Key takeaways

Dollarama offers stability and outpaces many Canadian retailers.

Its unique growth plan could support more upside despite higher prices.

Investors must carefully weigh the company’s valuation at this point.

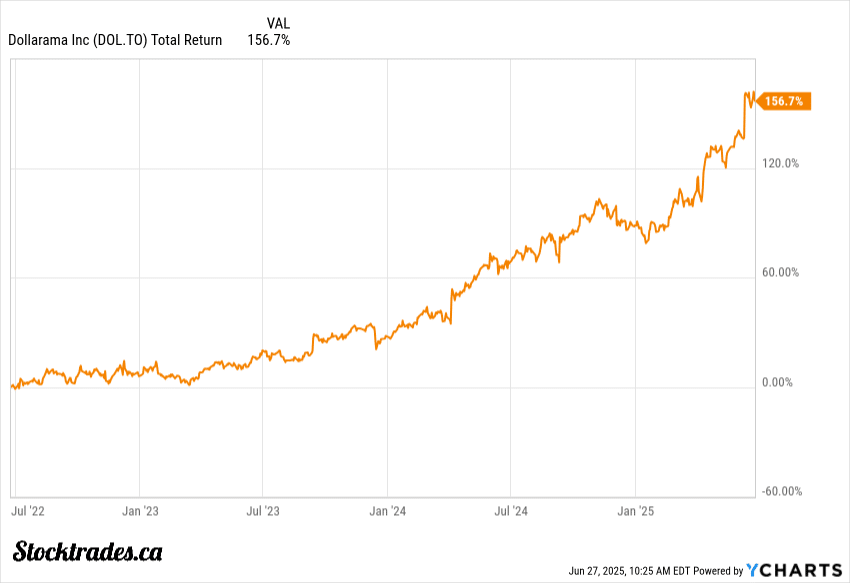

3 stocks I like better than Dollarama right now.It’s not every day we watch a Canadian stock rally more than 40% in a single year, yet Dollarama has done just that and left many investors wondering if the train has already left the station. It has been one of the best stocks to buy in Canada over the last while, there is no doubt.

If we span it out to 3 years, the company’s performance looks even more impressive.

With more Canadians stretching every dollar, we need to ask if Dollarama’s business model, known for steady growth and tight cost control, is still worth it at current valuations.

We shouldn’t ignore concerns about valuation, but we also can’t dismiss the fact that Dollarama’s strategy. Expanding stores, international licensing, and staying laser-focused on margins, which keeps them ahead of most of their retail peers.

The company’s position as a market leader means it tends to weather economic ups and downs fairly well, especially when Canadians are prioritizing smart spending. Lets dig into what really sets this company apart and if the current price is still justified for long-term investors.

Is Dollarama Still a Safe Bet in a Budget-Conscious Canada?

Let’s be honest: with inflation sticking around and the Bank of Canada keeping rates higher than pre-pandemic, most of us are looking for ways to stretch a dollar. When groceries, utilities, and mortgage payments all cost more, it’s natural for people to trade down on everyday purchases.

That’s exactly where Dollarama shines. Plenty of retailers try calling themselves “discount” stores, but Dollarama has made value its whole identity.

It’s not just about cheap knick-knacks. In fact, its aisles are full of essentials: cleaning products, snacks, party supplies, kitchen basics, and personal care items. That steady demand helps separate it from many other retail stocks on the TSX.

The discount element of Dollarama has resulted in some substantial growth:

| Metric | Recent Trend |

|---|---|

| Profit | +27% (year over year) |

| Same-Store Sales | Up 8.2% |

| Share Price | Up 36% in 2025 |

| Avg Location Traffic | Steady/Increasing |

We’ve noticed that more Canadians are shopping at Dollarama even as inflation has slowed a little. Stores continue to attract budget-focused shoppers, and the company’s profit margins remain healthy and industry leading.

What’s clever about Dollarama’s model is its fixed-price-point strategy. Shoppers know exactly what to expect. No sticker shock, no wild surprises at the till. Products are priced in increments, which not only appeals to anyone watching their spending but also helps simplify inventory and control costs.

The Business Model: Why Dollarama Operates on a Different Level

It’s easy to lump all dollar stores together, but Dollarama truly sets itself apart. Let’s be clear: not all discount chains have the same discipline or scale. Our perspective as Canadian investors is that Dollarama’s edge is built into every level of its operations.

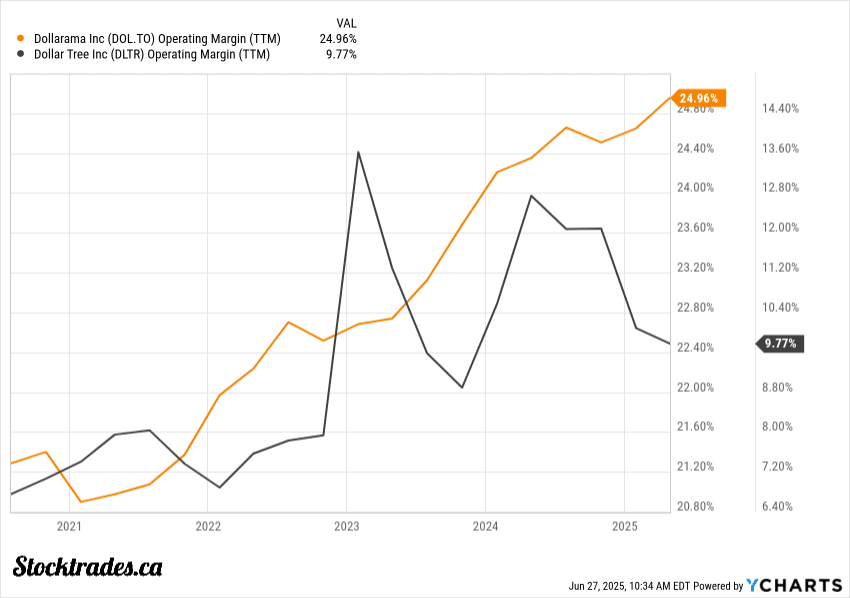

Sourcing efficiency is the first thing that stands out. Unlike competitors who mostly source locally or through third parties, Dollarama’s buying teams work directly with manufacturers worldwide. This means better prices and more control over quality, which are advantages that show up on the shelves and in the margins. Look at the chart below compared with competitor Dollar Tree. It isn’t even close.

Dollarama also dominates with private label products. By developing store-brand goods, they keep costs down and can react quickly to trends. You see this strategy pay off every time they launch a new category or update packaging without missing a beat.

Dollarama’s discipline is legendary. With a centralized distribution network, they move products quickly and efficiently to over 1,000 stores nationwide. No excess warehouses, no wasteful spending.

Here’s a quick breakdown of why the business model simply excels compares to its competition:

| Strength | Impact |

|---|---|

| Central distribution | Lower costs, fast restocking |

| Private labels | Higher margins, easy product rotation |

| Sourcing at scale | Buying power, better supplier terms |

| Tight inventory control | Less shrink, always fresh stock |

Store Expansion, International Licensing, and More

Let’s break down Dollarama’s growth engine. Domestic store expansion remains a core play.

The company is still opening new locations, especially in underserved towns and suburban pockets. They plan to push their Canadian store count from just under 1,600 in 2024 up to 2,200 locations by 2034, raising the long-term ceiling for sales and market share.

But it’s not just a Canadian play anymore. Dollarama owns a majority stake in Dollarcity, which operates in Latin America. This gives us exposure to higher-growth markets like Colombia, Guatemala, and El Salvador.

It’s quite rare to find a Canadian retail stock with international upside but, of course, currency, supply chain, and political risks are part of that package. Still, this angle is promising for expanding earnings outside Canada’s borders.

Omnichannel is the wild card. Dollarama’s DOL+ platform lets us buy in bulk online, but its rollout has been careful, even slow. On the one hand, that caution avoids costly missteps seen at other big-box retailers. On the other, it risks missing out on evolving consumer habits, especially for younger Canadians who want seamless digital options.

Valuation – Is it Still Worth the Premium?

Dollarama stock is no bargain at these levels. The company trades at a price-to-sales ratio above 6, far above traditional retailers in Canada. By comparison, big box names like Canadian Tire and Loblaw usually see lower multiples. We’re paying a hefty premium for Dollarama’s strong brand, steady growth, and consumer tailwinds.

| Metric | Dollarama | Canadian Retail Peer Average |

|---|---|---|

| P/E Ratio | ~32 | ~18-22 |

| EV/EBITDA | ~23 | ~12-15 |

We should ask if the market is already betting on several more years of rapid earnings growth. While Dollarama keeps posting double-digit revenue gains and healthy EPS growth, the bar for what counts as “outperformance” is set high. I would argue the company is priced to perfection.

Dollarama’s operating margin has held up well, even as costs increased. That’s not something we can say for every retailer in this country. Strong margin control hints at solid management and a strong business model.

Let’s not ignore free cash flow. Dollarama remains a cash machine, even after accounting for new store openings and investments.

The company pays a tiny dividend, less than 0.5%, and it’s clear that management would rather reinvest in expansion than pay out more today. In our view, this makes sense for a business with such reliable cash generation and growth prospects.

There are some flags on my radar. Inventory levels have crept up, and while same-store sales are still positive, I’ve noticed the growth rate is tapering off from pandemic highs. If this trend continues, the market’s high expectations might become tougher to meet.

Overall, I’m cautiously optimistic, but I’m not sure I’d be paying the prices it’s trading at today.