waiting for the psychological unlock of a 6% mortgage rate and a slumping economy to release years of suppressed growth.

- “Pro” Revenue synergies. The key metric to watch is “pro-heavy” category growth (lumber, concrete, drywall). Success here means Home Depot is successfully taking market share from smaller, local distributors and becoming the one-stop shop for large-scale contractors. This should diversify them away from the more cyclical retail side of things, which is exactly why it rolled out billions of dollars for these businesses.

- The Mortgage “Unlock” Level. Keep a close eye on the 30-year fixed mortgage rate. Economists suggest that as rates drift toward the 5.75%–6% range, the “lock-in effect” begins to vanish. This is the primary catalyst that could trigger a 14%–15% surge in home sales, which historically leads to an immediate spike in Home Depot’s high-ticket project revenue.

- Artificial intelligence. Follow the rollout of the “Blueprint Takeoff” tool. By using AI to generate material lists and construction estimates instantly from blueprints, Home Depot is removing the friction that often delays large projects. A trend toward higher digital-first Pro sales will highlight whether or not this is working.

- Guidance. Watch for management to move from their baseline guidance (flat to 2% comp growth) to their “Market Recovery Case” (5%–6% total sales growth). This might not happen in 2026, but I do believe it will happen at some point in the next couple of years.

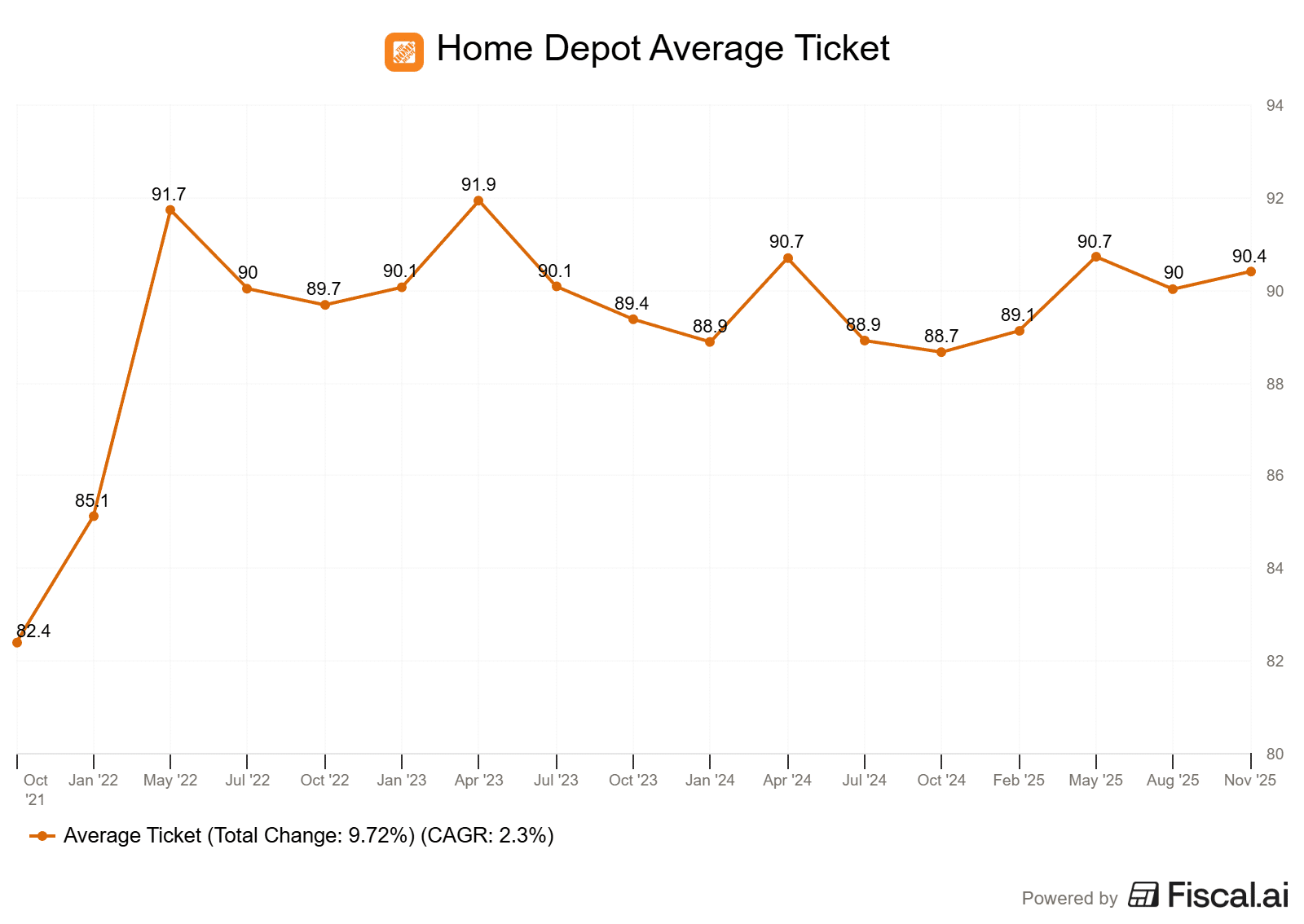

Home Depot is going to have 3 major KPIs that are much the same as any other retailer. The first would be same-store sales growth. This is going to be the growth that Home Depot achieves without factoring in new stores. This is an important KPI, as growing primarily from new stores is capital-intensive. We want to see growth from previous stores as well.

The second would be average ticket price. This is the average amount of money a customer spends at the store. A declining average ticket price can indicate consumers are pinching pennies and only buying necessities. And finally, we have total transactions. This one is fairly self-explanatory.

November 18, 2025 – Home Depot’s latest results, to me, show a company that is essentially bouncing along the bottom of this housing cycle. While total sales for the year grew 3.2%, that growth is almost entirely through acquisitions like SRS and GMS. If you strip away the M&A and the added sales from last year’s extra week, we’re looking at a business that is effectively flatlining. However, I’ve mentioned this quite a few times, this is expected. The environment is not all that good right now, and as patient investors, we are accumulating Home Depot waiting for a bit of a macro spark.

Comparable sales for the year were up just 0.3%, and while Q4 did manage to hit 0.4%, it’s clear the organic growth engine is still struggling to keep its head above water.

The biggest takeaway for me is management’s admission that they haven’t seen an inflection point in housing activity. I mentioend this in the thesis. This is a “delay” and not necessarily a thesis breaking situation.

We’re dealing with 40-year lows in turnover, and because people aren’t moving, the “repair and remodel” tailwind has turned into a headwind. Management pointed out that there is a $22B in pent up demand in home improvement right now because homeowners are just doing the bare essentials. They’re fixing the leaky pipe but they aren’t gutting the kitchen. There’s a few reasons for this. For one, interest rates are still too high south of the border. People will tap into home equity, but not when it’s this expensive. Secondly, it’s just a situation of a cost of living crunch. We need the middle/lower class to have a bit more financial flexibility so they open their wallets. I do believe this will happen eventually.

All of this showed up in the margins. Adjusted earnings for the year fell 3.6%, and return on invested capital, a metric I watch closely, dropped from over 31% to 25.7%.

What’s interesting is how aggressively Home Depot is doubling down on the “Complex Pro” to fight this. They’ve spent billions to buy their way into specialty companies like roofing and drywall, betting that being a one-stop-shop for contractors will protect them until DIY homeowners pick up the slick. It’s a smart long-term move, but it’s expensive over the short-term. They’ve even introduced AI tools for contractors to build project lists automatically. Considering I built my entire basement out with the assistance of Chat GPT over a year ago, I can’t imagine how good the technology is now.

For 2026, it’s more of the same “wait and see” story. They’re calling for comparable sales to be between 2% and flat, and expect Q1 earnings to be down mid-single digits. This isn’t necessarily due to sales weakness, but more so the integration of the major acquisitions they’ve made.

They’ve hiked the dividend again to $2.33 a quarter, which is great, but they’ve put share buybacks on pause until 2026. To me, the thesis remains the same as it was last quarter: the turnaround is taking longer than anyone wanted, and we are still at the mercy of mortgage rates and housing turnover.

Home Depot is doing the right things to gain market share in a bad environment, but until the macro picture clears up, the stock is going to remain in a holding pattern. If you’re a shareholder here, you simply have to stay patient and let the cycle play out.

Berkshire Hathaway Inc (BRK.B)

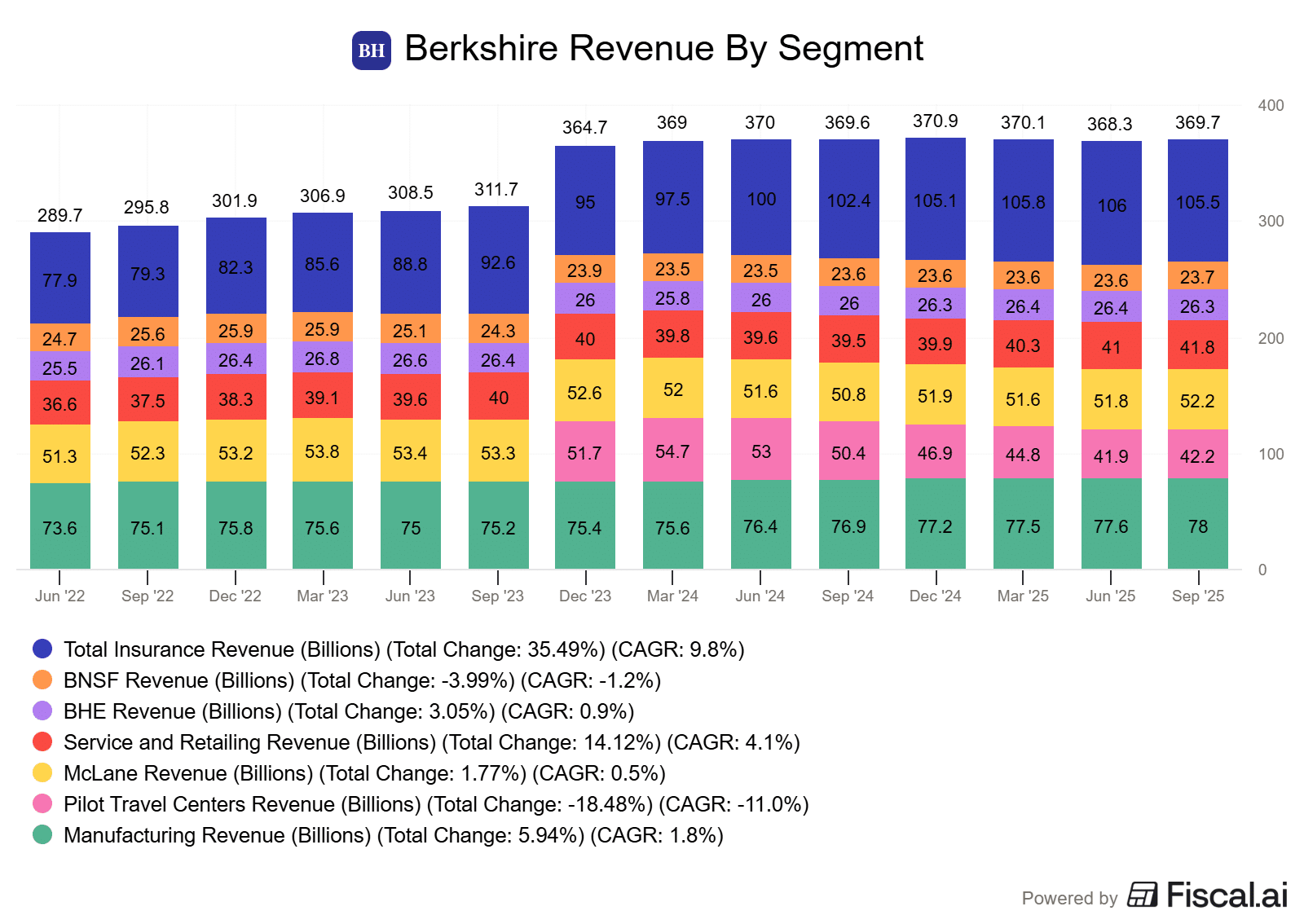

Berkshire Hathaway is a holding company with a wide array of subsidiaries engaged in diverse activities. The firm’s core business segment is insurance, run primarily through Geico, Berkshire Hathaway Reinsurance Group, and Berkshire Hathaway Primary Group. Berkshire has used the excess cash thrown off from these and its other operations over the years to acquire Burlington Northern Santa Fe (railroad), Berkshire Hathaway Energy (utilities and energy distributors), and the companies that make up its manufacturing, service, and retailing operations (which include five of Berkshire’s largest noninsurance pretax earnings generators: Precision Castparts, Lubrizol, Clayton Homes, Marmon, and IMC/ISCAR). The conglomerate is unique in that it is run on a completely decentralized basis.

The official hand-off at Berkshire on January 1, 2026, is easily the biggest milestone in modern finance. After all, this is the man who made it possible for a $1000 investment in 1965 to be $55M today. The market initially applied a slight “succession discount” to the share price. However, I think this was overblown. The underlying cash-generating machines like GEICO and BNSF provide a significant margin of safety, which is precisely why Berkshire remains on the Foundational List in 2026.

Greg Abel is definitely more hands-on and data-driven than Charlie and Warren. Warren’s “official” last investment was in Alphabet. However, this one had Abel written all over it. As good of an investor as Buffett was, technology was not his thing. After all, he needed to be convinced to buy Apple, the greatest investment Berkshire has ever made.

The secret sauce for this company is still the insurance side of the business, providing hundreds of billions of dollars in “float” that Berkshire can invest in public and private businesses. Most companies need to tap into the debt or equity markets for capital to make acquisitions. Berkshire’s float is basically permanent, zero-cost capital that Berkshire is paid to hold, and it gives them a massive advantage over many competitors because they can take on risks that would sink their peers. When you’re talking tens or even hundreds of billions of dollars, being able to utilize that money without it being debt is a gigantic plus.

Because of the float, the company’s leverage ratio (debt to EBITDA) typically hovers in the 1.5-1.6x range. Just to give you an idea, a debt-heavy telecom often runs north of 3.5X. As long as the insurance units keep breaking even on their underwriting, which has never been an issue, Berkshire essentially has a bottomless investment fund to play with. Berkshire’s setup is so solid that the real risk isn’t actually Buffett retiring, it’s more about who eventually replaces Ajit Jain in the insurance seat, given he’s at the helm of the straw that stirs the drink.

In 2026, a lot of investors are looking for more conservative investments in order to shelter themselves from overvalued markets. After all, three consecutive years in a row of double-digit returns typically comes with a few shaky years afterwards. However, investors also don’t want to give up all their exposure to the markets, because many understand how much they can truly run up before they eventually come down. Berkshire is the perfect option for someone in this situation. Why?

Berkshire is sitting on more T-bills than the Federal Reserve. This makes them a unique player when things get messy. Berkshire’s stockpile of cash makes holding it more like a 65/35 equity cash position. For a while, I don’t think Berkshire minded the large cash hoard. After all, you could get yields north of 5% on US treasuries. However, now we have the difficulty of declining rates coming into the picture and the urgency that is added to deploying that cash effectively. Many have speculated for a dividend. However, I just don’t see it. I do believe the company will opt for buybacks, if its share price becomes attractive enough.

While the core portfolio has moved toward high-quality technology and financial names, the firm remains a defensive juggernaut designed to outperform during periods of market volatility. I say this because a lot of people express frustration with Berkshire’s lack of returns during speculative eras of market activity. For most of these companies, they take the stairs up during bull runs and the elevator down during bear runs. Berkshire, on the other hand, takes the stairs both up and down.

Despite many expressing how difficult it will be for a company of this size to keep outpacing the S&P 500, Berkshire has done it time and time again. During every bull market, pundits mentioned that Buffett had “lost his touch” because Berkshire has lagged the index. Fast forward a few market corrections later, and there is Berkshire, outpacing the index again.

The primary risk remains the difficulty of finding large-scale acquisitions that can meaningfully move the needle for a trillion-dollar conglomerate. However, it is not like this is the be-all-end-all for the company. A lack of deals wouldn’t result in a catastrophic situation for the company. It simply might result in a lagging share price. So, why are we worried about an event that not only might not ever occur, but might not cause any turmoil at all? Let’s cross that bridge if we get there.

Ultimately, Berkshire Hathaway in 2026 remains a foundational holding for investors seeking a combination of capital preservation and steady, risk-adjusted growth. Between the industrial floor (railways, utilities, etc) and the insurance ceiling, Berkshire is the kind of foundational asset you hold for the long haul, especially when the rest of the markets feel a bit shaky.

- Capital deployment. Following several years of acquisition dormancy due to market valuations, 2026 is viewed as the year Berkshire could execute a massive, company-altering acquisition. With valuations in certain industrial and energy sectors being quite low, which are businesses Berkshire loves, there is a chance we see some big moves in 2026.

- AI growth. Berkshire Hathaway Energy (BHE) is emerging as a primary beneficiary of the artificial intelligence boom. The trend to watch is how BHE manages the soaring electricity demand from AI data centers. Abel has deep expertise in the utility sector, which could be an added tailwind.

- Insurance health. The backbone of Berkshire is insurance via its GEICO and Berkshire Reinsurance segments. The company will need to continue to navigate through catastrophes and execute strong underwriting performance to drive strong returns. In addition to this, higher-than-average interest rates will continue to benefit the insurance segment via large returns on its fixed-income investments. Rates are coming down, but they’re still high.

- Greg Abel taking over. Unlike Buffett, who focused primarily on capital allocation and stock picking, Greg Abel is recognized as an “operations-first” leader. He was heavily involved in the non-insurance side of the business (railroads, energy, and manufacturing), so he is expected to bring a more hands-on management style. The key will be to watch any of the major acquisitions Abel makes, and how he’s able to use this “hands-on” style that Buffett never did to improve the efficiencies of its 90+ subsidiaries.

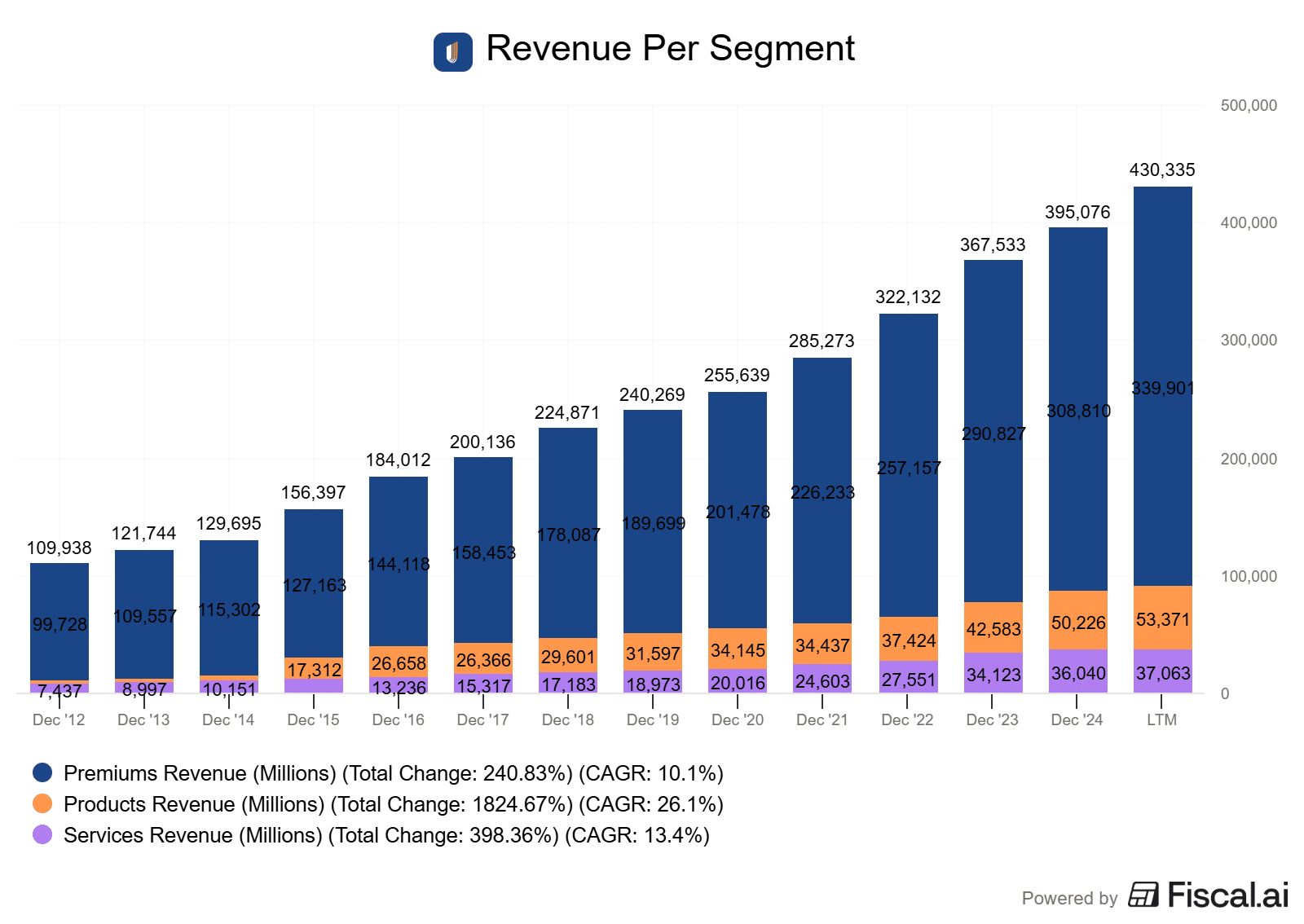

With Berkshire being a conglomerate of businesses, it is difficult to narrow down specific KPIs. However, the bulk of the company is driven through insurance, some smaller subsidiaries, and its investments in major corporations. For this reason, I have the company’s revenue stream by segment chart, which can seem a bit confusing at first, but it gets easier the more time you spend with it. Along with this, I’ve added the company’s GEICO premiums written, a key KPI with its insurance business. The company does announce its equity investment value, but I need to wait until the Fiscal year end to get that.

November 17, 2025 – Berkshire turned in a strong third quarter after a fairly soft second, with operating earnings rising 34% year-over-year, a clear sign the underlying businesses are performing well despite market noise.

Total revenue came in at $95 billion, up low single-digits from the prior year, while net earnings reached $30.8 billion. A large chunk of this, around $22B, was due to investment gains.

That said, it is important to understand that these investment gains are volatile and don’t really reflect the core business operations. I don’t pay much attention to them at all, and have mentioned as much in my reporting on Intact Financial, who was experiencing the same thing.

The real story is the continued strength in insurance and the stability of its other operating units. Insurance underwriting showed improvement over what I viewed was a soft last quarter, with fewer losses and better expense management.

Railroads and utilities, as always, delivered steady results. BNSF’s freight revenue ticked up slightly, which is to be expected considering the macro headwinds. We’ve witnessed it with our Canadian railways. Utilities and energy remained stable as well, with top-line revenue flat but reliable, a hallmark of a regulated utility. Operating costs in these areas did increase, hinting at some margin pressure, but nothing alarming in my opinion. Together, these segments are not huge growth drivers, but dependable income streams that smooth volatility from the investment and insurance side of the business.

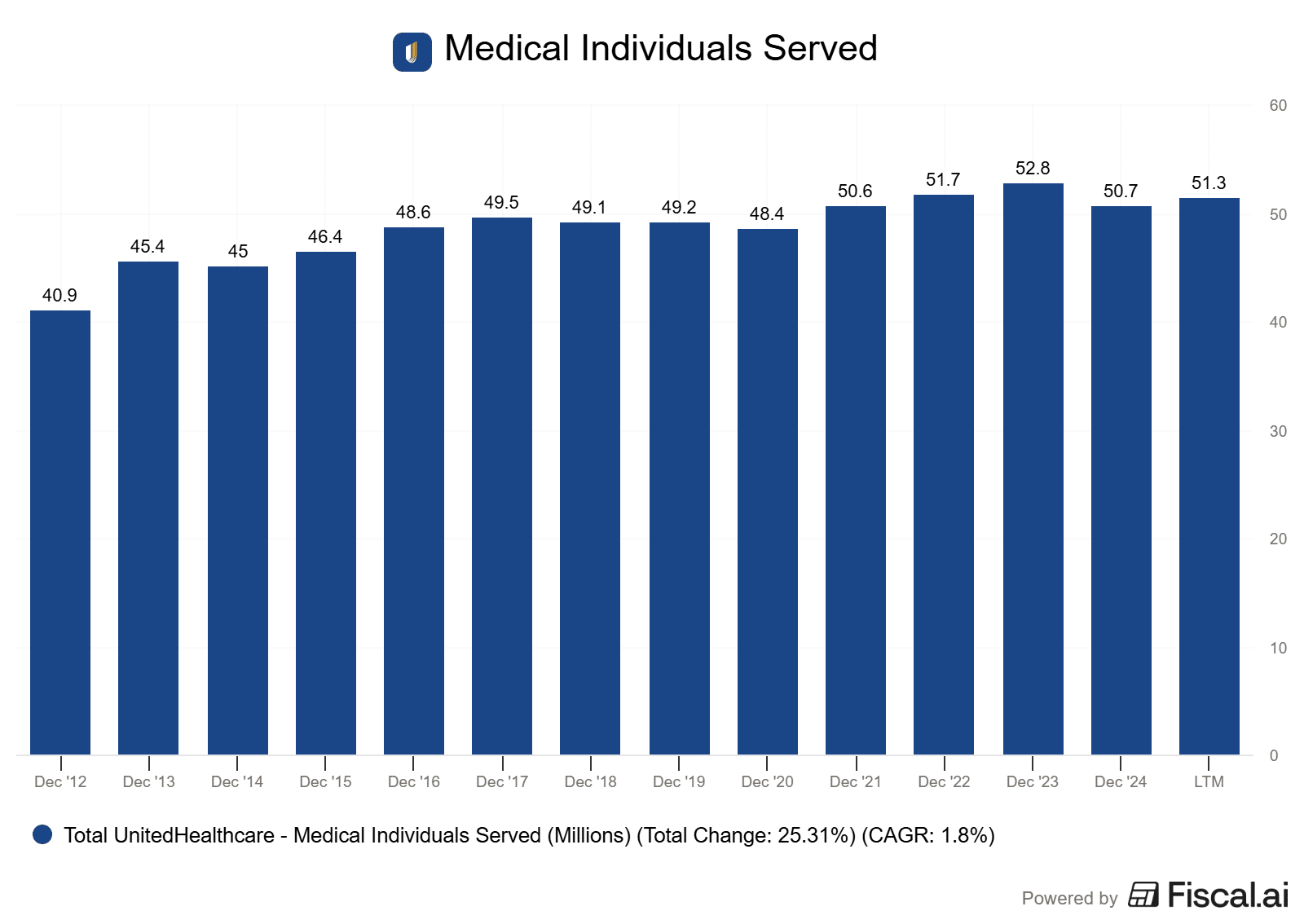

One of the most closely watched themes continues to be capital deployment. Berkshire ended the quarter with over $350 billion in cash and short-term investments, a mind-boggling war chest. The company again refrained from repurchasing shares in Q3, signaling that Warren Buffett and his team still don’t see compelling value at current prices, either in Berkshire stock or elsewhere. However, it did make a few small deals over the last while, acquiring $1.5B~ of UnitedHealth shares and around $4.5B of Alphabet shares.

With Warren Buffett set to step down and Greg Abel taking the reins, the market is eager to see how Berkshire evolves. Abel is seen as a steady hand with deep knowledge of the operating businesses, but questions remain about how he’ll approach capital allocation, especially with such a large cash position to deploy.

Overall, Q3 was a solid bounceback. The core businesses are generating solid returns, underwriting discipline is holding, and the balance sheet is fortress-like, as always. The company remains well positioned to weather volatility and seize opportunities. For long-term shareholders, the value is intact, the engine is running smoothly, and the next few years are going to be very interesting because of the succession.

Alphabet Inc (GOOG)

Alphabet is a holding company that wholly owns internet giant Google. The California-based company derives slightly less than 90% of its revenue from Google services, the vast majority of which is advertising sales. Alongside online ads, Google services houses sales stemming from Google’s subscription services (YouTube TV, YouTube Music, among others), platforms (sales and in-app purchases on Play Store), and devices (Chromebooks, Pixel smartphones, and smart home products such as Chromecast). Google’s cloud computing platform, or GCP, accounts for roughly 10% of Alphabet’s revenue with the firm’s investments in up-and-coming technologies such as self-driving cars (Waymo), health (Verily), and internet access (Google Fiber) making up the rest.

The investment thesis for Alphabet this year is much different than last. Last year, I was speaking on the idea that I believed the fears of AI disrupting Alphabet’s business were overblown and that there was an opportunity from a valuation perspective. This year, the thesis has shifted toward Alphabet dominating artificial intelligence buildouts. It’s funny how short-term fears can spark long-term opportunities. Alphabet is fully valued here, there is no question. However, the future looks bright.

The company has successfully silenced everyone who feared that large language models would cannibalize its search business. How? It just built the world’s best LLM itself. The integration of Gemini into the search experience through AI Overviews has increased user engagement and ad relevance, as consumers find it easier to navigate. Is this advancement horrible for publishers such as myself? Absolutely. They take content produced by writers, show it in an AI overview, and the end user doesn’t have to click through to any article.

However, from the perspective of Alphabet and the end user, the user experience is tenfold what it was a few years ago. This is good for search revenue.

By controlling the entire technology stack, from its own Tensor Processing Units (TPUs) to the world’s most popular mobile operating system (Android), Alphabet has a massive advantage. It can scale AI services more profitably than competitors. We’re starting to see this in the company’s results.

YouTube has emerged as a massive beneficiary of artificial intelligence. Businesses are now using AI to simplify the process of video advertising. Before, you needed cameras, actors, a script, a production area. Now? The rise of AI tools allows even small-scale marketers to generate studio-grade video content from text prompts.

In turn, this fuels a surge in ad spend for YouTube Shorts and the broader platform. This is perfectly timed with a large-scale consumer shift away from written content toward video-first information. As YouTube continues to capture the largest share of streaming time, it is exceptionally hard for media companies to compete.

I feel like I’ve talked about some massive avenues for Alphabet to grow, and I haven’t even gotten to its fastest-growing segment, that being Cloud. For many years, Google Cloud was seen as a third-place competitor. However, cloud revenue has launched, primarily due to its ability to add “AI as a service” type systems. This integration has led to significant margin expansion, with the cloud division now contributing meaningfully to Alphabet’s overall operating income. The huge backlog of enterprise contracts signals that this is not a temporary spike, for anyone who thinks that might be the case.

Finally, headline numbers are no doubt impressive from Alphabet. The company could realistically spin out any of its core businesses, and they’d all be popular companies on their own. However, there is also some upside here from the “Other Bets” the company has made that are finally maturing. One I can think of right off the top of my head is Waymo.

The combination of a revitalized core search business, a dominant video platform in YouTube, and a high-growth, high-margin Cloud division, and one of the best LLMs in the business has created a powerhouse. While the era of easy valuation gains is behind us (you had that chance last year!), Alphabet is still an outstanding company, and worthy of a core position in a long-term portfolio.

- From search to agentic. Google is evolving from a company that provides blue links to someone’s website into a platform that executes tasks. The company is shifting toward “intent-based computing,” where users don’t ask questions, they provide goals, and Google gets them there. This trend is turning Google into a transaction engine, which is ultimately good for those who advertise on Google, which makes Google more money.

- Waymo. In 2026, Waymo has officially graduated from an experimental project to a scalable juggernaut, reaching the milestone of one million weekly rides by the end of the year. Look to how Waymo scales in 2026. If the business becomes popular enough, I could realistically see Waymo being spun out as another entity.

- TPUs. Alphabet’s multi-decade investment in its own Tensor Processing Units is paying off. By running its massive AI workloads on its own hardware rather than relying solely on third-party GPUs, Alphabet can scale its AI services more profitably than any other hyperscaler. This is a similar situation to another Foundational Stock, Amazon. A key trend to watch in 2026 is the potential for Alphabet to begin selling these TPUs to other companies, potentially opening up a brand-new, high-margin revenue stream that mimics a semiconductor business.

- Google Cloud. As I mentioned in the thesis, Google Cloud is no longer a third-place competitor. Revenue growth is now consistently outpacing its larger rivals. This is largely due to its “AI-as-a-Service” model. As the backlog of long-term AI contracts continues to grow, Cloud is now a meaningful contributor to Alphabet’s overall operating income. Keep an eye out as to whether or not it continues to accelerate its revenue growth in 2026.

Google has 3 core business areas you need to pay attention to. The first is Google Search. This is the moaty end of the business and by far the largest. With Google dominating 90%+ of search, this part of the business should be able to provide consistent growth. On the YouTube side, this is an important KPI for the business because of the growing use of video content.

Next, we have Google Cloud revenue. This is no doubt the company’s fastest-growing segment and also its highest-margin segment. Finally, we have a chart of Google’s cost-per-click on its ads. As you can see, in a post-pandemic world, ad rates are launching, which is a good thing for the business.

February 5, 2026 – Alphabet’s fourth-quarter results cemented the fact that it is indeed the leader in the artificial intelligence space. However, the market is currently digesting whether or not that’s a good thing, or a bad thing. I’ll get to why in a bit.

Revenue grew 18% to nearly $114 billion, but the real story is the acceleration in Google Cloud, which grew 48% year-over-year. It’s clear that the enterprise market has moved past the experimentation phase and is now aggressively signing massive deals for AI infrastructure. this is reinforced by a backlog that more than doubled to $240 billion.

Search is also showing zero signs of the disruption many feared. In fact, AI Mode and AI Overviews are actually driving higher engagement and longer queries. The introduction of Universal Commerce Protocol suggests that Google is preparing to own the entire transaction funnel, moving from just a search engine to an agentic platform where you can buy products directly through an AI interface. The UCP is effectively that. It is a platform that allows AI agents to make purchases, so people never need to leave the LLM interface.